Most of the Magnificent Seven reported earnings last week. Overall, it was a strong quarter, with Microsoft, Meta, and Apple all beating expectations on the top and bottom lines.

Apple

Apple’s earnings proved again how good it is to own the rails. The company posted a better-than-expected holiday quarter, with revenue rising 16% — its fastest quarterly growth in more than four years. Sales in China rose nearly 38% year over year, a sharp turnaround after declines in three of the past four quarters.

That strength came despite Apple’s underwhelming AI narrative. Growth was driven by stronger-than-expected iPhone demand (quarterly sales jumped 23%) and record services revenue (up 14%).

Meta

Meta CEO Mark Zuckerberg delivered a clean AI growth story this quarter, and investors loved it.

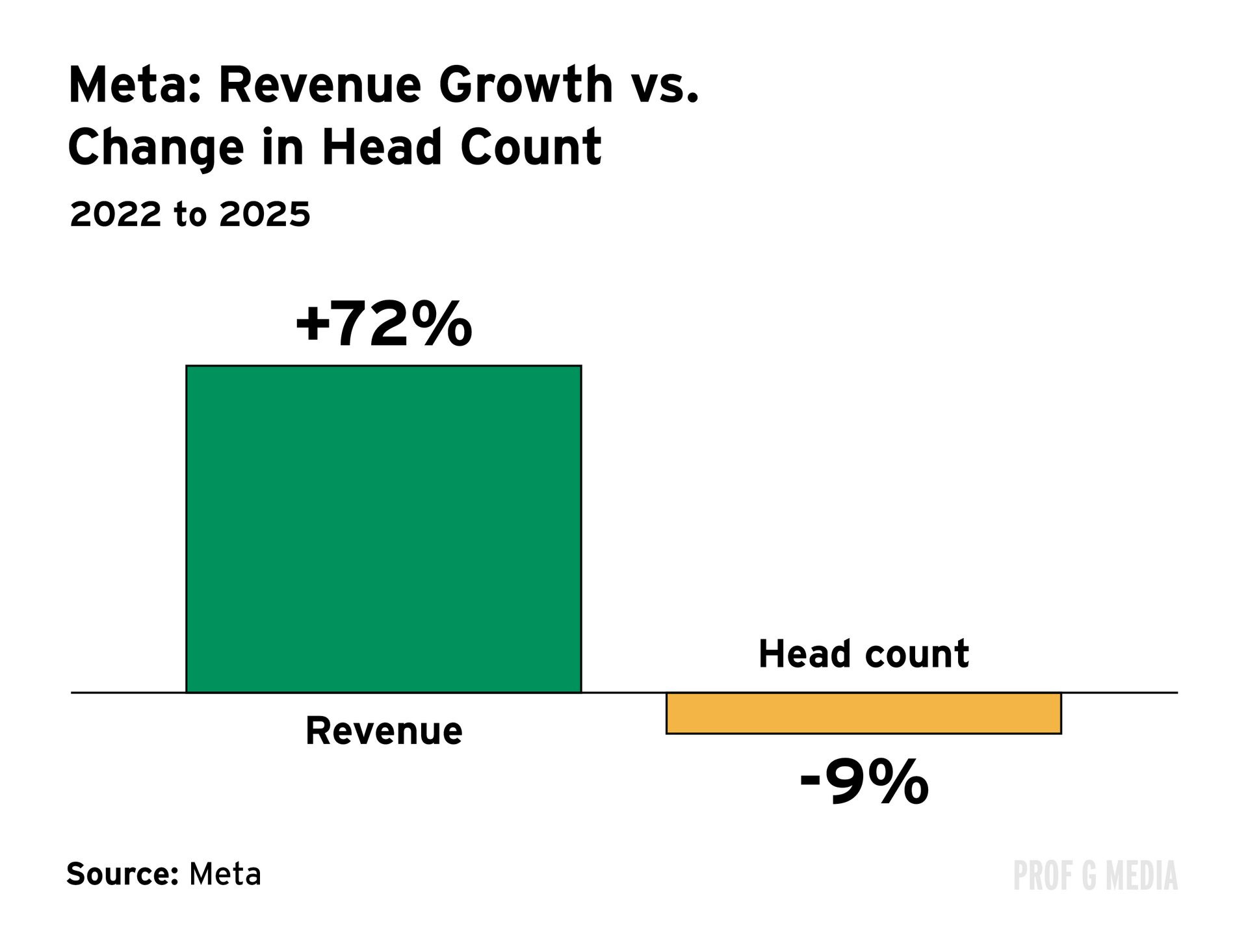

Meta’s fourth-quarter sales rose 24%, and the company issued stronger-than-expected sales guidance for the current quarter.

AI is supercharging Meta’s ad-targeting capabilities: Users clicked on Facebook ads 3.5% more often this quarter, and conversions increased 1%. For a company of Meta’s scale (40% of the world’s population uses a Meta product daily), that’s meaningful.

The growth helped justify a sharp increase in 2026 capex estimates to $115 billion to $135 billion — around 60% above last year — and the stock jumped as much as 10% after hours.

Microsoft

Microsoft had another strong quarter, but a slight slowdown in cloud growth rattled investors. Shares fell 5% after hours and plunged 10% the next day, erasing $357 billion in value — the second-largest single-day drop in market history.

Microsoft’s AI growth story looked more complicated this quarter. Its cloud backlog grew, but more than half of future bookings are attributable to OpenAI.

There’s also growing concern around Microsoft’s partnership with Anthropic, as Anthropic’s Claude Cowork could end up competing with Microsoft’s own AI-powered productivity tools.

Tesla

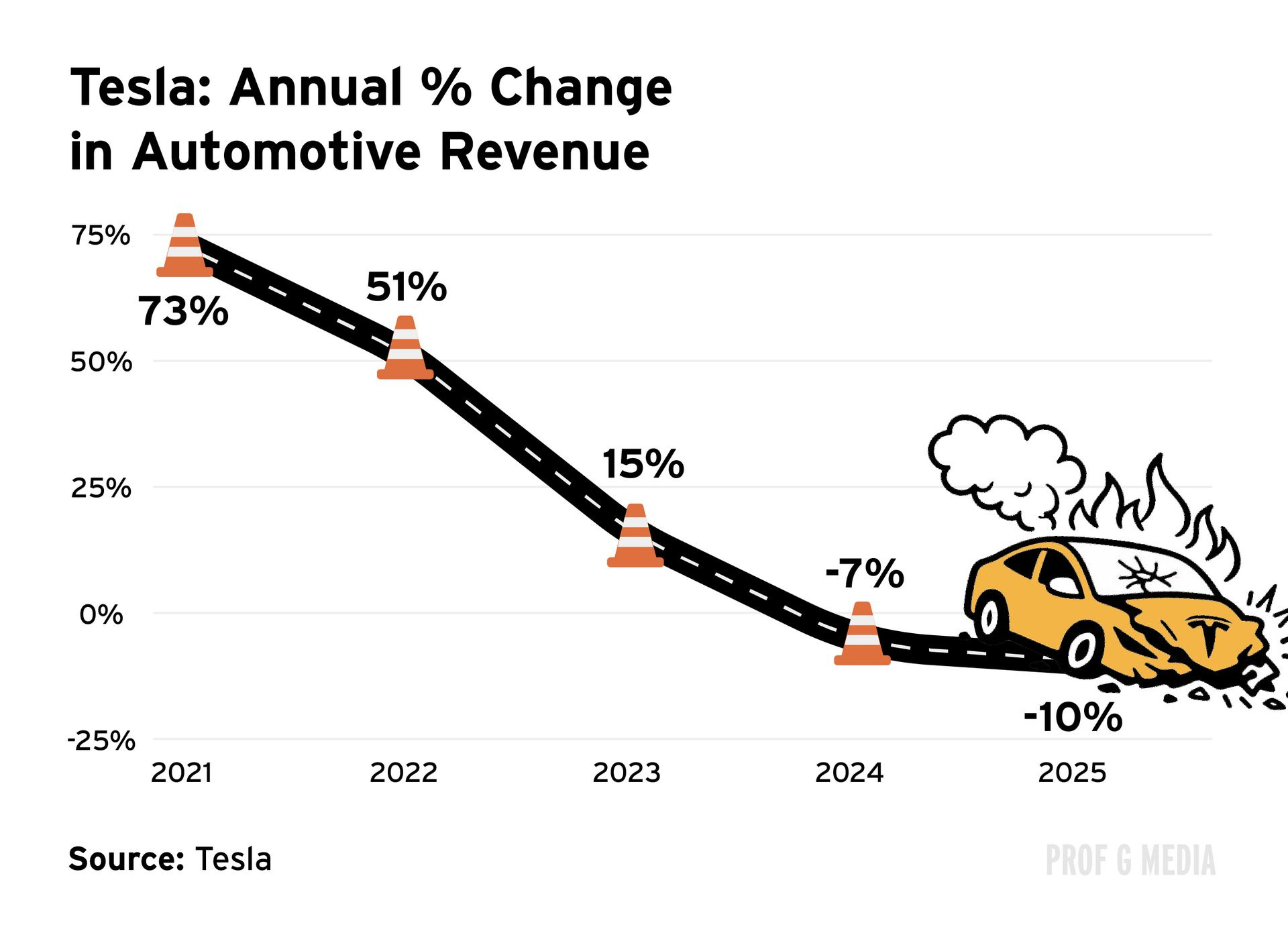

Tesla’s full-year sales declined for the first time ever, and net income fell 61% to $840 million — even after including almost $550 million in regulatory credits. Excluding those credits, profits would have declined 86% year-over-year.

Despite all of that, the stock rose 2% after the earnings announcement.

The earnings call was decidedly not about electric vehicles. Musk mentioned Optimus 28 times on the earnings call and said they will start using Tesla production facilities to build Optimus robots. He also announced that Tesla is investing $2 billion into his AI company, xAI.

Meta’s earnings showed that it’s better to be in the business of leveraging AI than in the business of AI. Anyone who’s on Instagram understands the power of AI because you keep getting served more and more relevant content, which increases ad clicks and time spent on site. Time spent on Instagram Reels increased 30% globally last quarter. That’s remarkable.

It’s better to draft off of the AI wars than to be on the front lines.

Tesla’s earnings, on the other hand, were about anything other than their core business. Talk about weapons of mass distraction – on the earnings call, Musk updated investors on Tesla’s new mission, which is “to build a world of amazing abundance.” I would translate that into an abundance of ketamine before the earnings call.

Automotive revenues declined 10% year over year, and Tesla, which used to have some of the highest margins in the auto industry, now has pre-tax profit margins that are about 6%, less than half of Toyota’s.

Make this make sense: Tesla trades at 400x earnings while Toyota, the best-managed automotive company in the world, trades at 10x earnings.

The biggest issue with Microsoft’s earnings was their remaining performance obligations. That is how much revenue they have in the pipeline. It grew dramatically to $625 billion, which sounds like great news. But here’s the catch: 45% of that backlog is attributable to OpenAI.

And where is OpenAI’s money even coming from? It’s not coming from profits, it’s coming from Microsoft. It’s all just a circular transaction.

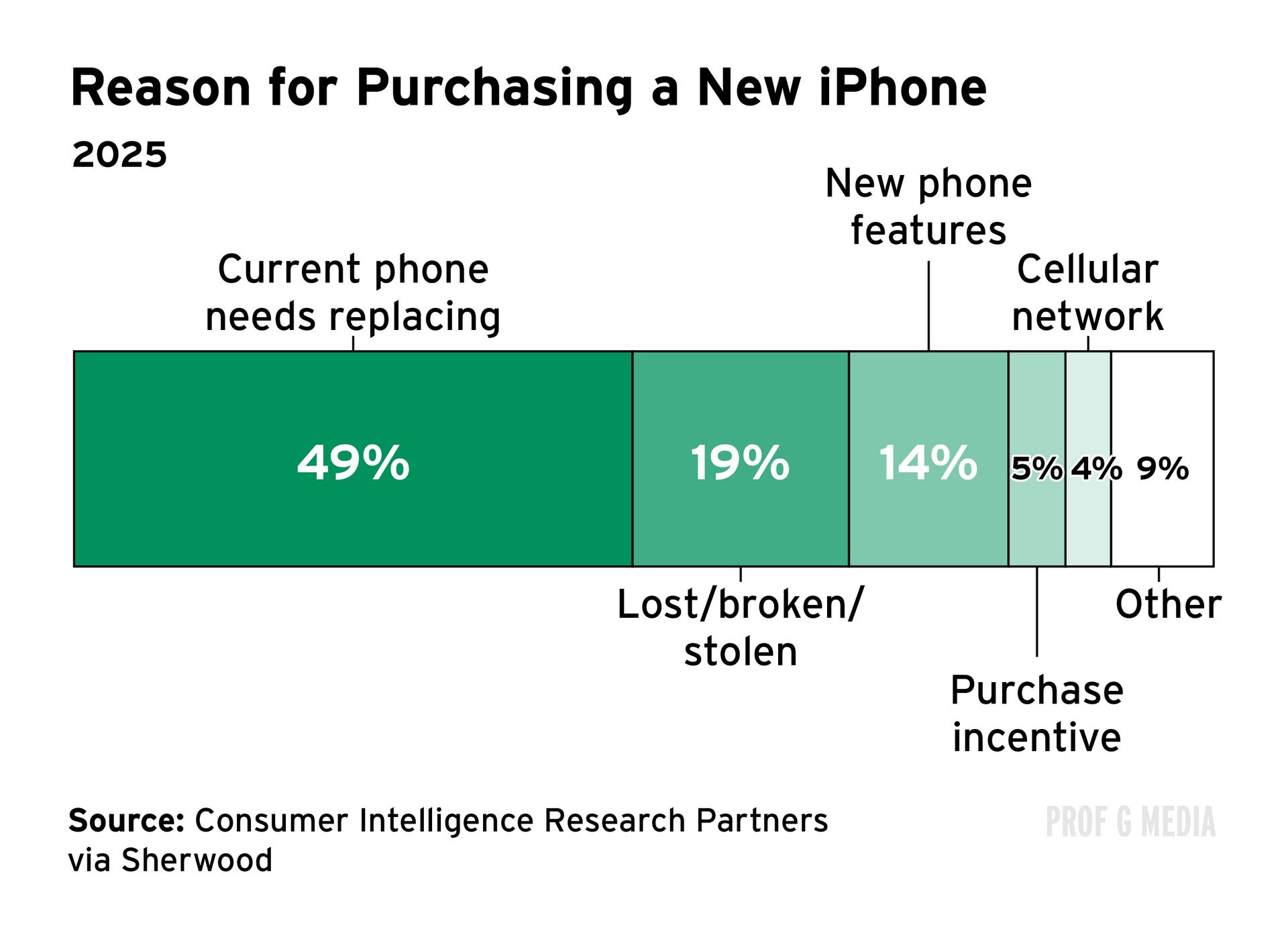

Apple’s earnings were solid but unremarkable. The 16% revenue growth is impressive, but I don’t think it’s a testament to the product itself. An analysis found that only 14% of people are buying iPhones for the new features.

Apple has gotten so entrenched in our society that the iPhone just sells itself. But in the long term, I don’t think what they’re doing is very exciting. Apple is becoming more and more of a legacy tech company.