Is SpaceX Really Worth $2 Trillion?

Plus: Nike’s struggle continues, and OpenAI buys TBPN

$23 million

That’s how much the toilet in NASA’s Artemis II spaceship cost to develop.

Is SpaceX really worth $2 trillion?

Nike’s struggle continues, and Allbirds is closing all its U.S. stores

The most underrated lesson from the OpenAI-TBPN deal

Newsletter Exclusive: Why is America turning away doctors when there’s about to be a shortage?

SpaceX’s IPO Could Make Musk the World’s First Trillionaire

SpaceX has confidentially filed with the SEC for what could be the largest IPO ever. The company is targeting a $2 trillion valuation and could raise up to $75 billion in the offering, which could come as soon as June.

If the IPO prices are as expected, Elon Musk’s 40% stake in SpaceX, in addition to his other holdings, will make him the world’s first trillionaire.

SpaceX is by far the most dominant player in the largest ever addressable market: the cosmos. It controls two-thirds of the satellites orbiting Earth, accounted for 85% of all U.S. space launches last year, and operates at one-fifth the cost of its closest domestic competitor.

Some perspective: NASA’s Space Launch System rocket that jettisoned astronauts on a path around the moon last week has launched twice since its development in 2011; SpaceX’s Falcon 9 rocket has launched more than 640 times. The Falcon also cost half as much to develop.

SpaceX generated $8 billion in profits in 2025 off of roughly $16 billion in revenues, and analysts expect sales to increase 25% this year. A $2 trillion valuation would imply a 125x price-to-sales multiple.

SpaceX’s out-of-this world valuation sent ripple effects through the broader space economy. These only intensified when, on Thursday, the FT reported that Amazon is in advanced talks to acquire the satellite telecom group Globalstar for roughly $9 billion. Satellite services stocks Planet Lab, Viasat, EchoStar, and Rocket Lab closed the week up 29%, 22%, 18%, and 15%, respectively.

Is this an amazing company or is it ridiculously overvalued? The answer is yes.

This man of the people bullsh*t where Elon is reserving 30% of the shares for the retail investors? He’s doing that because retail investors are the only ones stupid enough to pay this price. Institutions weren’t going to cover the allotment here.

Research shows that IPOs that allocate directly to retail investors lose over 60% of their value, on average, within a year, underperforming their peers by about 20%. Why? They’re priced more aggressively, and retail trading platforms push shares and hype companies up, leading to big IPO spikes.

If this thing gets out anywhere near a $2 trillion valuation, you do not want to be in this stock three, six months out. Even Musk and his jazz hands can’t figure out a way to justify anything resembling this valuation.

This company bundles SpaceX, Starlink, xAI, and X. It’s very hard to understand what the right valuation is because there’s a lot of bullsh*t — but also a lot of substance.

That complexity is by design. Musk bundles enough ambitious far-horizon narratives such that investors cannot build a clean model and they just have to trust him. This valuation requires you to believe his whole pitch perfectly, across the longest possible timeline.

When Google went public, it was trading at 10x trailing revenue with revenue growth of 240%. SpaceX is going public at 125x trailing revenue, with revenue growth of 25%. So SpaceX’s revenue growth is almost 10 times lower than Google’s was, and yet its valuation is more than 10 times higher.

Nike Lost Hundreds of Billions. Allbirds Lost Everything

Two sneaker brands at opposite ends of the market are both running into trouble.

Nike stock tumbled 16% last week after reporting earnings. Net income fell 35%, gross margins compressed on the back of tariff pressure in North America, and management warned that revenue will decline for the rest of the year. Sales in China, one of its most critical markets accounting for 15% of global revenue, will fall 20% next quarter alone.

Investors are disappointed, and so is Nike’s CEO, Elliott Hill. Brought back 18 months ago to turn Nike around, Hill told employees in an all-hands meeting he is “so tired of talking about fixing this business.”

He still has a long way to go. Nike is valued at 1.4x sales — roughly the multiple it was trading at in 2009. Its market cap has fallen from almost $300 billion in 2021 to $65 billion today; Nike is now worth a third of what discount retailer TJ Maxx is.

Meanwhile, Allbirds, the wool sneaker brand that went public in 2021 at a $4 billion valuation, sold off its remaining intellectual property last week for $39 million to a brand management firm. The buzzy company, whose shoes were once deemed part of the Silicon Valley uniform, never turned a profit.

Allbirds was always a bad business. The VC community embraced it, which should have been the tell. It had a fashionable product, expensive retail leases it could never sustain on unit economics, no wholesale infrastructure, and no brand loyalty. When the hype faded, there was nothing underneath it.

Nike is a completely different conversation. This is still one of the greatest consumer brands in the world. Whether you are watching football in Ghana or badminton in the U.K., that Swoosh means something.

Elliott Hill has only been back 18 months, and he should be given three years. But I think he’s got the wrong strategy. Something that Aswath Damodaran told me that always struck me is that we’re obsessed with youth, and growth companies never want to accept that they’re aging into mature companies.

Nike has not recognized that it’s a mature, low-growth company. It’s time to cut costs. For every dollar in expenses you cut, it has the same impact on the bottom line as $5 to $6 in incremental revenue.

Which do you think is easier right now? What investors need to hear is a margin story: flat revenues, costs cut 4% to 6% a year for three years, low-double-digit EBITDA growth. That almost certainly means 10,000 to 20,000 layoffs are coming, and an activist will show up and force this if leadership will not. This is a $70 to $80 stock — if there is an adult in the room.

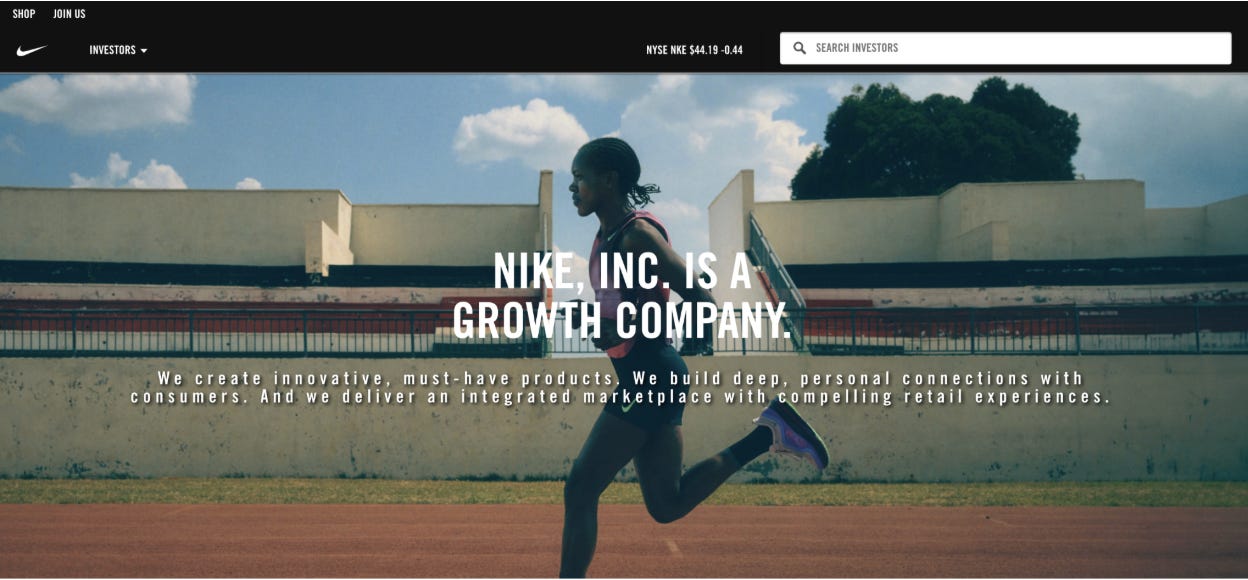

One thing that has always struck me on Nike’s investor relations homepage is that the first thing you see is “Nike is a growth company” in huge letters. It’s been that way for years. That’s like their main pitch to investors: We’re a growth company. And, well, definitionally, you’re not because your revenue has fallen every quarter for more than a year.

sponsored content

“AI is making scammers’ lives easier

Your name, address, phone number, and financial info are traded online for as little as $5. Scammers, identity thieves, and AI-powered fraudsters can buy this data to target you.

Generative AI is making these scams more difficult to spot until it’s too late.

But here’s the catch: they can’t scam you if they can’t find you.

Incogni Unlimited eliminates the fear of your personal details being found online. The data removal service automatically removes your data from the databases that scammers rely on.

Try Incogni and get 55% off with code PROFG”

sponsored content

Can TBPN Make OpenAI Cool?

In its buzziest acquisition to date, OpenAI acquired tech-industry talk show TBPN last week. According to a source familiar with the transaction, the acquisition was valued at approximately $200 million.

Founded just 18 months ago by entrepreneurs John Coogan and Jordi Hays, TBPN has become a media staple for fans of the tech industry, and a platform for CEOs like Mark Zuckerberg, Satya Nadella, and Alex Karp.

The caliber of TBPN’s guests creates a flywheel effect: High-profile guests attract other high-profile guests, which attracts high-profile viewership.

This in turn attracts premium advertising dollars. With only 11 employees, TBPN generated $5 million in ad revenue in 2025 and was on track to exceed $30 million in 2026. They will no longer run ads, but as a house publication for OpenAI, they effectively become a marketing platform.

TBPN’s revenue per employee, assuming $30 million in sales, is greater than Apple’s.

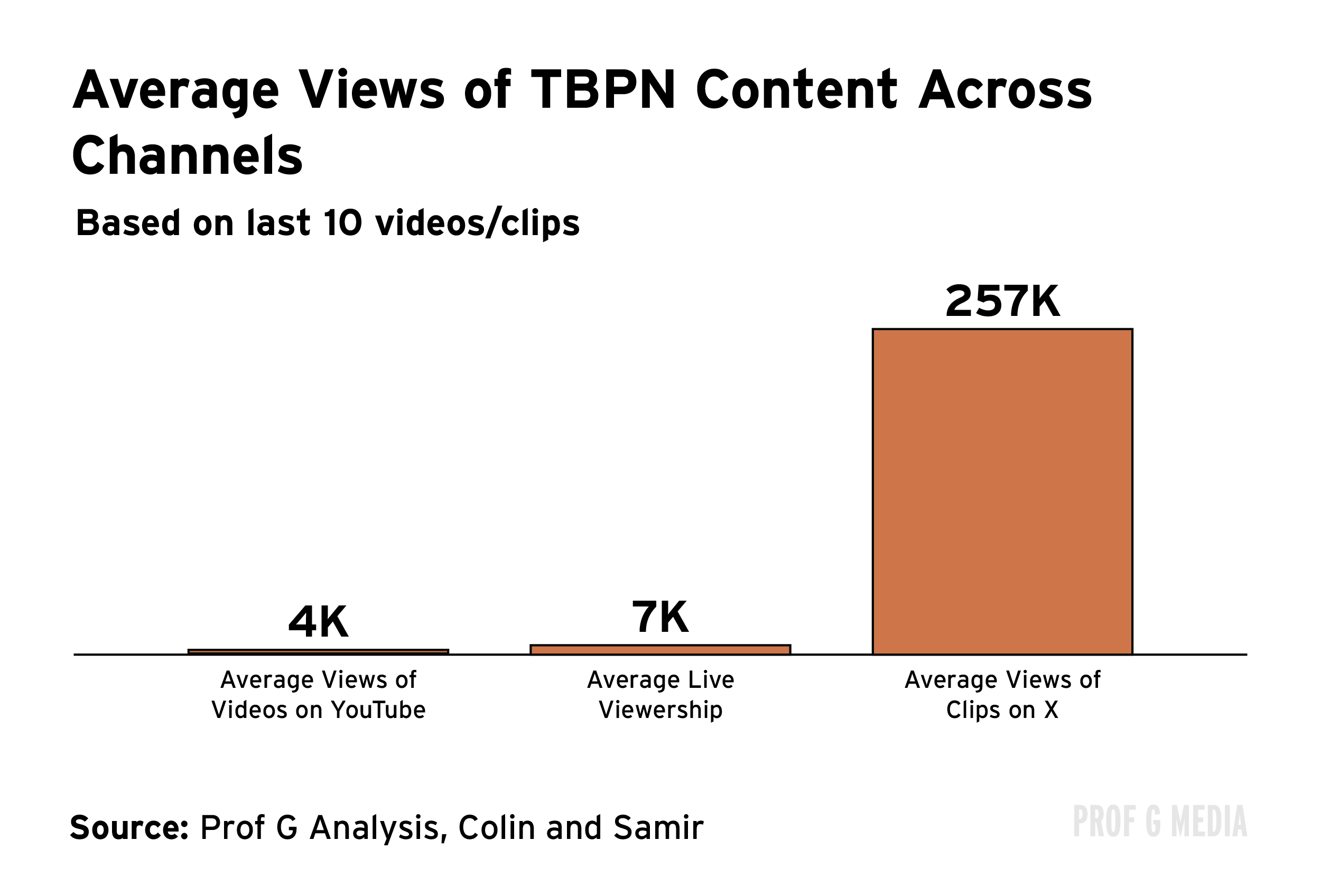

TBPN livestreams from YouTube and X for three hours a day, five days a week. Most episodes get between 4,000 and 10,000 live viewers. Most of its influence stems from clips on X. It’s both a reinforcement of X’s continued cultural gravitas and a reminder that clips are no longer just a marketing requirement. The clips are the content.

OpenAI’s decision to purchase a media company isn’t entirely surprising. There is a long history of tech companies buying or starting media firms as a marketing and customer acquisition strategy. Microsoft and NBC started MSNBC in 1996 to drive traffic to Microsoft’s internet portal, MSN. Bloomberg launched Bloomberg News to sell its terminals, and retail trading platform Robinhood acquired MarketSnacks and launched Sherwood News, a tech-focused media outlet.

OpenAI’s move follows an old strategy, but there is a new lesson we can learn from this deal.

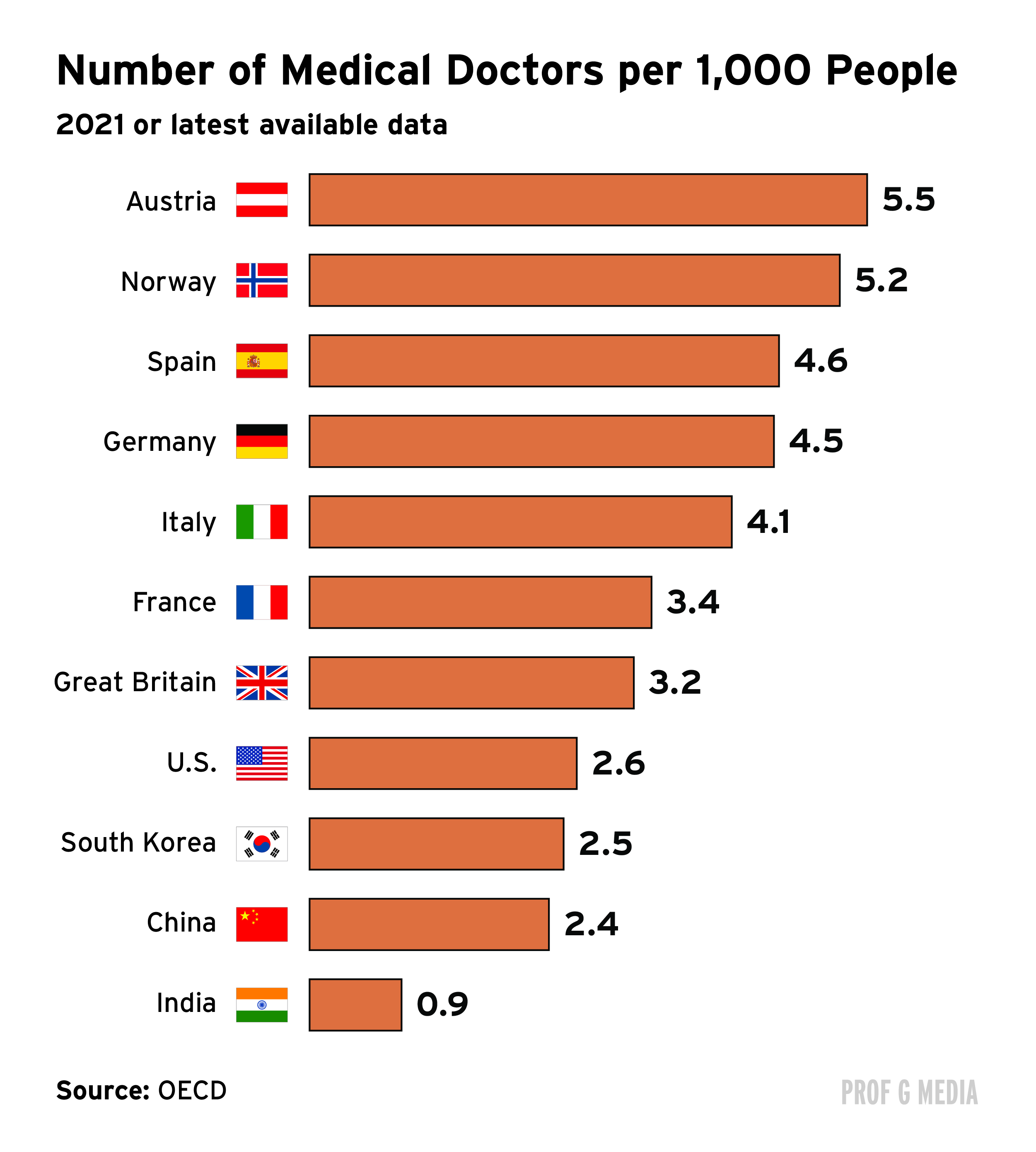

America Is Running Out of Doctors. It’s Also Turning Them Away

The richest country on the planet has a problem: It’s running out of doctors.

More than 80% of U.S. counties are medical deserts, meaning areas with too few physicians to meet demand. By 2037, the U.S. will have a shortfall of 87,000 primary care providers. In other words, between 130 and 175 million Americans — almost half the country — could lack a primary care doctor.

But here’s the confusing part: We have no shortage of people who want to become doctors. Every year, medical schools turn away roughly 30,000 applicants, some exceptionally qualified.

Last year, American medical schools rejected about 25% of applicants who scored in the top-10th percentile.

Today, the chance of a premed freshman becoming a doctor is just 6%.

First, Medical School

Before a medical student spends a dollar on tuition, they’ve already spent $7,400 on preparation and admission expenses. Most apply to 16 to 18 schools; some apply to as many as 30. Ambitious students have to, because the most competitive programs’ acceptance rates range from 2% to 10%. Some are even lower. Stanford admitted 1.0% of applicants. NYU? 0.5%.

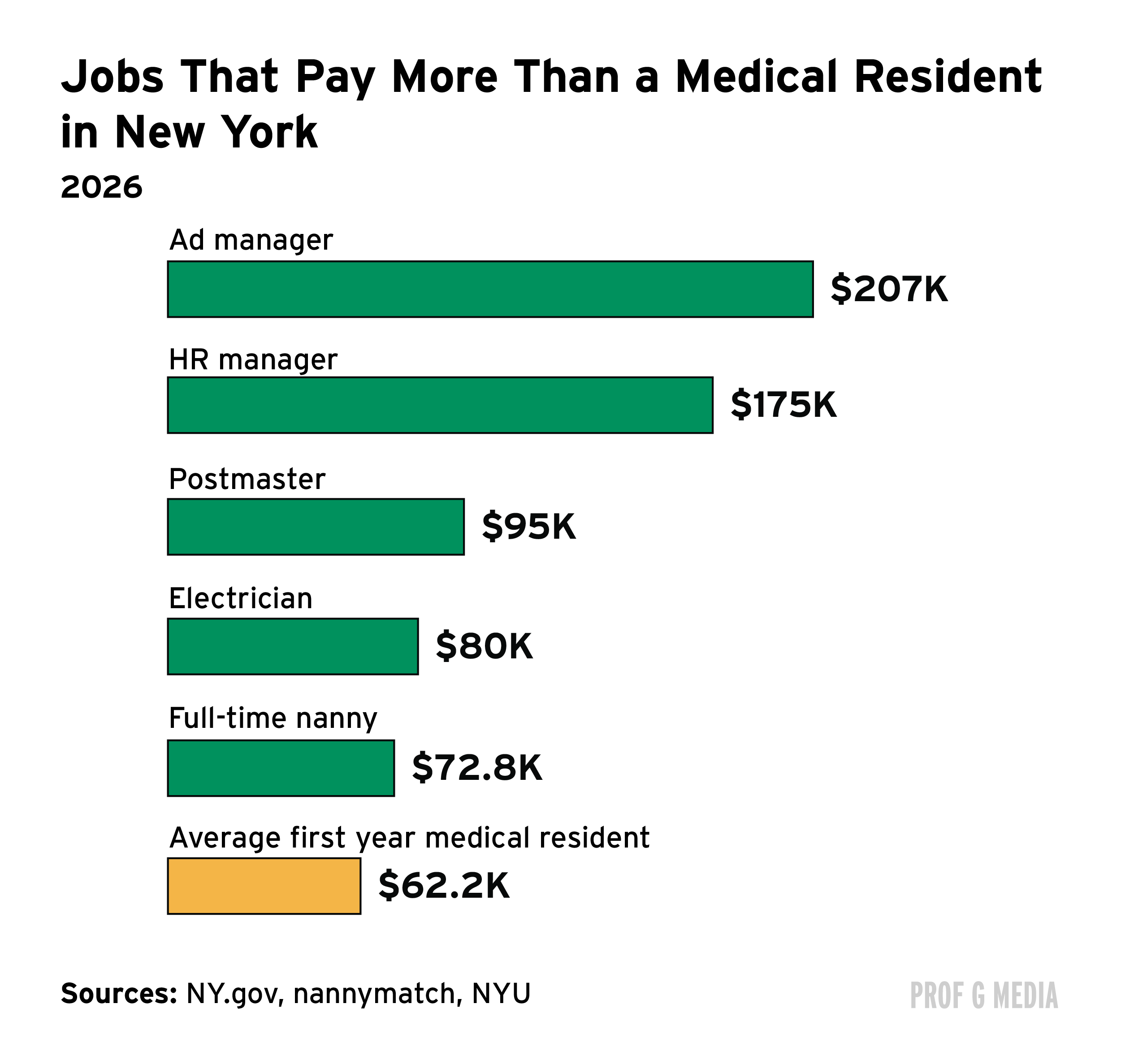

After four grueling years of medical school, graduates have to apply for residency. Residency is a mandatory, post-graduate training period that lasts between three and seven years. During this period, they work 80-hour weeks and make, on average, $62,200.

The Residency Bottleneck

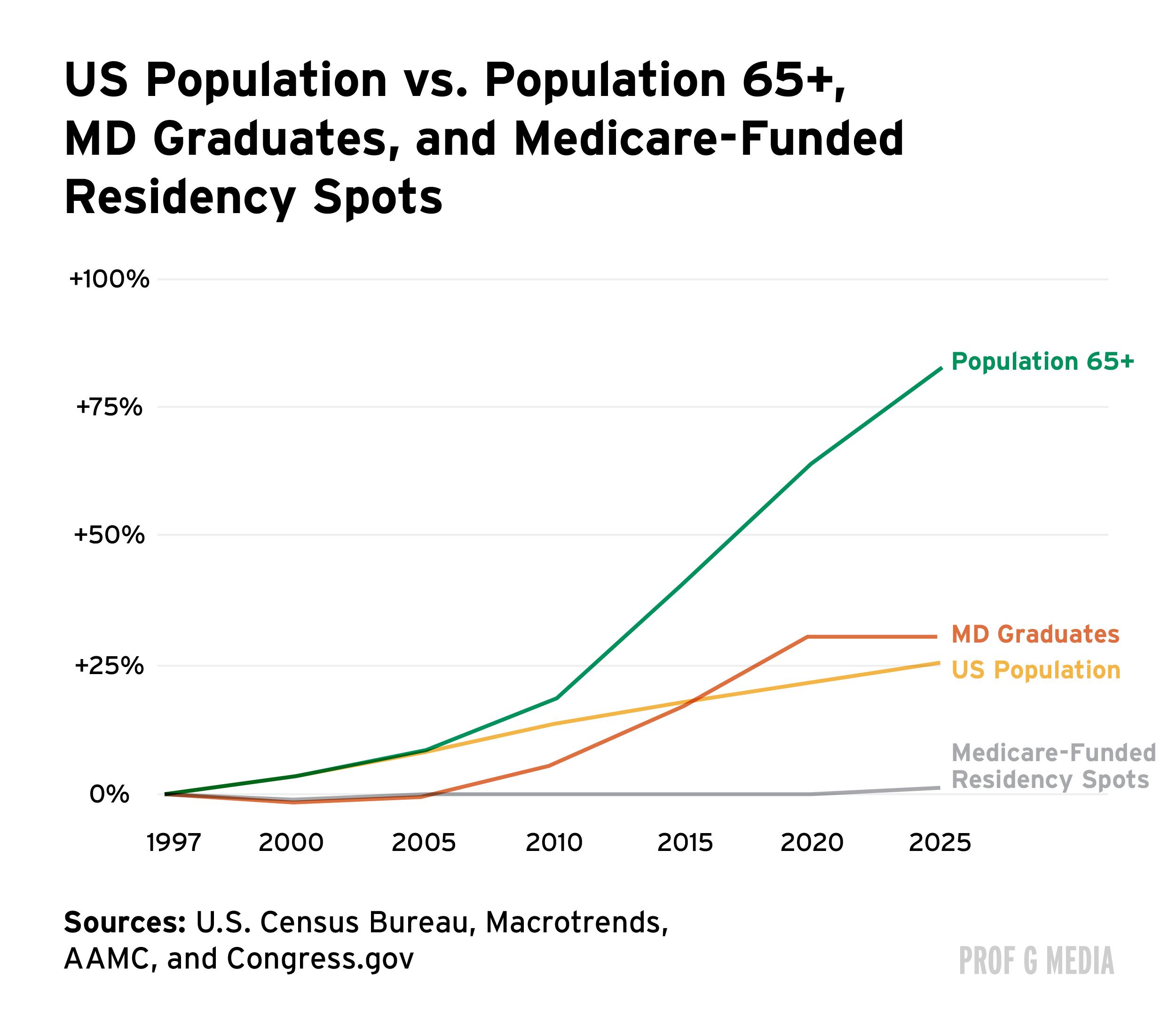

Over the past three decades, the federal government has increased the number of residency spots by only roughly 1%, while the U.S. population has increased nearly 30%.

Seventy percent of teaching hospitals fund their own residency slots, but they can’t keep up with demand — and disproportionately fund spots for lucrative specialities where they can recoup the cost through billing, not where the shortage is worst (primary care and rural medicine).

This has created a bottleneck where medical schools are reluctant to increase enrollment because there aren’t enough residency slots. It’s not a good look for very expensive schools to be graduating lots of unemployed MDs. The consequence is that they reject thousands of qualified applicants.

Shaheen Lakhan, M.D., Ph.D., explained that this residency gridlock is a policy choice, not an inevitability. “We have, in effect, added more cars to the on-ramp without building new lanes on the highway.”

It’s Expensive to Save Lives

The average medical school graduate has paid more than $370,000 for their undergraduate and doctoral degrees. More than 70% of graduates carry debt; the average owes $223,130. It takes most of them two decades to be debt-free.

On July 4, 2025, President Trump signed the “One, Big, Beautiful Bill Act” into law, enacting sweeping changes to federal loan programs that will impact who can afford to pursue medicine.

Starting July 1, 2026, professional degree students (including medical, dental, and law students) will be limited to borrowing $50,000 per year and $200,000 over a lifetime. Grad PLUS loans — which allow grad students to borrow up to the entire cost of attendance minus federal aid — will be eliminated entirely.

As a result, many students will be forced to bridge the gap with private loans, or not finish at all.

The Surplus That Never Materialized

How did we get here? It all started back in the 1980s, when people weren’t concerned about a shortage of doctors. In fact, they were concerned about a surplus. The Graduate Medical Education National Advisory Committee report projected in 1980 that the U.S. would have 70,000 more physicians than it needed by 1990.

Policymakers responded accordingly: Scholarships were scaled back, residency training requirements were tightened, and medical schools agreed to a voluntary moratorium on new institutions that lasted from 1980 to 2005.

The most consequential legislation came in 1997: Congress passed the Balanced Budget Act, which capped the number of residency slots that Medicare would fund, freezing support at 1996 levels.

The surplus never materialized. The models failed to account for demand driven by population growth, aging, and expanded insurance coverage. By 2005, the Association of American Medical Colleges had reversed course entirely, acknowledging that the U.S. was now in shortage territory.

America’s rapidly aging population only intensifies this crisis. The number of Americans 65-plus is expected to double by 2060. The 85-and-older population, which requires the most intensive care, is expected to triple by 2060.

We are woefully unprepared to care for them: Only 44% of geriatric medicine residency spots were filled in 2025. That’s largely because geriatricians earn half of what cardiologists do. Primary care physicians make even less than geriatric physicians on average.

At the same time, roughly 20% of practicing physicians are 65 or older, and those between ages 55 and 64 made up another 25% of the active workforce. Realistically, more than a third could retire in the next decade.

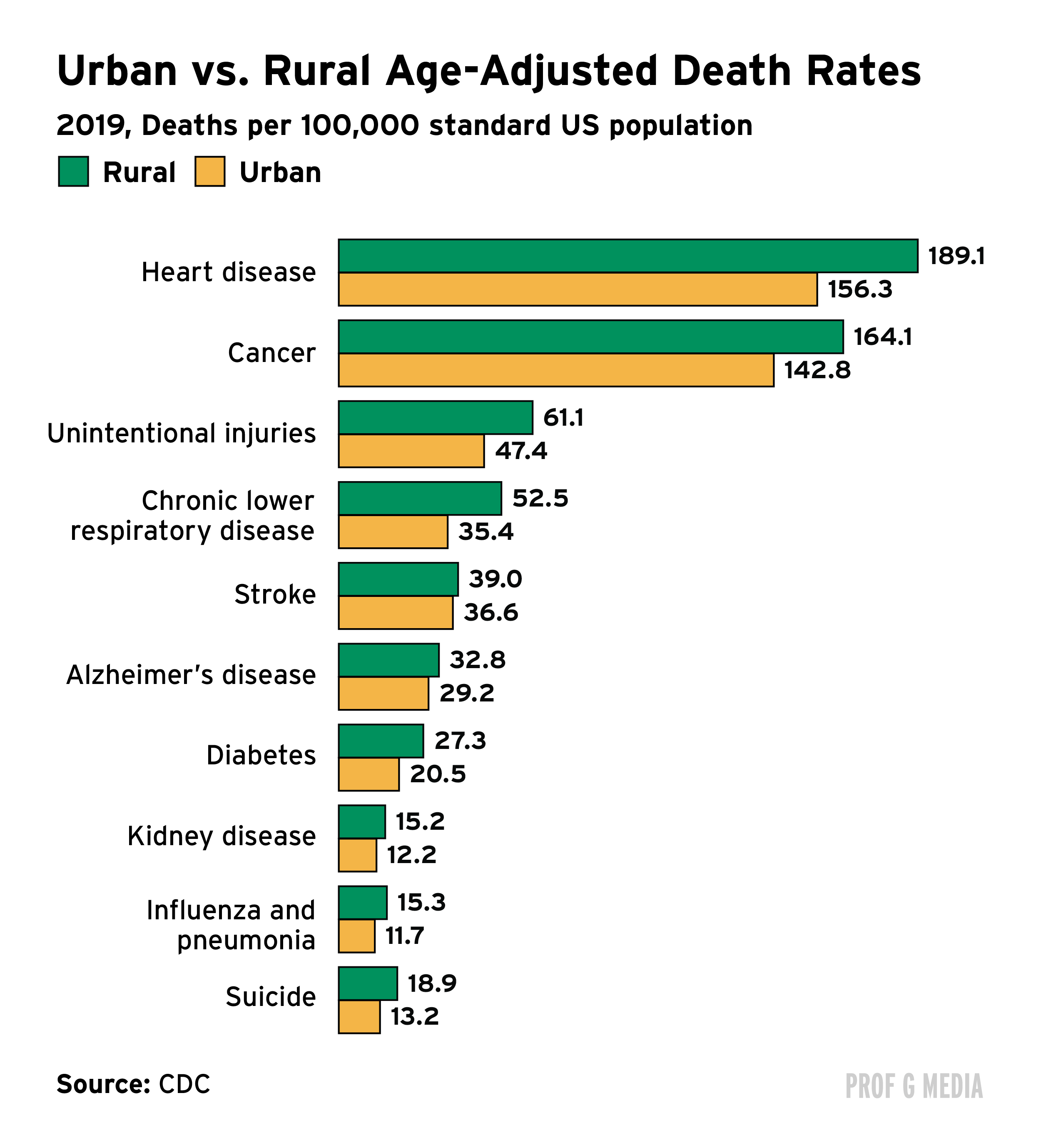

Geography as a Preexisting Condition

The shortage of doctors is already affecting rural America. In 2020, only 2% of Medicare-funded training slots were in rural areas, despite rural communities representing 18% of the U.S. population.

Part of the problem is student preference: Only 3% of residents finishing their training say they would prefer to practice in a community of 25,000 or fewer.

This asymmetry has lethal consequences. Rural residents face dramatically worse health outcomes across nearly every major disease category.

It’s gotten worse over time: Prime working-age mortality in rural areas was 43% higher than in urban areas by 2019 — a stark increase from just a 6% difference in 1999.

Access to care is a major driver of these disparities. A 2025 Brown University study found that in rural counties, adding just one primary care physician is associated with 1.4 fewer deaths per 100,000 older adults, a benefit 37 times larger than the same addition would yield in urban areas.

Solutions

The physician shortage is not a mystery, nor is it a demographic accident. It’s the downstream consequence of a policy decision that has never been meaningfully reversed.

The political path forward exists. The Resident Physician Shortage Reduction Act of 2025 would add 14,000 new Medicare-supported residency positions over seven years and codify the Rural Residency Planning and Development Program. It has bipartisan support, but it has not passed.

Without action, the shortage of doctors will only get worse — and every year that we fail to address this problem, another class of qualified applicants is turned away from medical school.

The SpaceX IPO might get a pop, but it will not stay anywhere near a $2 trillion valuation.

Is Partiful fixing the loneliness epidemic? Ed interviews Shreya Murthy, Partiful’s CEO and co-founder.

No. It is another shell game. Tesla is sinking fast, got to spin something else up to keep up the illusion.

Investors should not forget about "China, China, China" that always seems to come spoilt the fun. Without Chinese EVs, Tesla could be biggest car company in the world. And X / Twitter if without TikTok or US AI companies without Chinese DeepSeek & gang. Not forgetting kungfu humanoids robots.

The Chinese companies may be now well behind SpaceX, and few US, European and Indian companies come close. But I wouldn't bet my retirement fund that the Chinese space companies don't do another EV on Tesla.