You’ve probably seen some alarming headlines about a crisis brewing in private credit. In recent weeks, investors have tried to pull their money out of private credit funds including Blue Owl and Blackstone, raising questions about how these vehicles work, and what happens when people head for the exits all at once.

It also raises a more basic question: What exactly is private credit anyway? Prof G Markets exists to inform, entertain, and educate — so in that spirit, this week’s exclusive is a simple guide: private credit for dummies nonfinance bros.

What is private credit?

When you think of a company taking out a loan, you probably picture the loan (credit) coming from a bank like JP Morgan, Bank of America, Wells Fargo, etc. That’s what happens most of the time.

But in some cases, if companies want faster, more customized loans, they can turn to private credit. Private credit refers to tailored, often higher‑interest loans that specialist investment firms — like Ares Management, Blackstone, Apollo Global Management, and Blue Owl Capital — make directly to companies, instead of those companies borrowing from a traditional bank. It’s a fast‑growing but still relatively small segment of the corporate debt market.

When did this party start?

The modern private credit market expanded in the wake of the Great Recession of 2008. In response to the crisis, regulators raised capital and risk management requirements on big banks, making it harder for them to lend money to less-established borrowers. This created an opportunity in the market for less-regulated lenders.

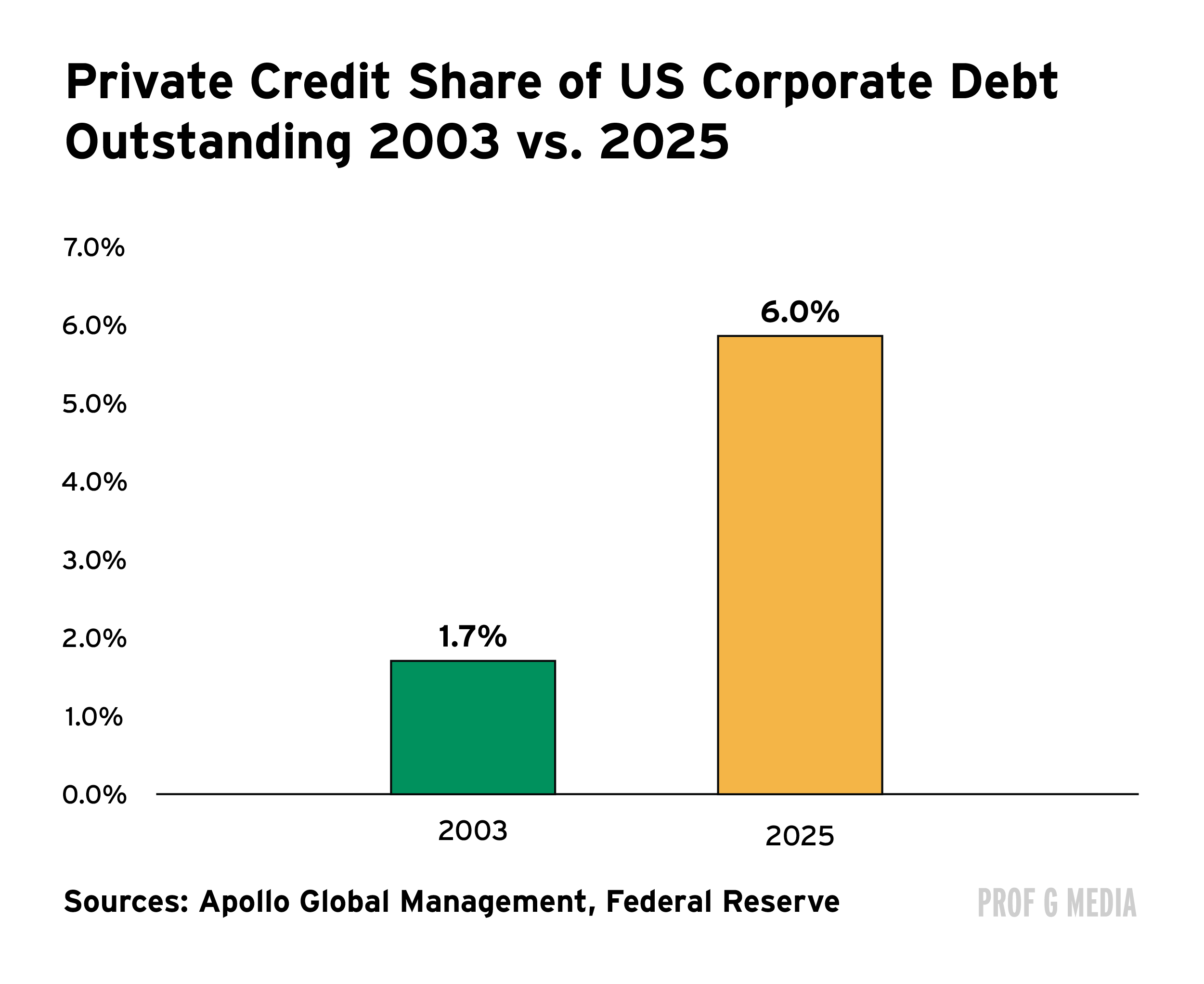

In 2007, private credit funds had $108 billion in assets under management (AUM) globally. This year, AUM is expected to exceed $2 trillion.

A Quick Guide to Credit Lingo

Direct lending: a loan made directly to a company by a private fund

Floating-rate loan: a loan where the interest rate changes over time (usually every month or quarter) based on a benchmark rate. Payments go up when rates rise and down when they fall. Most private credit loans have floating rates.

Covenant: rule in the loan agreement that the borrower has to follow — like limits on taking on more debt or requirements to keep certain financial metrics in a healthy range.

Business development company (BDC): private credit fund for retail investors: They operate like closed-end mutual funds (meaning that unlike mutual funds, they don’t accept new capital after they’re formed) and are often publicly traded.

Dry powder: uninvested capital committed by investors to private credit funds

Principal: the original sum of money borrowed by a company or investor, excluding interest and fees

Yield to maturity (YTM): the annualized rate of return an investor is expected to earn if a bond is bought at its current price and held until its final due date.

The ecosystem

The private credit ecosystem has three main players: the private credit funds (like Carlyle, KKR, Apollo, etc.), the limited partners (those who invest in the private credit funds), and the businesses (who take out the private credit loans).

Private credit funds

Historically, most private credit borrowers have been small to mid-sized companies, ranging from $3 million to $100 million in EBITDA. But as private credit funds have attracted more capital from institutional and high-net-worth investors, they’ve started to underwrite bigger and bigger loans. This increased lending capacity has helped fuel the growth of private companies; before, if a large firm needed to raise a ton of money, it would go public. Now, it can turn to the private credit markets.

Private credit has also become a popular source of funding for big public companies that want flexible terms and to diversify their sources of financing.

This is increasingly applicable for Big Tech. Though the biggest tech companies can generally borrow cheaply in public bond markets, there are certain benefits to private credit financing, namely, flexible terms. Instead of traditional corporate debt that would show up on companies’ balance sheets, arrangements with private credit funds can be structured such that most of the debt sits in separate legal entities called special purpose vehicles (SPV).

For instance, Meta announced a $27 billion financing deal with Blue Owl in which most of the debt sits in an SPV.

The largest investors in private credit funds are institutional and wealthy investors, including pension funds, family offices, and sovereign wealth funds.

Investors are drawn to private credit because it has historically offered a higher return than traditional fixed-income strategies like Treasurys or traditional corporate bonds. It can also improve portfolio diversification, giving investors exposure beyond the public markets.

Retail investors are increasingly participating in private credit through business development companies. BDCs represent about 14% of the private credit market.

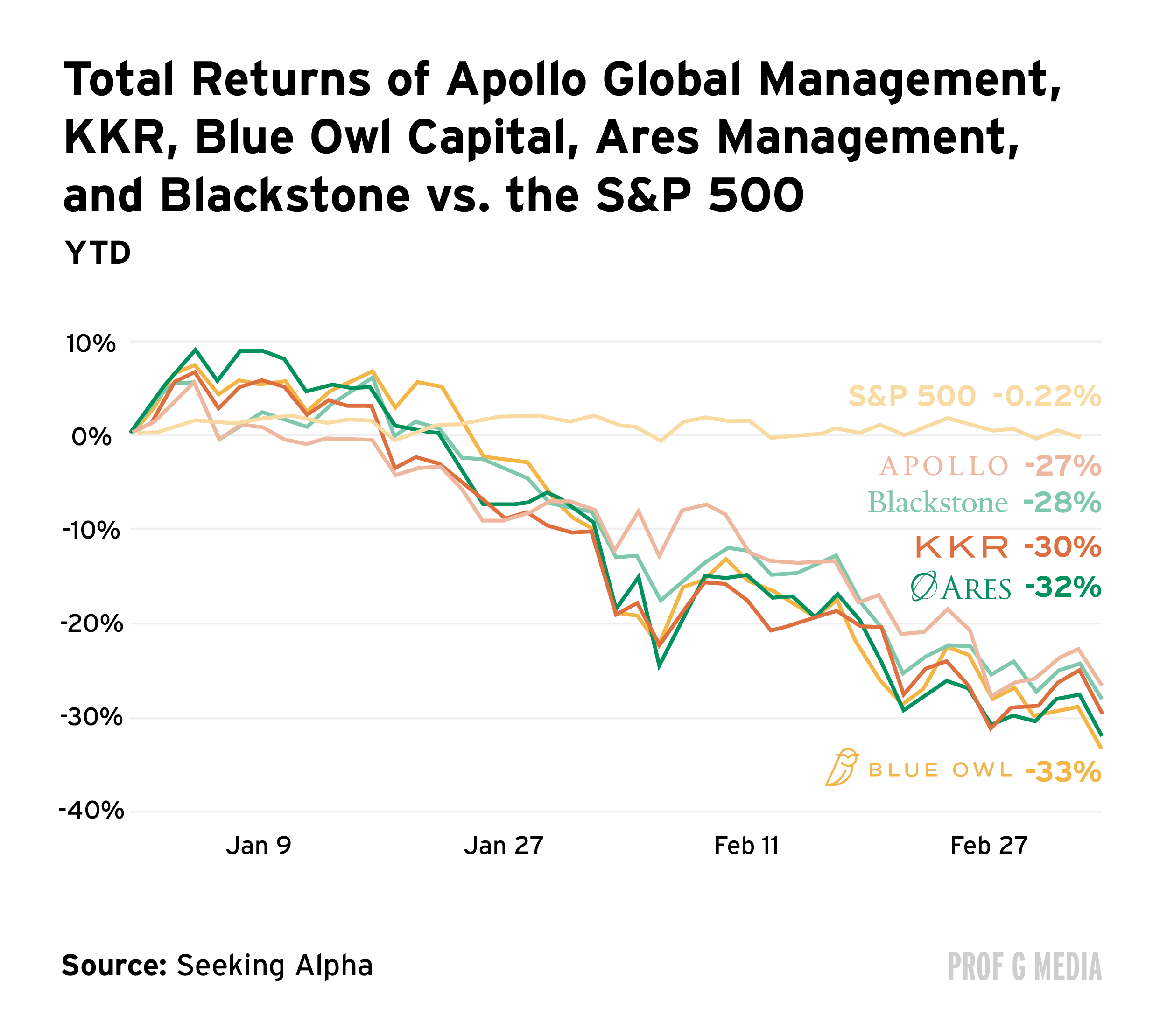

Private credit firms have gotten crushed recently. Why?

Private credit firms have had a rough 2026.

Over the past few years, lending to software companies has become a significant part of private credit portfolios. Now, investors fear that if AI weakens software firms’ businesses, they could default on their private credit loans. Earlier this month, UBS researchers estimated up to 35% of private credit portfolios faced elevated risk of AI disruption. This could hit retail investors, too: Technology firms account for approximately 24% of holdings at BDCs.

This risk is making investors nervous, and they’re starting to ask for their money back. This creates a whole separate problem. Redemptions are typically allowed on a schedule, but when requests surge all at once, private credit firms aren’t typically liquid enough to return all of their capital (investor money is tied up in long-term loans). If funds refuse withdrawals, that makes investors even more nervous.

That’s what happened late last month at Blue Owl Capital’s BDC: After redemptions spiked, the firm decided to “shut the gates” on the fund, preventing investors from pulling their cash.

Executives claim that these current challenges are merely “hiccups,” not a signal of crisis.

Others warn that investors have good reason to be concerned. “People made choices: If you wanted a higher dividend, you could take more risk,” Mark Rowan, CEO of Apollo, said recently. “That felt really good on the way up. That’s not going to feel so good on the way down.”

Rowan’s quote highlights a vulnerability that isn’t unique to private credit. After almost two decades of most assets going up and to the right, many investors — consciously or not — have come to expect that’s how things will continue. When they’re reminded that risky assets can also go down, the first crack spurs a race to exit doors that nobody thought they’d ever have to use.

Also, thanks for the great explainer. Very helpful and appreciated.

Scott has highlighted private credit companies like Apollo and Blue Owl as potentially undervalued. It would be great to hear if his thoughts have shifted given the most recent panic moves by investors in this sector.