American life is getting more expensive again. Last month’s Consumer Price Index (CPI) came in at 3.8%, the highest reading in three years. Wholesale prices just posted their largest gains in four years. Gas is now averaging $4.54 a gallon, up 52% year-over-year. Diesel is over $5.60. Airline fares are up 20.7%. Amazon just added a 3.5% surcharge on everything shipped through its platform.

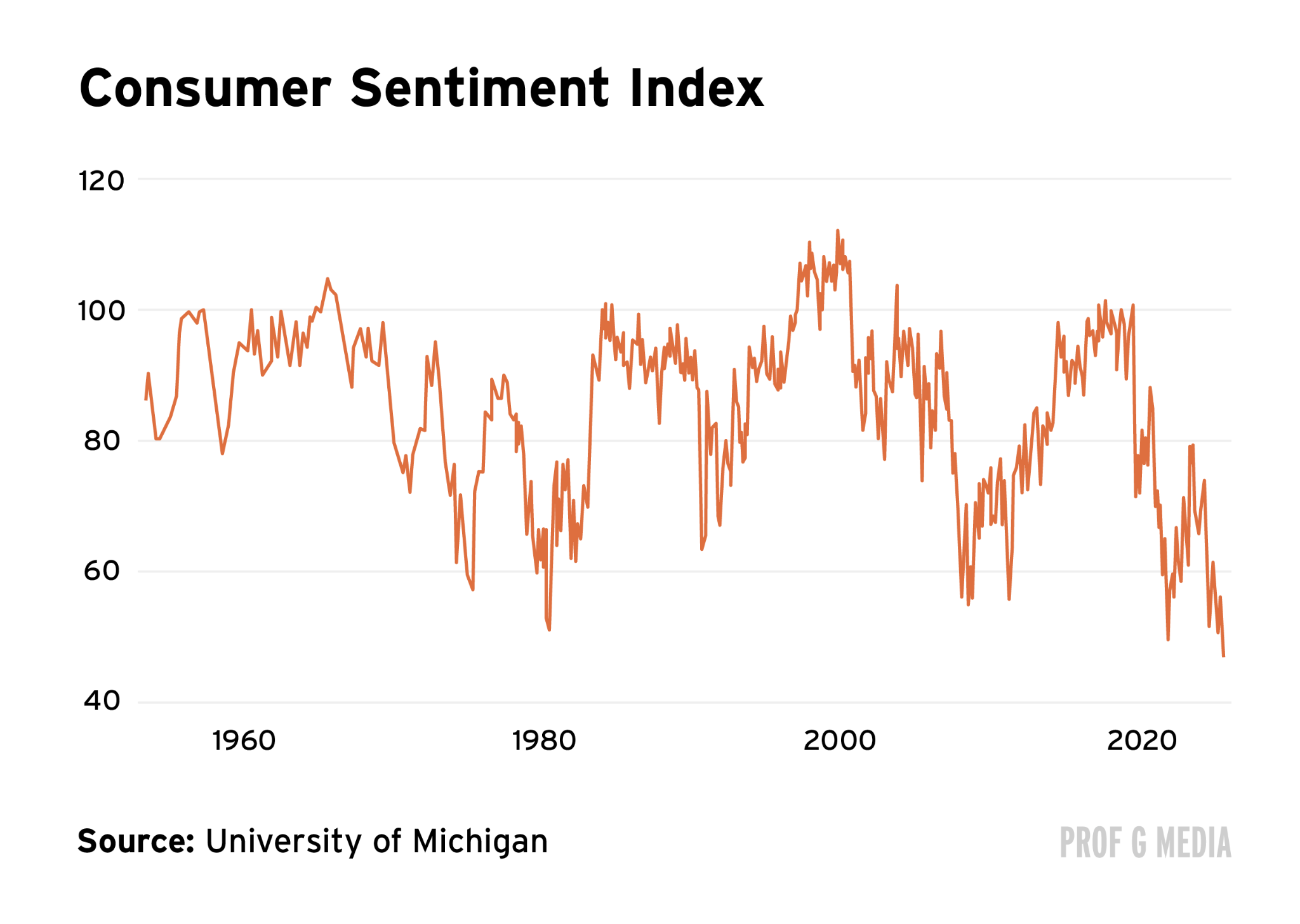

In previous months, wages rose faster than inflation. That’s no longer true. Real average hourly wages fell last month for the first time in three years. As a result, consumers are not happy: The University of Michigan consumer sentiment index just hit its lowest level in recorded history.

Two forces are driving this pain: 1) Tariffs: It’s estimated Trump’s tariffs cost the average household $1,000 in 2025 – a figure set to rise to $1,300 this year. 2) The Iran War: Since Operation Epic Fury began, the price of goods like oil, fertilizer, and food has exploded – price hikes costing the average American household $410 a month. Undo these actions and prices will moderate over time. Carry on and they’ll continue to rise. This momentous decision lies in the hands of one man. Last week, President Trump revealed the plan. In sum: Expect inflation to get worse.

Who Cares

For most Americans, inflation matters a lot. It’s the difference between saving vs. spending, vacationing vs. staying at home — and, for 34 million Americans, eating vs. going hungry.

But there’s one group who’ve decided inflation doesn’t matter at all: investors. Last week’s worse-than-expected inflation report had almost no impact on stocks. Aside from an initial dip, the highly inflationary war in Iran hasn’t made a dent either — the S&P 500 is up over 7% since the war began. Despite some initial bickering, investors have reached their final conclusion on the war and its price impacts: “We don’t care.”

Why don’t investors care about inflation? On its face, their reasoning is actually quite sound. While inflation is painful for consumers, it’s NBD for stocks. Technology companies now account for nearly half of the entire S&P 500 (the top ten make up 40%), and none of them are affected by higher gas prices. If the war made it impossible to ship, say, software then it’d be a different story, but it doesn’t. So, when it comes to consumer inflation, technology companies — and therefore, the stock market — are “insulated.”

Feels Like ‘22

I’ll cut to the chase: I disagree. Let me take you back to 2022, a year that looked eerily similar to today, and which ended up being the worst year for the stock market since the Great Recession.

As with 2026, our big problem in 2022 was inflation. It was also triggered by two major forces: 1) Covid, which blocked up supply chains, making it harder to ship goods around the world thus raising prices. 2) The Ukraine War, which resulted in Russia cutting off its oil supplies and driving up fuel prices around the world. (Side note: neither were self-inflicted.) Like bankruptcy, the crisis happened slowly then suddenly. U.S. inflation hit 4% in April 2021. Within twelve months it had doubled.

For the same reasons they aren’t too worried today, investors weren’t too worried then. Per a March 2022 Baird report, the tech industry offered “very limited direct exposure to higher input prices.” Conventional wisdom was that consumer inflation doesn’t hurt the stocks that matter (tech).

But then … something strange happened. Meta reported their ad business was slowing. This was surprising but not awful. Then came their cardinal sin in Q2: For the first time ever, the company’s revenue declined.

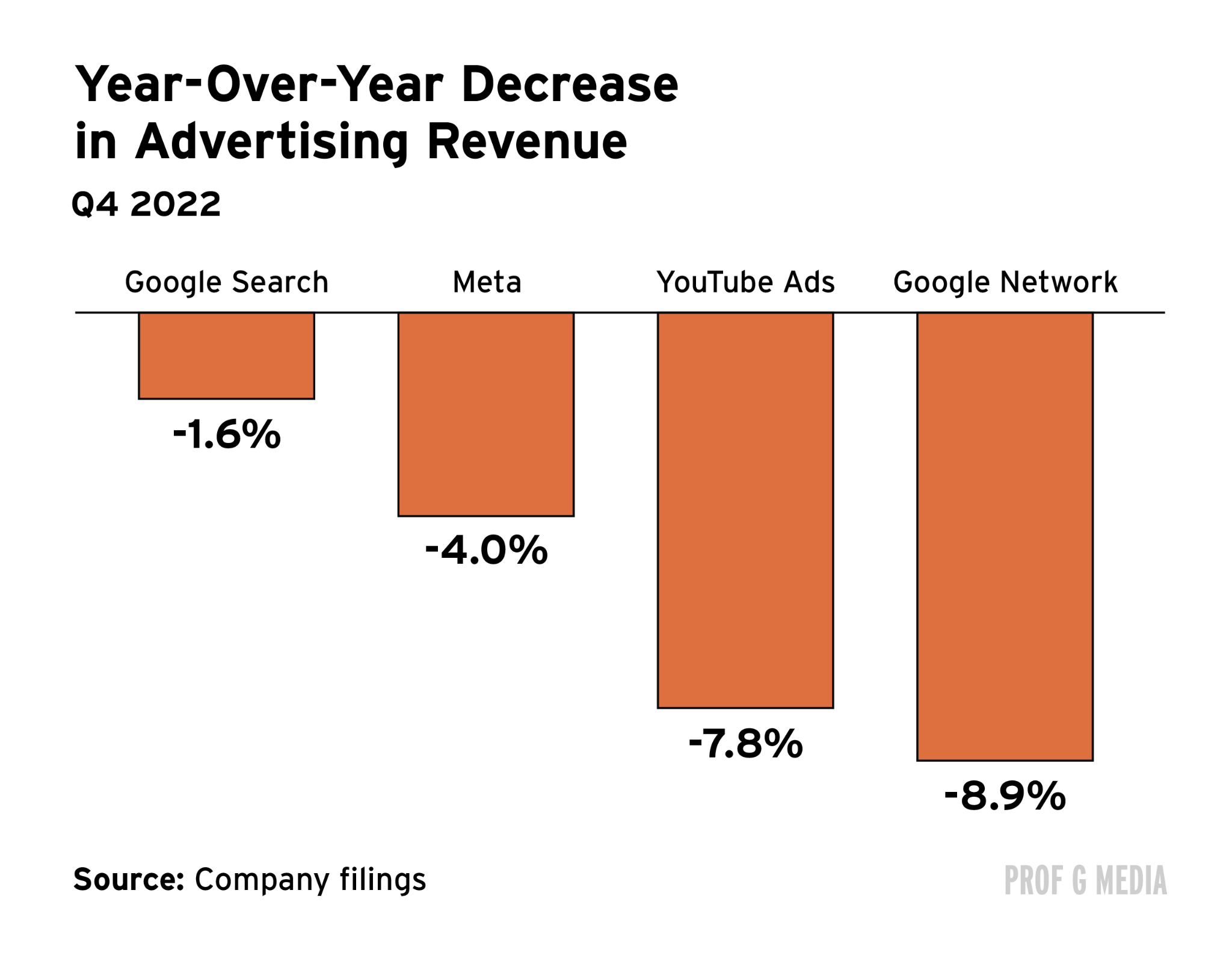

What seemed impossible soon became standard. Meta later reported that ad revenue had fallen even further. Snap’s revenue flatlined. YouTube’s revenue shrunk. Google’s search business went into decline, as did the company’s ad network. The digital ad market was collapsing, and the biggest victim was Big Tech.

Why did this happen? Meta’s 2022 SEC filing lays it out perfectly: “As macroeconomic pressures reduce the likelihood of consumer purchases of discretionary goods and services, advertisers are more likely to reduce their spending as they anticipate a lower return on investment.” In other words, consumers were spending less (due to inflation), which caused advertisers to spend less too, which … hurt Big Tech.

It was at that moment we realized how unprotected tech companies really are, as they rely heavily on advertising. Ads make up almost a tenth of both Amazon and Microsoft’s business. For Google, about 75%, and for Meta … almost 100%. Most of us already knew that less advertising meant less Big Tech revenue. What we forgot, however, was that less shopping also meant less advertising. As a result, Big Tech was a victim of inflation. Their pain just showed up further down the chain.

The hit to equity markets was enormous. Google stock fell 38% that year. Amazon fell 49%. Meta, 65% The Nasdaq dropped 30%, its worst year since the dot-com crash. The tech industry was brought to its knees by none other than the thing it was supposedly impervious to. And here we are again, calling markets “insulated.”

Chain Reaction

You can see how this might all play out today: Tariffs remain intact. The Strait of Hormuz remains blockaded. Oil prices continue to rise. Higher freight costs lead to higher wholesale costs, which lead to higher retail costs. Consumer spending starts to fall. Ad budgets get restricted. Instagram CPMs decline. Big Tech revenues go from double-digit growth to single-digit growth to no growth at all. With each falling domino, a step-change in Mag-7 multiples. And then … boom: bear market.

You might say this year won’t look like 2022 because of AI. You might say we’re less dependent on digital advertisers because of, say, Nvidia and Broadcom. That’s true, but remember who Nvidia and Broadcom depend on: digital advertisers. Meta, Google, Amazon, and Microsoft make up nearly half of Nvidia’s revenue. Fifty percent of Broadcom’s revenue comes from five (unnamed) companies. It’s widely agreed that three of them are Google, Meta, and TikTok.

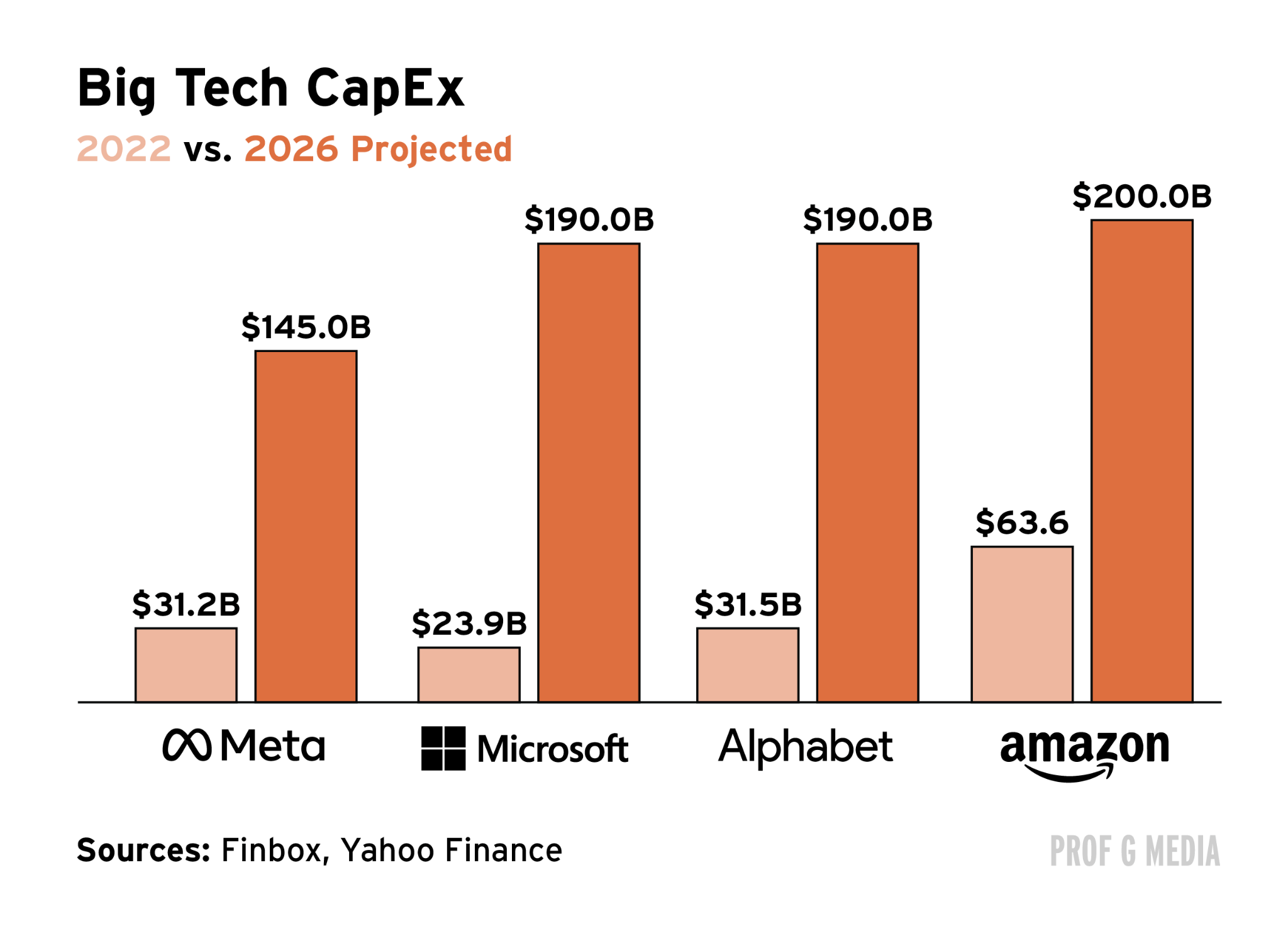

You might then argue that lower ad revenues don’t necessarily mean Big Tech won’t spend big on Nvidia chips. History suggests otherwise. One of Meta’s first moves after they reported bad earnings in 2022 was to reduce CapEx by about 13%. Amazon did the same thing. Google went from 30% CapEx growth to 2%. It became known as the “Year of Efficiency” — three words that would make Jensen Huang throw up if he heard them today.

We’re actually more dependent on these companies in ‘22. AI spending drove two-thirds of GDP growth last quarter. It’s expected to make up 40% of earnings growth in 2026. America is a giant bet on AI — or, more specifically, a giant bet on Big Tech spending gobs of money on AI. Do anything to change that, and portfolios could go kaput.

Hut Hut Hike

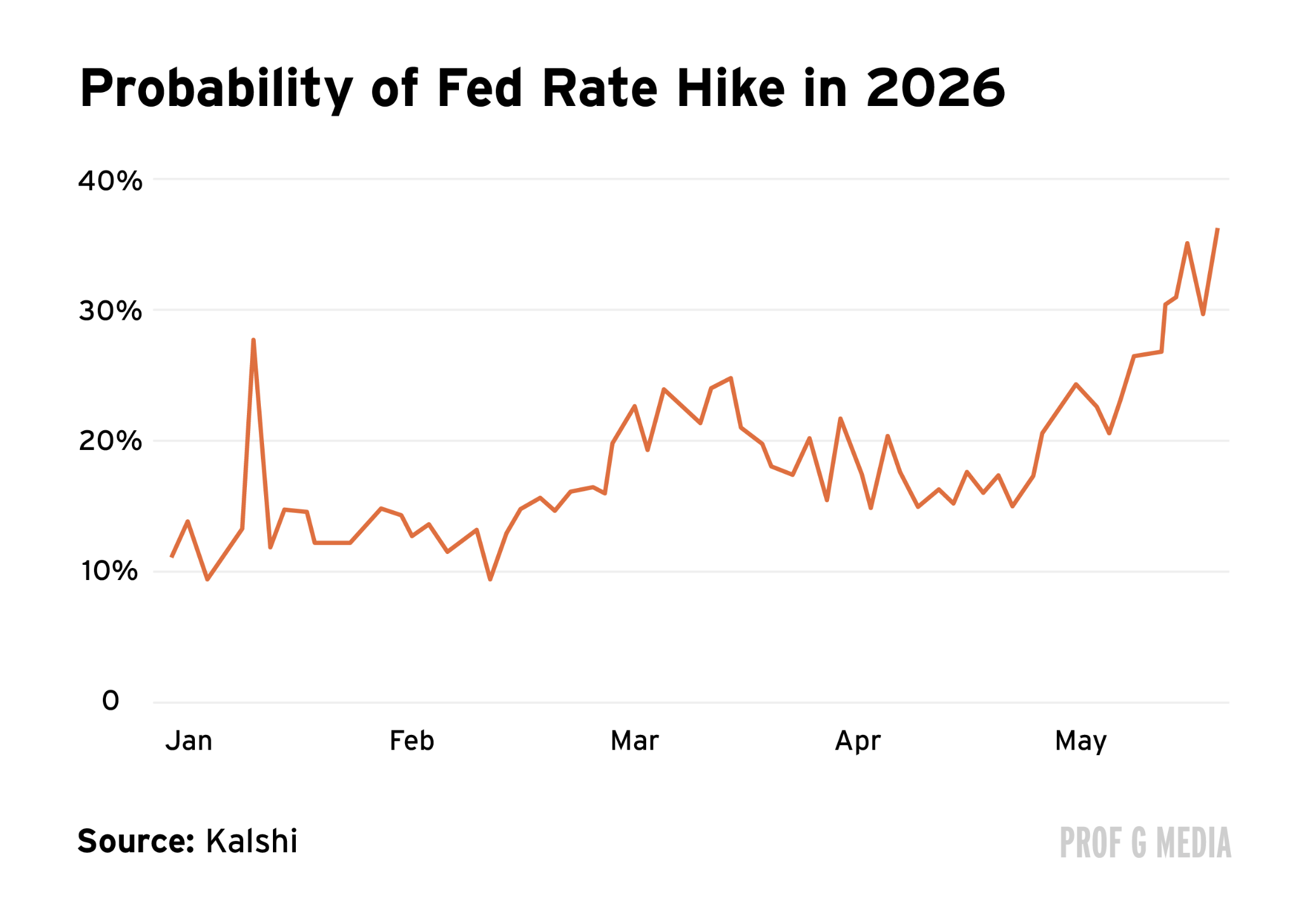

Inflation is already starting to break down the original bull thesis for 2026. Going into the year, we all agreed we were entering a lower interest rate environment. It wasn’t necessarily our reason to be bullish, but it was certainly our reason not to be bearish. Ever since we bombed Iran, however, that argument has collapsed. It’s unlikely we’ll see any cuts this year, and after last week’s inflation print, the chances of a rate hike rose to 37%. Rate hikes hurt stocks in ‘22 — they could hurt them again this year too.

I’m not saying any of this is inevitable — I’m simply saying it’s possible. So far investors have disregarded this fact.

Optimists

The big question: Why are investors telling themselves the same story they told in 2022?

On the one hand, there are various scenarios in which a 2022-like bear market would not play out. Maybe the Iran War will come to a swift conclusion. If not, maybe consumer spending will stay resilient in the face of inflation. If not, maybe ad budgets will keep growing anyway. If not, maybe Big Tech will keep spending like there’s no tomorrow. Lots of ifs, lots of maybes … but it’s all possible.

Ultimately, however, I don’t think investors are all too interested in these questions, because they know getting rich largely comes down to one thing: optimism. Almost no one has gotten rich shorting the market. Even fewer have gotten rich not investing in the market. The truth is, there’s simply more money to be made when stocks go up — and it’s the investor’s job is to imagine every which way that could happen. Investors are, by definition, optimists.

Are they right? Over the long term, yes. The S&P 500 has risen 107% since its 2022 low. The Nasdaq has risen 153%. While stocks do go down, generally speaking, they go up. That is the prevailing thesis driving markets right now, and though it might sound dumb, it’s true.

Learning

It’s late, I’m tired, and I have several podcasts tomorrow morning that I’m not prepared for. The more I consider how little time I have, the more anxious I become. My brain is telling me they won’t go well.

At the same time, though, most of my podcasts have ended up fine. Actually, better than fine: According to my podcast app, my latest is the 49th most-downloaded episode in the country. Come to think of it: If I had to put money on it, I’d bet tomorrow’s recordings will go well. Why wouldn’t they?

I’m learning.

See you next week,

Ed

Ed, while I understand FUD sells (especially podcasts!), I worry you get down and depressed delivering that message.

I recommend listening to this Carter Family tune every morning to balance that dark side.

https://youtu.be/UrI_ZAkgHBI?si=Q97nxEFiY1DUsXs2

Investors are not worried because they now know that if things get bad enough the government will step in to stabilize things. Regular people will buy more things on credit until they can't pay, rather than downgrading their lifestyle. If things get bad enough and defaults start affecting the banks, well, the government will backstop that too. Our capitalism with airbags will not let pain become too bad any time a crisis starts to brew. Not saying this is a good thing but that's what we've been trained to expect.