In a few weeks’ time, Elon Musk’s SpaceX will go public. The IPO has been described as a “once-in-a-generation market event,” and for good reason: At a roughly $2 trillion valuation, it will be the largest IPO in history.

The go-public may also make Elon Musk the first trillionaire, pushing his net worth to roughly 3.6% of the GDP of the U.S. (the richest American ever). At $2 trillion, SpaceX would be the seventh-most valuable company in the world, more valuable than Meta, Walmart, JPMorgan, and even Tesla.

That’s why I was anxious to read SpaceX’s IPO filing, the first real look into the company’s financial statements, which finally dropped late last week. At 277 pages, the document is longer than The Great Gatsby and The Catcher in the Rye. And while not as captivating, it might be more consequential than either of those novels, as the words on the page will be the determinant of trillions of dollars.

This post is an examination of the SpaceX filing. To be blunt: It’s a trainwreck. Unserious, empty, hallucinatory, and borderline dishonest. I’m not exaggerating when I tell you I was shocked to see what I saw. So let’s get into it.

Hopeium

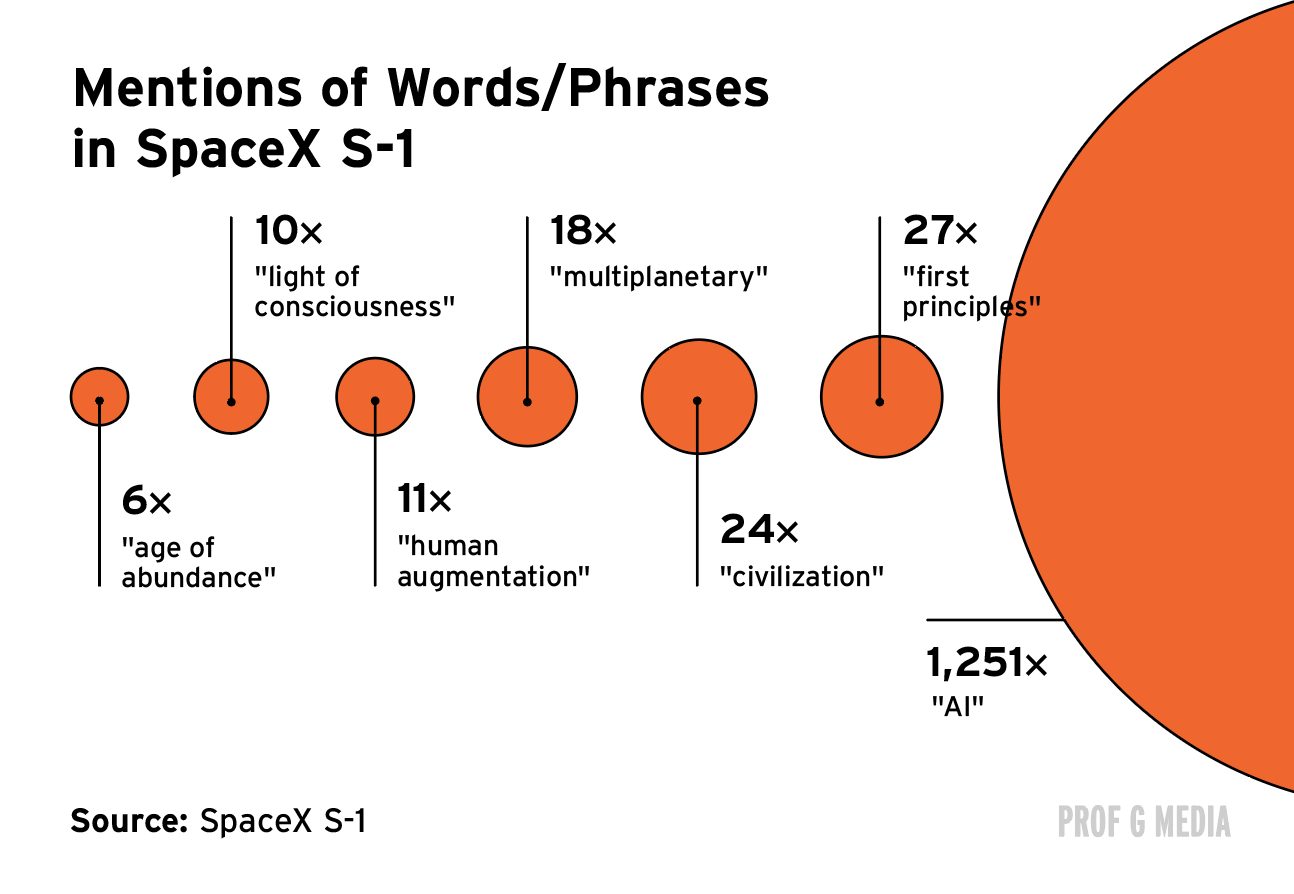

The trouble starts at the very beginning of the document. After eighteen images of rockets in space, we learn that the company’s mission is “to extend the light of consciousness to the stars.” To accomplish this, the company plans to advance humanity “to Kardashev Type II status,” which is defined in the document as “a civilization that harnesses the full energy output of its local star.” Only a few pages in and it’s already starting to feel like an ayahuasca trip.

We soon learn that psychedelic language is part-and-parcel of the pitch. “The light of consciousness” (sounds like WeWork’s old slogan?) is mentioned ten different times in the document. Meanwhile “human augmentation” is mentioned eleven times, and “first principles,” twenty-seven times. AI gets a mind-boggling 1,251 mentions — more features than the word “Jesus” gets in the Bible.

SpaceX-stasy

Once you arrive at the financials you start to realize what the language is overcompensating for: awful numbers. The company generated $4.7 billion in Q1 2026, up only 15% from the year before (very low for an “AI company”). It also lost $4.3 billion, up 700% from the year before. That means the company is spending roughly twice as much as it makes (and on pace to explode those losses even more), while growing its topline six times slower than Nvidia and two times slower than my own podcast. There’s no getting around it — these numbers are terrible.

But it gets worse when you compare those numbers to last year’s. Revenue grew 33% in 2025, meaning the business has actually started to decelerate. Meanwhile net losses came in at $4.9 billion, so the company is on track to lose four times more money than it did last year. I’ll put it simply: slowing revenue + skyrocketing expenses = not good.

Pricing Problems

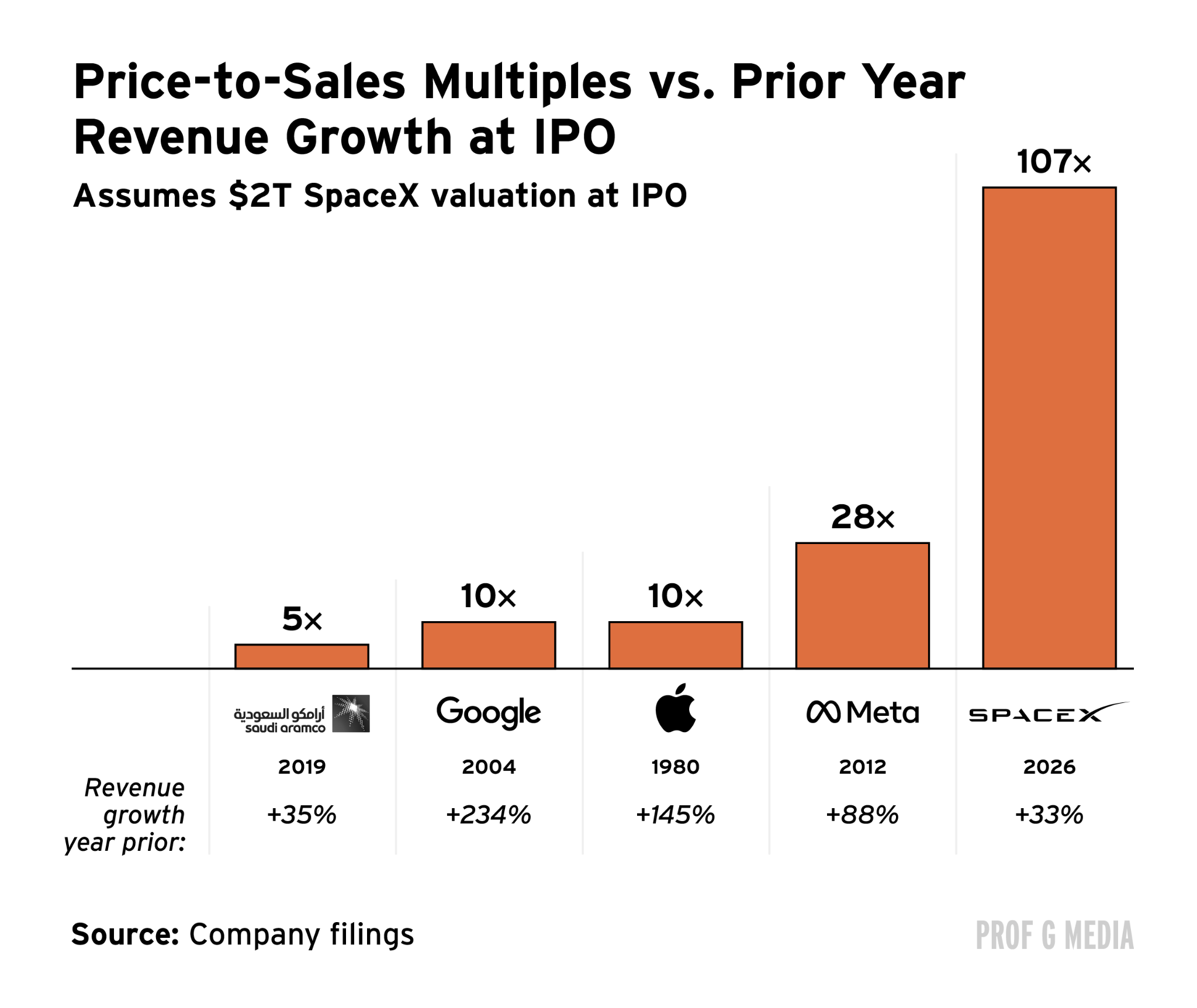

I’d have no problem with SpaceX’s sh*tty financials if they were reflected in the valuation — but they’re not. The stock is set to be priced at 107 times sales, which would make it one of the most expensive stocks in history. (The most expensive stock in the S&P 500 is Palantir, which trades at 64 times sales). It will be twice as valuable than Walmart while generating less revenue than Macy’s.

Maybe this is just the nature of blockbuster IPOs? No. Compared to previous go-publics, SpaceX’s valuation falls nothing short of insane. Meta went public at 28 times sales with 88% revenue growth. Google went public at 10 times sales with 234% growth. Put another way, SpaceX is growing seven times slower while asking for a multiple ten times higher. Pass me the crack pipe.

Ke-TAM-ine

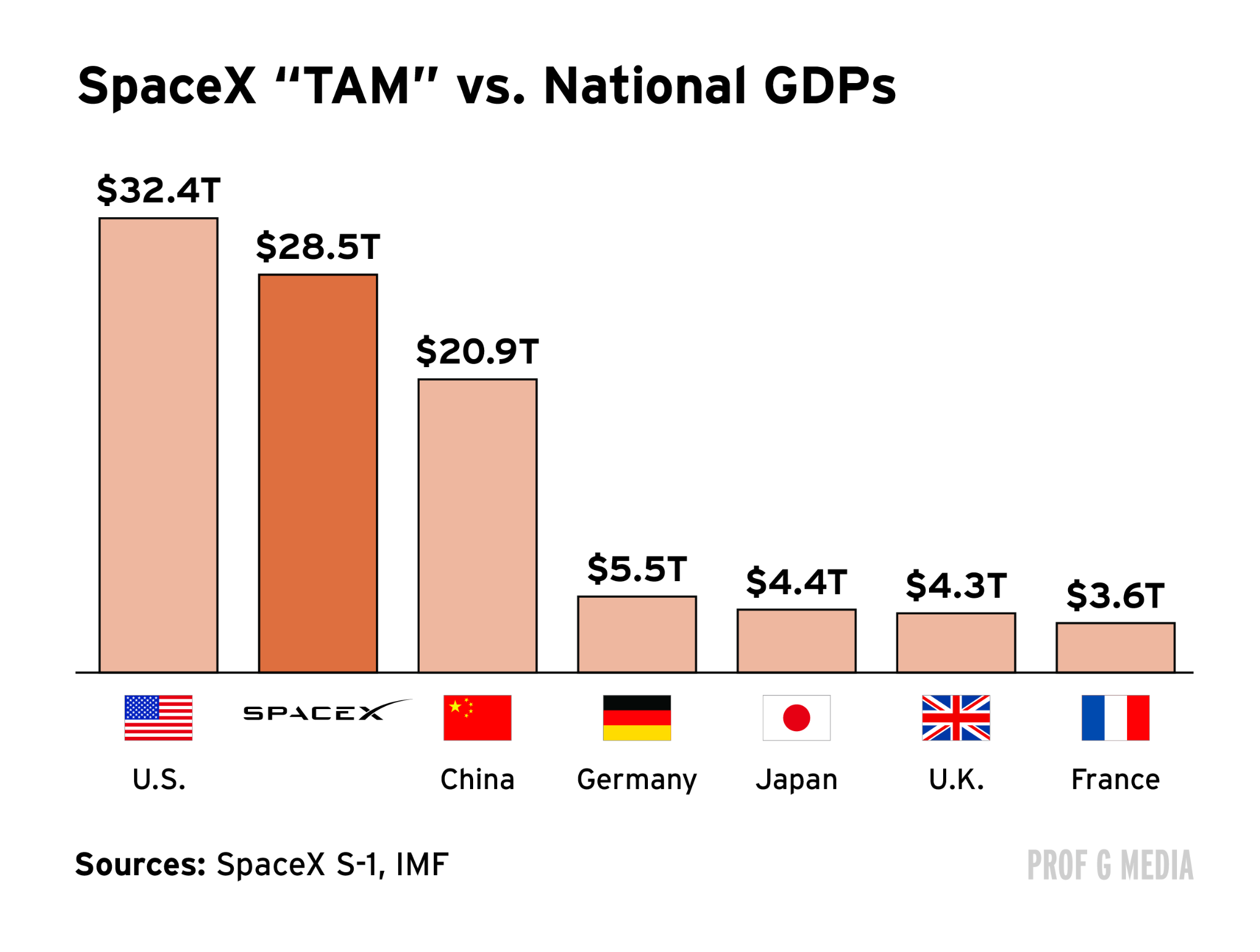

How did they reach such a stupid valuation? With stupid financial projections. SpaceX claims to have “identified the largest actional total addressable market (“TAM”) in human history,” worth (wait for it) $28.5 trillion. That’s larger than the GDP of Europe or China. If this sounds dumb to you that’s because it is.

It gets even dumber when you learn the company attributes less than $2 trillion of that TAM to space and satellites. Isn’t this a space company? Where’s that $26 trillion coming from? I’m asking the question but you already know the answer. Two letters: AI.

AI-huasca

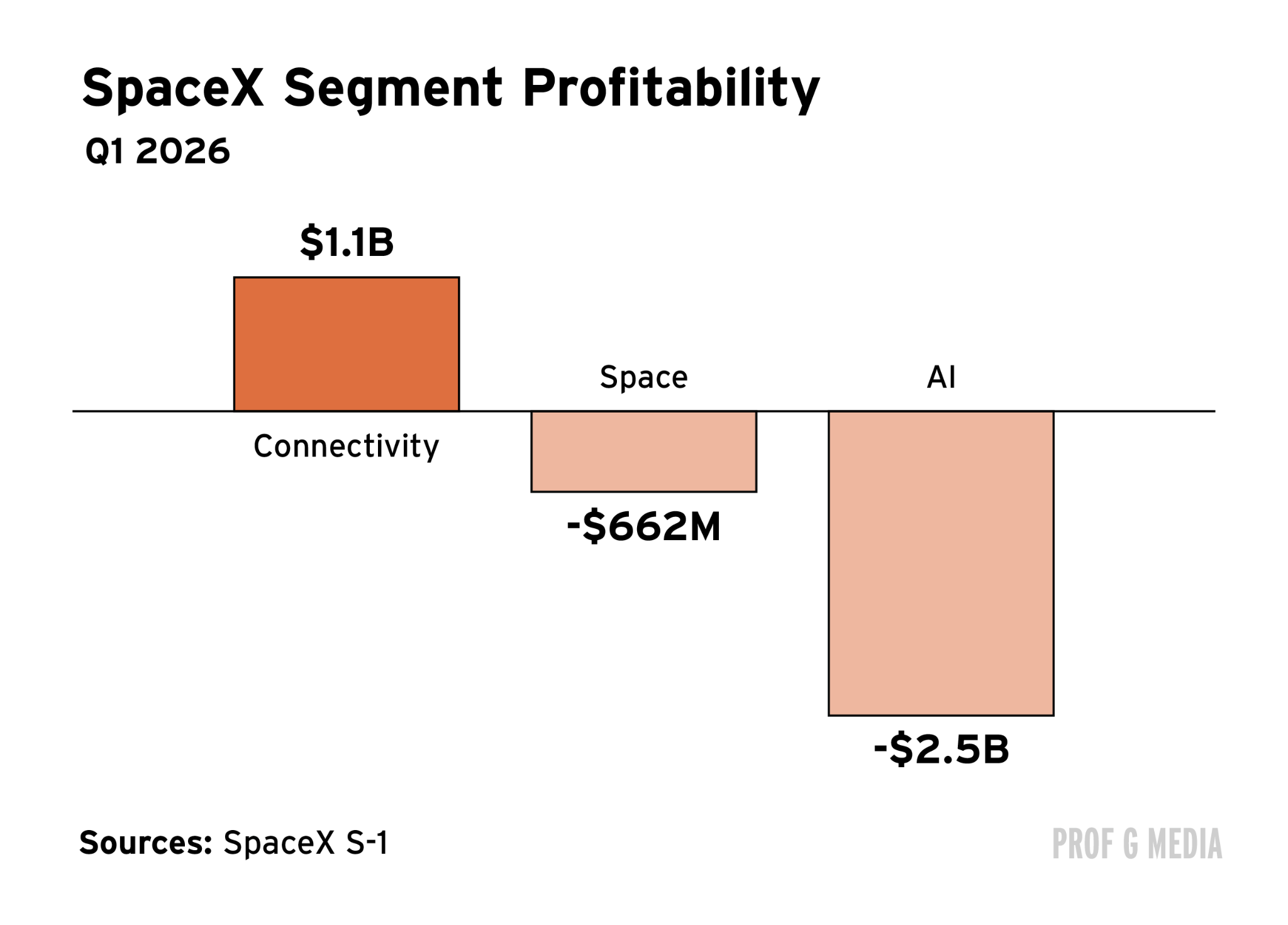

AI is where this business comes off the rails. While other parts of the business make sense, — such as connectivity (i.e. satellites), which generated more than a billion dollars in profits last quarter — SpaceX’s AI unit is essentially a giant sinkhole. The segment generated less than a billion dollars last quarter while spending more than three billion. Total AI losses for Q1 2026? $2.5 billion. That’s in addition to a ridiculous quarterly AI CapEx bill that came out to $7.7 billion. #MoneyFurnace.

Strangely, the AI unit was not part of the company until a few months ago, when SpaceX acquired Elon’s other startup xAI for an implied $250 billion. Why purchase this seemingly bad business? Because it spices up the sales pitch. SpaceX can now be sold not just as a “space company,” but also an “AI company.” It allows the company to increase its “TAM” by $26 trillion while expanding its multiple. In fact, the filing mentions AI 23 times more than space. This is an intentional sleight of hand trick to make it seem like the core business (building rockets) isn’t the core business.

EBITDon’t

Elon stans will argue SpaceX is profitable on an EBITDA-basis, which is true. The problem, however, is in the D and the A. While EBITDA can make sense for evaluating companies with low capital expenditures, it makes no sense for a company that builds rockets. The depreciation and amortization costs at SpaceX are gigantic — stripping them out in your financial analysis makes no sense whatsoever.

Exit Liquidity

So who will actually buy this thing? Management believes retail is the answer. SpaceX is reserving 30% of its shares for retail investors, three times larger than the average IPO. The expectation is that die-hard Musk fans will buy the stock no matter what — a bet on the “dumb money.”

The other big buyer will likely be you. Elon negotiated a “fast entry” deal with Nasdaq so that SpaceX will be automatically included in the blue-chip index. That means billions of dollars of passive money will automatically flow into the company as soon as it lists. In other words, if you own the Nasdaq, you’re about to own SpaceX.

Return To Earth

If we apply comparable market multiples to each of SpaceX’s three business lines (space, connectivity, and AI), we arrive at a sum of parts valuation of $550 billion. That would be a reasonable valuation of SpaceX. However, it’s roughly 75% less than the target.

The only way to get yourself mentally to $2 trillion is to believe that every possible sci-fi objective will be achieved, from data centers in space to asteroid mining to building cities on Mars. Once you’ve done that, you then have to convince yourself that each of those endeavors will also make money. There’s optimism, and then there’s delusion. As Patrick Boyle told us on the pod last week, SpaceX is more a science experiment than a business.

It’s a shame because I used to like this company. I’m fascinated by space travel and I believe we owe it to ourselves to better understand the universe. But there’s a time and a place for childlike wonder, and valuing companies is not that place.

Needless to say I won’t be buying the SpaceX IPO. Not until it returns to earth.

See you next week,

Ed

The "forced buyers" framing is exactly right, and a "the fix is in" analogy practically writes itself. Nasdaq didn't just bend its rules, it revealed what those rules actually were: Negotiable, for the right client. The seasoning period existed to protect passive investors from being force-fed freshly-priced shares before markets had time to discover a fair value. Waiving it doesn't just benefit SpaceX, it sets a precedent that OpenAI, Anthropic and every future mega-IPO will now expect as standard.

The circularity is the real scandal. SpaceX's $1.75 trillion valuation is partly justified by the near-certainty that tens of billions in passive money will flow in mechanically on listing day. The valuation inflates the index weight, the index weight triggers the forced buying, the forced buying supports the valuation. Retail index investors consented to none of it.

Some may call it "dumb money." The more precise term might be "captive money". Nasdaq didn't sell SpaceX to the public. It sold the public to SpaceX.

"Elon negotiated a “fast entry” deal with Nasdaq so that SpaceX will be automatically included in the blue-chip index. That means billions of dollars of passive money will automatically flow into the company as soon as it lists."

It only means that if the mutual fund companies (Vanguard, Fidelity, Blackrock, etc.) that own every company in the NASDAQ decide to actually purchase shares in SpaceX. But mutual fund companies have agency! They can make choices! They could choose simply not to buy SpaceX.

How would they justify such a choice? Easily. Just say that you are only going to include companies in your NASDAQ index that would have been included in the index prior to the recent changes. Make clear that your company thinks the changes to the index are a bad idea and you're not going to waste your investors' money on bad companies.

I don't know what the exact rules are for the NASDAQ, but for the S&P they're pretty clear.

The rules include:

***Every company in the S&P 500 must report positive earnings in the most recent quarter and the sum of its earnings in the previous four quarters must be positive.***

That would exclude SpaceX.

So I feel like retail investors have a play here. If you own shares in a mutual fund indexed to the S&P or the Nasdaq, contact your mutual fund company and tell them that you are boycotting them if they buy the enshittified index.

“I will sell all my shares in your S&P 500 mutual fund (over time, perhaps, if such a sale will trigger tax consequences), and I will never buy another fund from your company again, if your S&P 500 index fund purchases any company that has never shown a full-year profit.”

The S&P can decide to include any company in the index, and individual investors probably don’t have much they can do about it … but if Vanguard, Fidelity, Schwab, and the rest hear from their investors, there will be blowback.