Did Markets Overreact to Citrini’s AI Scenario?

Plus: an update on Waymo, Uber, and the autonomous wars.

94%

of all cryptocurrency buyers are Gen Z or millennials.

Did markets overreact to Citrini’s AI article?

Trump likes to exaggerate. What is the real state of the union?

Who are the winners and losers of the Warner Bros. acquisition saga?

Newsletter exclusive: The dark horse in the autonomous vehicle wars

Breaking Down Citrini’s 2028 Global Intelligence Crisis

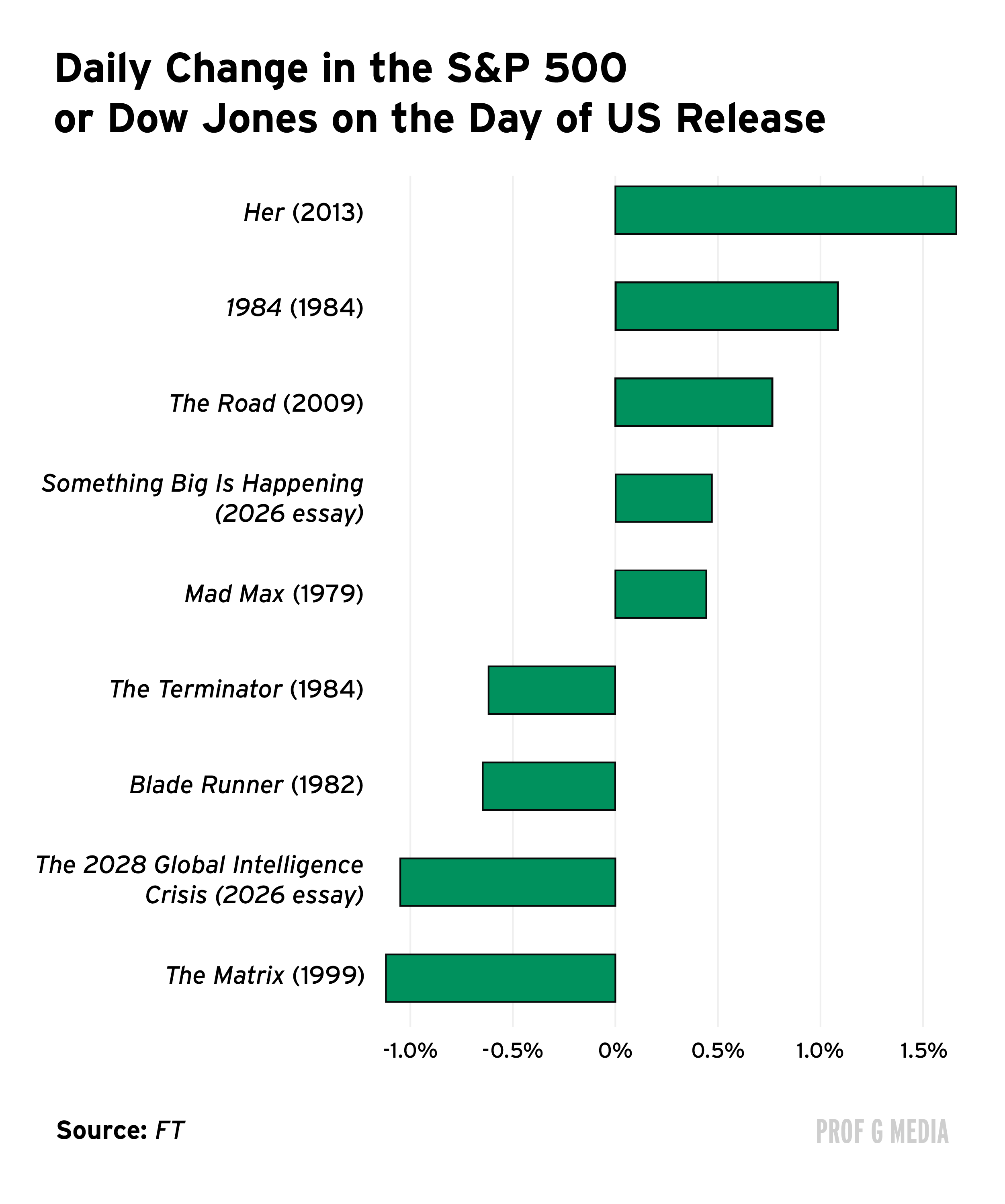

A science fiction article from Citrini Research erased $300 billion in market value last week.

Set two years in the future, The 2028 Global Intelligence Crisis imagines a scenario where AI has driven unemployment to 10%, consumer spending has collapsed, markets have plunged, and the economy is fundamentally reshaped.

The foreboding piece only intensified fears about software obsolescence, and the State Street Software & Services ETF fell 5% the day after the article was published.

Companies name-checked in the post including DoorDash, American Express, KKR & Co., and Blackstone fell by at least 6%, and Uber, Mastercard, Visa, Capital One and Apollo all fell by 4% or more.

The co-author of the post, Alap Shah, confirmed that his hedge fund had “a set of shorts against businesses that we think are going to be disrupted by AI.”

Later in the week, eBay announced it would lay off 6% of its employees, and Block (formerly Square) announced it would cut 40% of its workforce.

Block CEO Jack Dorsey blamed the cuts on AI, writing: “The intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working.” Block’s stock jumped 25% in response to the news.

U.S. companies announced 108,435 layoffs for January, up 118% from a year ago.

The layoffs made the Citrini article’s claim that AI adoption will cause mass unemployment seem less like science fiction.

At the same time, while AI has, and will continue to destroy some jobs, there is no evidence that it will happen at the pace that the post suggests.

Business leaders surveyed in the U.S., U.K., Germany, and Australia expect AI to reduce employment by around 0.7% over the next three years. This pace should give governments time to react to changes in labor demand.

Furthermore, AI will be a subpar substitute for most human labor until hallucination rates meaningfully decline. In the best case, 80% of AI-generated answers are correct. Would you trust an employee who is wrong a fifth of the time?

The article also ignores Jevons Paradox, which shows that efficiency improvements can actually lead to higher total resource use. If each unit of efficient work gets cheaper, that can expand output so much that demand for labor actually increases.

In fact, it’s already happening. It looked like software engineers would be completely replaced by AI coding tools, but now job postings are on the rise. As it gets cheaper to ship software, it becomes easier to start new companies and launch new products. “Vibe coding” goes only so far when you need to launch a professional product.

There used to be people who would sit in the elevator all day and wear a uniform and a special cap. They would literally stand there and press people’s floors for them. Is anyone like, what happened to all the good elevator operator jobs?

Of course we’re gonna have disruption. Entire categories of jobs will be lost. The thing that people are worried about is that the destruction will all happen at once. The more realistic scenario is that this rolls industry through industry. And as AI destroys jobs across industries, it creates new ones in their wake. The time frame is what matters.

But the fact that a creative blog posted on Substack inspired such incredible selling pressure and value destruction tells me a lot about how investors are feeling right now.

The State of the Union: Rhetoric vs. Reality

In the longest State of the Union address in history, President Trump painted an optimistic picture of the country, declaring a “turnaround for the ages.” He covered everything from inflation and immigration to health care and voter fraud.

He highlighted some legitimate wins: the Trump accounts, which give every American child born between 2025 and 2028 a $1,000 stake in the stock market, the most-favored nation program for lowering the price of pharmaceutical drugs, and he announced that Big Tech companies will commit to paying the electric bill for their data centers.

But the rest of Trump’s speech serves as a reminder that you can do anything with numbers if you’re morally flexible enough. So, what is the real state of the union?

Foreign investment

Trump: “In 12 months, I secured commitments for more than $18 trillion …”

Reality: A White House website boasts that U.S. and foreign investments under Trump total $9.7 trillion, and even that figure is disputed.

Tariffs

Trump: Foreign countries are paying the tariffs.

Reality: The Fed Reserve Bank of New York found that nearly 90% of the tariff burden falls on U.S. firms and consumers. The Congressional Budget Office puts it at 95%.

Employment

Trump: “More Americans are working than at any time in the history of our country.”

Reality: U.S. had almost no job growth in 2025; it was the weakest year of job creation since 2020. Manufacturing, one of Trump’s main focus areas, shrank as a share of total U.S. workforce to a record low last year of less than 8%.

Market performance

Trump: “... the stock market has done so well, setting all those records.”

Reality: The market may have set records, but its performance lags most other developed markets. The S&P 500 rose 16% in 2025, while the MSCI All Country World Index minus USA rose 29%.

The whole speech was a master class in cherry-picking. To be fair, unemployment is pretty low. Inflation is down from its peak, GDP growth is positive, but it’s especially concentrated around a small number of companies. He’s sort of asking everyone to stare at AI and big company capex and then take off your glasses when you’re looking at your grocery receipts.

At one point, he said we brought in $18 trillion in investment. Where the f*ck is he even getting these numbers? It felt like an earnings call, where the investors are the Republicans and there’s no SEC. You can’t get in trouble. You can just throw out numbers. It’d be like if Jensen Huang said, Our earnings were up 11 million percent. It was the greatest earnings quarter in history.

But anyway, we’re not dealing with the real issue, which is the deficit. Democrats are gonna have to cut spending, Republicans are gonna have to raise taxes. Let’s get to it. Who are the adults in this room? I feel like Congress burns more calories clapping than actually legislating.

Netflix vs. Paramount for Warner Bros. Discovery — Who Came Out Ahead?

Netflix has dropped out of the Warner Bros. Discovery bidding war. The transaction will still need regulatory approval, but for now, Paramount has come out on top.

The Warner Bros. board declared Paramount’s $31/share offer ($111 billion) for the whole company superior to Netflix’s $27.75/share offer ($83 billion) for HBO and the Warner Bros. movie studio.

The combined Paramount-Warner Bros. entity will still be smaller than Netflix in terms of total subscribers (211 million subs vs. Netflix’s 325 million).

Warner Bros. gave Netflix four days to counter, but the company declined, saying the deal was “no longer financially attractive.”

The OG streamer will walk away with a $2.8 billion breakup fee, equivalent to 25% of Netflix’s entire net income last year.

On the news, Warner Bros.’ stock fell nearly 3%, Netflix increased 10%, and Paramount popped nearly 20%.

Let’s talk about winners and losers.

At the top of the list in terms of winners are WBD shareholders and David Zaslav. I think he was a mediocre operator, but he’s an outstanding investment banker. This is a company that’s gone from a low of $8/share six months ago to $31/share, and the business has gotten worse over that period.

A close second in terms of winners is Netflix shareholders. This saga shows that Ted Sarandos is a disciplined operator. Good operators walk away when the deal no longer makes sense.

Netflix stock increased 10% on the news, adding $36 billion in market cap, and they get another nearly $3 billion for the breakup fee. So if you consider the price they were going to pay — $83 billion — plus the $40 billion free gift with purchase, they’re basically getting $120 billion to not do this deal. I think Netflix is probably a buy right now.

The biggest loser is the creative community. Paramount has paid so much for this company — there is no vision that’s going to increase revenues to the extent to justify the price they paid. They are gonna have to focus on the expense side (Latin for layoffs).

You’re going to see a destruction in human capital that’s going to make Jack Dorsey’’s announcement look soft and cuddly.

sponsored content

Keep Your SSN Off The Dark Web

Every day, data brokers profit from your sensitive info—phone number, DOB, SSN—selling it to the highest bidder. What happens then?

Best case: companies target you with ads.

Worst case: scammers and identity thieves breach those brokers, leaving your data vulnerable or on the dark web.

It’s time you check out Incogni. It scrubs your personal data from the web, confronting the world’s data brokers on your behalf. And unlike other services, Incogni helps remove your sensitive information from all broker types, including those tricky People Search Sites

Help protect yourself from identity theft, scam calls, and health insurers raising your rates.

Plus, just for PROF G MARKETS readers: Get 55% off Incogni using code PROFG

sponsored content

Newsletter Exclusive: The Autonomous Vehicle Race Has a New Rivalry

The conventional wisdom is that the autonomous vehicle war is a two-way race between Tesla and Waymo. That’s wrong.

The real race is Waymo versus Uber.

Waymo is expanding into four new U.S. cities, bringing its total to 10, with testing underway in another 20 and a confirmed expansion to London this year. In California, it’s doing 1.2 million rides per month — a 22x increase over two years — and has already surpassed Lyft in San Francisco, despite it costing nearly 30% more.

Waymo’s newest generation system addresses cost concerns. It uses 42% fewer sensors than the previous version, and is expected to cost $20,000 per unit (on top of the vehicle cost) — a more than 50% reduction from the fifth-gen system. Tesla CEO Elon Musk has said that the company’s robotaxi will cost less than $30,000.

Uber is taking the “toll booth” strategy: trying to partner and take a cut from every piece of the value chain. It has partnerships with nearly two dozen autonomous companies, and, in a major shift from Uber’s traditional asset-light business model, the company is starting to invest in owned physical assets. The company is building fast charging stations for AV vehicles in San Francisco, LA, and Dallas, and is working with Wayve and Lucid to manufacture robotaxi vehicles.

Meanwhile, Tesla is still struggling. For over a year, Elon Musk has said Tesla is just months away from launching a fully driverless robotaxi service in California. But Tesla’s fleet of over 1,000 vehicles in SF all require safety monitors behind the wheel, and most of its “autonomous” vehicles operating in Austin also require a safety monitor.

Rollout isn’t the only problem. Tesla’s robotaxis have been involved in crashes at 8x the rate of human drivers. Waymo, by contrast, estimates that its vehicles get into injury-causing crashes 80% less than human drivers.

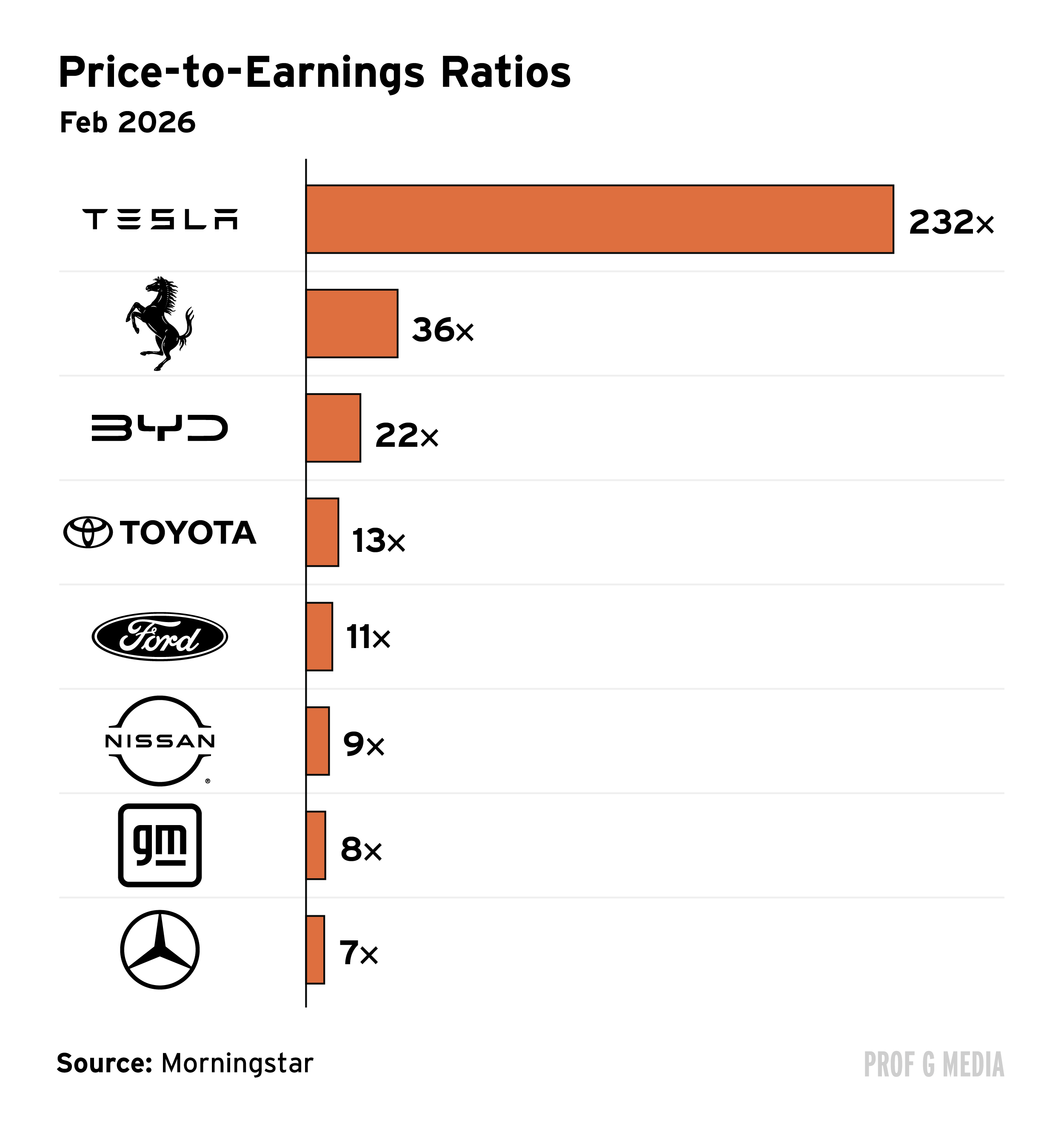

In the face of his public robotaxi failures, Musk’s focus has shifted to Optimus robots. For investors counting on Tesla’s robotaxi vision paying off (and for a stock trading at nearly 400x earnings), that’s not a good sign.

Uber has gotten crushed in the software apocalypse. It’s off more than 25% from its peak in September, and its forward PE multiple is now about 20, slightly lower than the S&P average. I mean, Uber’s just a better company and growing faster than the average S&P company. Because of the catastrophizing around AI, there’s more opportunity right now in the markets than I’ve seen in a while.

I believe SaaS is a great buy right now because people underestimate how lazy consumers are. If you have an Uber account, Uber has your credit card; you’re used to the interface. Uber has a huge advantage in that it has custody of 200 million consumers. Uber going vertical and partnering is really smart. Dara Khosrowshahi has proved himself to be one of the more deft leaders of big tech.

Tesla is in trouble. Not only is Tesla years behind Waymo in terms of their commercial robotaxi service, but their vehicle sales are falling off a cliff. Last year, Tesla lost its spot as the world’s top EV maker to BYD after posting its second-straight year of sales declines. Despite all of this, Tesla still trades at a price-to-earnings ratio that is more than 20x higher than most auto companies.

Many have ascribed Tesla’s rich valuation to something called the “Elon premium,” a phenomenon that describes Tesla investors’ willingness to pay outlandish sums in exchange for Musk’s “charisma and vision” at the helm of the company.

With SpaceX’s IPO on the horizon, Tesla’s “Elon premium” will finally disappear. Investors will no longer need to pour money into a pig with lipstick on — a declining car company masquerading as an AI business, a robotaxi business, a humanoid robot business — just to get exposure to Elon. SpaceX will offer a far cleaner way to do that: a genuine high-growth, cutting-edge space and AI company, without the theater.

The private credit providers, Blackstone, Blue Owl, TPG, Apollo, etc., are going to outperform the market.

The best thing about the Citrini paper is that it inspired an enormous drawdown, and now the market is pricing risk more aggressively than current earnings trends justify. That presents an opportunity.

The news cycle is faster than ever, and it’s harder than ever to find political coverage you can actually trust. That’s why Scott Galloway and Jessica Tarlov are bringing Raging Moderates to you five days a week — breaking down the stories that matter, without the partisan theatrics. Find new episodes here, or wherever you get your podcasts.