China's Chip Queen Takes on Nvidia

Plus, the Chinese billionaires making Hong Kong richer than Switzerland

TL;DR

Huawei’s chip queen just declared Moore’s Law dead

Europe is arming for a trade war China will probably win

Hong Kong just dethroned Switzerland as the world’s top wealth hub

Huawei’s Chip Queen Has A New Theory of Everything

Nvidia’s CEO Jensen Huang has publicly conceded China’s AI chip market to Huawei. Huawei now holds around 50% of China’s AI chip market in 2026, and the market itself is projected to grow from $21 billion this year to $67 billion by 2030, according to Morgan Stanley.

The architect behind Huawei's semiconductor push is He Tingbo, who has run the company's internal chip unit since 2003 on an annual budget of roughly $400 million. This month she announced what she is calling the Tao scaling law, a new framework for measuring semiconductor performance that rejects the old race to miniaturize transistors. Instead of shrinking components, her approach focuses on how fast data moves through a chip, optimizing the arrangement of chips, wiring architecture, and memory systems to extract greater compute efficiency.

The announcement matters because the physical limits of Moore’s Law are real. Transistors are already smaller than a human virus, and further miniaturization is hitting the walls of physics. TSMC is moving toward 3D stacking for the same reason. Huawei’s argument is that it has a workable alternative route. Even if China cannot access Nvidia’s latest Blackwell chips, He Tingbo’s team can stack and cluster indigenous Huawei chips to close the gap, pairing that compute with cheap solar electricity available near the Gobi Desert to run data centers at scale.

The benchmark questions remain open. According to the Council on Foreign Relations, the best U.S. AI chips are still roughly five times more powerful in compute than what Huawei can currently produce, and that gap may be widening. In the most optimistic scenario, Huawei can supply only about 4% of the aggregate AI compute that Nvidia produces. Whether that is enough to meet China’s surging domestic demand for AI infrastructure is the central question.

Alice’s Take: Huawei is becoming the Samsung of China. It started in telecoms, expanded into handsets, and is now building out a complete technology supply chain across the stack. That evolution matters: Huawei is no longer just a chip company under siege. It is the symbol of China’s capacity to prevail against the U.S. export control regime, and He Tingbo is the human embodiment of that story. Her Tao scaling law may or may not become the industry standard for benchmarking, but the confidence it signals is real. I am still bullish on Chinese semiconductor stocks. The sector is up at least 40% year-to-date and is functioning as the picks-and-shovels play for Chinese AI investment the way Nvidia has in the United States.

James’s Take: The running is going in China’s favor. The core insight is that China does not need to match Nvidia chip for chip. What it needs is sufficient compute to train and run its models at the scale domestic demand requires. Stacking and clustering indigenous chips, combined with cheap electricity from solar-powered data centers near the Gobi Desert, gives China a credible workaround. Blackwell chips are considerably more powerful, but China’s engineers have a track record of finding ingenious solutions to the constraints placed on them. Huawei has been the main target of American sanctions and it seems to have prevailed. This is a geopolitical story as much as a technology one.

Europe is Arming for a Trade War. Germany May Not Let it Happen

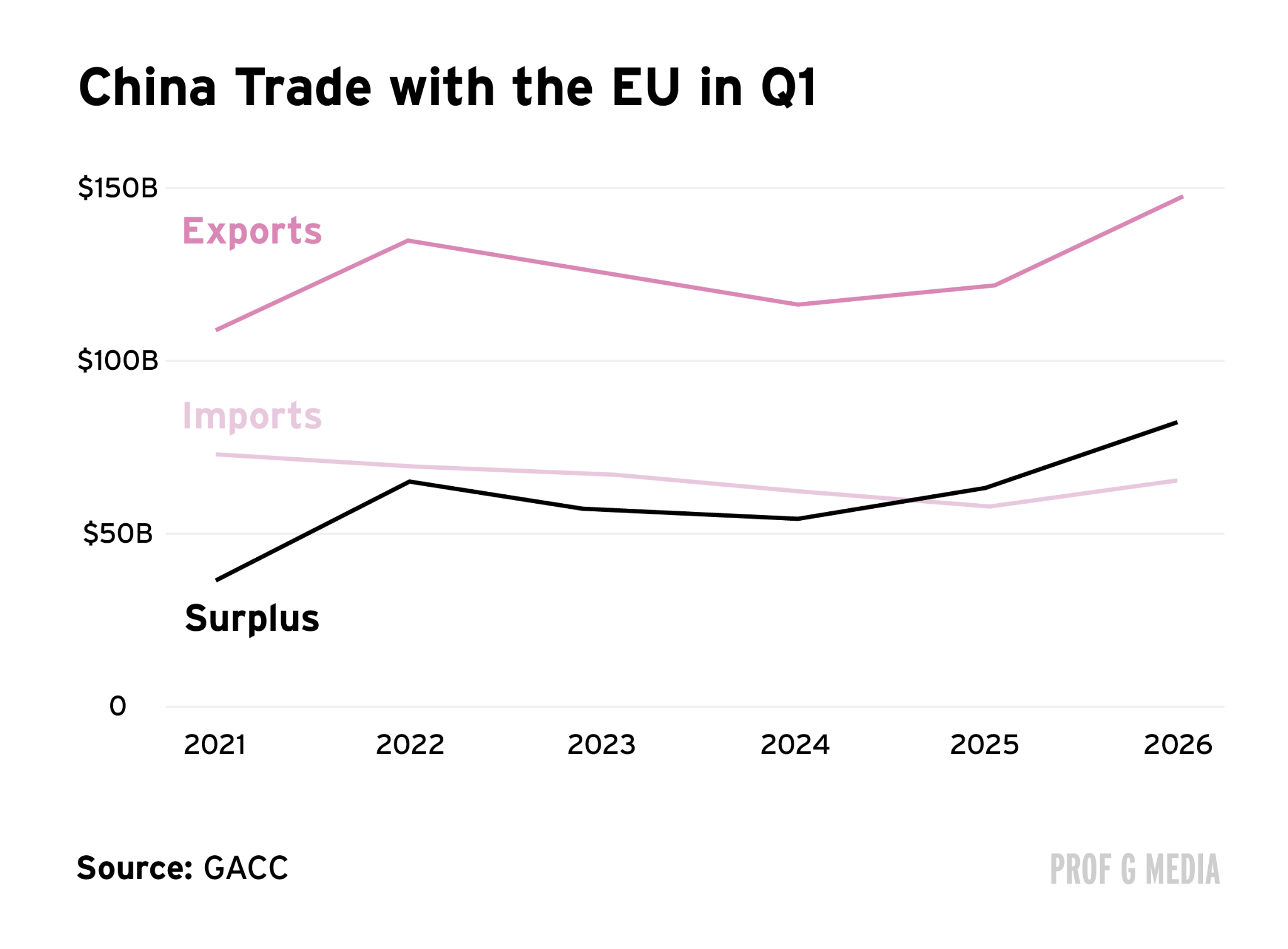

China’s trade surplus with the European Union has reached a record high, topping$400 billion last year, and a coalition of five EU member states is now pushing Brussels to act. France, Italy, Spain, the Netherlands, and Lithuania are calling on the European Commission to deploy stronger cross-sector tariffs and defensive trade tools against Chinese state-subsidized imports. European Commission officials have signaled they are drawing up what they describe as more assertive and effective trade defense policy.

The pressure is also coming from above. A G7 summit is scheduled in France on June 15, where reducing economic dependence on China is expected to be a central theme. French President Emmanuel Macron has been unusually direct, saying that China is effectively dismantling large parts of European industry. The sectors most exposed are cars and machinery, but chemicals are increasingly under pressure as well.

The structural tension is this: Germany’s largest multinationals depend on China as their single biggest market, and they will lobby against any trade measures that risk retaliation from Beijing. China, meanwhile, has demonstrated it is willing to weaponize rare earth exports and agricultural tariffs when confrontation escalates. A separate OECD report estimates that 60% of Chinese market gains are driven by state subsidies.

There is also a longer-run dynamic that complicates the tariff argument. Chinese foreign direct investment into Europe grew 57% year-on-year in the last reported period, concentrated in automotive manufacturing and green tech. That mirrors the playbook Japan used in the 1980s when U.S. tariffs prompted Toyota and others to build factories in America rather than accept import restrictions.

Alice’s Take: I am skeptical these trade barriers will work. EV tariffs went up over a year ago, and Chinese EV exports into Europe are still at record levels. The more interesting story is what China is doing with its capital. If Chinese companies simply build factories in Hungary, or increasingly in France and Germany, the tariff question becomes less relevant. You end up with Chinese firms creating European jobs in green tech and batteries while European manufacturers slowly lose ground. That may well be the equilibrium we reach. Beijing’s counterpunch will almost certainly target European agriculture: cognac, pork, wine. That is where the political lobbying power is, and China knows it.

James’s Take: My prediction is that Europe will not have a full-blown trade war with China. The interests of Germany’s big multinationals will ultimately prevail in Brussels. But the deeper risk is the worst-case scenario: Europe erects barriers that protect its existing inefficiencies, those measures fail to stop Chinese competition, and no structural reform happens in the meantime. High energy costs, high labor costs, restrictive investment laws, very low productivity across almost all countries. Europe could end up losing a trade war it started unprepared, without having fixed any of the underlying problems that made it vulnerable in the first place.

Hong Kong is the New Capital of Capital

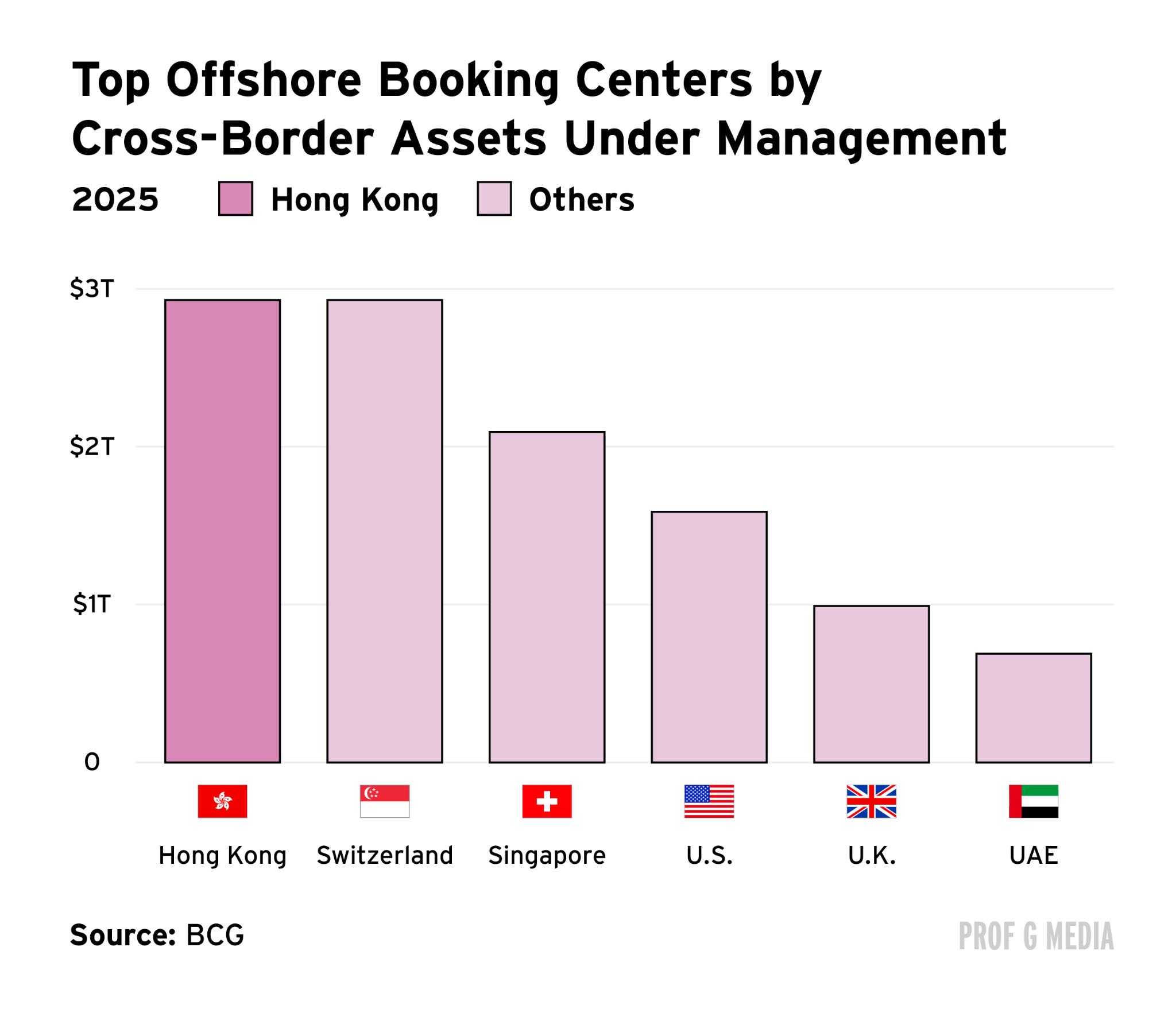

Hong Kong has overtaken Switzerland as the world’s leading offshore wealth hub, according to a new report from Boston Consulting Group. Measured by total cross-border assets under management, Hong Kong ended 2025 at $2.95 trillion, a 10.7% increase year-on-year and slightly ahead of Switzerland’s total. BCG projects the gap will widen to nearly $600 billion by 2030.

The shift is driven by mainland Chinese capital looking for somewhere to go. Large volumes of fixed-term deposits on the mainland, many yielding around 5% on five-year terms, are maturing this year into an environment where current deposit rates have fallen to around 2%. With Chinese real estate still declining and the equity market volatile, mainland investors are looking for alternatives. Hong Kong’s status as a freely convertible currency hub, where renminbi can be exchanged and invested globally, makes it the natural destination.

Hong Kong now has 71 billionaires, second only to New York. The stretch of land once occupied by old British trading houses now houses mainly mainland Chinese tech tycoons. The wealthiest person in Hong Kong is Robin Zeng, chairman of CATL.

The National Security Law, enacted in 2020 following the 2019 protests, prompted significant concern at the time that Hong Kong’s era as a wealth haven was ending. That concern proved wrong. Political freedoms have been circumscribed, but economic freedoms have been carefully preserved. Beijing does not want to kill the golden goose.

Alice’s Take: I was not surprised by this. When you spend time in Hong Kong over the past 18 months, the shift in sentiment is tangible. Post-COVID despondency has been replaced by something more purposeful. Beijing wants Hong Kong to serve as the channel through which mainland capital finds global investments and foreign capital finds mainland opportunities. The expiry of trillions in mainland fixed-term deposits this year is a structural catalyst. With onshore yields low and real estate still under pressure, Hong Kong wealth management products are increasingly attractive. Phase one of China’s wealth story was getting rich. Phase two is creating the infrastructure to maintain and expand that wealth. Hong Kong is central to phase two.

James’s Take: When the National Security Law came in, I said that Beijing would not sacrifice Hong Kong’s economic freedoms because the city is too valuable as a financial gateway. That has proven correct. The flow of mainland money has not just continued, it has accelerated. On Hong Kong versus Singapore: I think they serve different functions. Hong Kong is still more freewheeling, more entrepreneurial. Singapore is more regulated and more conservative. It is politically tighter now, but economically it retains a character that the mainland does not replicate.

Predictions:

Alice’s Prediction: The CNY has been up about 3.4% against the dollar year-to-date, and I don’t think that is durable. If the oil supply shock from Iran causes demand destruction globally, China’s export engine takes a hit, and an appreciating yuan makes that worse. We’re currently at 6.7. I expect some paring back before a rebound in the second half, moving back toward the 7 region.

James’s Prediction: Europe will not have a full-blown trade war with China this year. There will be skirmishes and some new defensive tools, but German corporate interests will ultimately prevent serious escalation.

There is a prevailing and trendy sentiment against the value of patents in the west. I think this is misaligned with the true value of a global IP strategy. I’d love for you guys to discuss intellectual property more.

I know you guys cover this when pertaining to contemporaneous issues such as the Financial Times article that came out shortly before trumps China visit.

Please discuss these issues more

You guys remind me of the McLaughlin group on PBS with your predictions… keep it up 👍