Day 25 of our war with Iran. The death count rises. 13 American soldiers have lost their lives. 18 are dead in Israel. 1,000 are dead in Lebanon. 1,500 are dead in Iran. According to the President we’re holding talks with Iran, but according to Iran, we’re not. Meanwhile, Trump still wants his $200 billion in defense funding because it’s “nice to have,” and Secretary Hegseth there’s “no time set” on when this war will end. Let’s be realistic: It’s here to stay.

The time for shock and outrage is over. Not because it’s unwarranted, but because it’s too late. The bombs have been dropped, the conflict is underway, and our President cannot be bargained with. It’s time we accept our new normal and start preparing for the future as there’s no going back.

Our future probably holds a few things: more violence, more polarization, and more instability among them. You could start scenario-planning for this future, or you could determine it’s so uncertain that scenario-planning is pointless. Both would be reasonable perspectives. But there’s one aspect of this war that you’d be foolish not to plan for. In fact, it’s a future I’d argue you must plan for. Not because it’s lethal, nuclear, or poisonous, but because it’s certain. That future is quite simple: Everything in your life is about to get way more expensive.

It Starts With Oil

As you probably know, the price of crude oil is going haywire. That is because 20% of the world’s supply is shipped through the Strait of Hormuz, which Iran all but entirely controls. These are the very basic facts you’d think our leadership had strongly considered before they decided to start dropping bombs on them. I guess not.

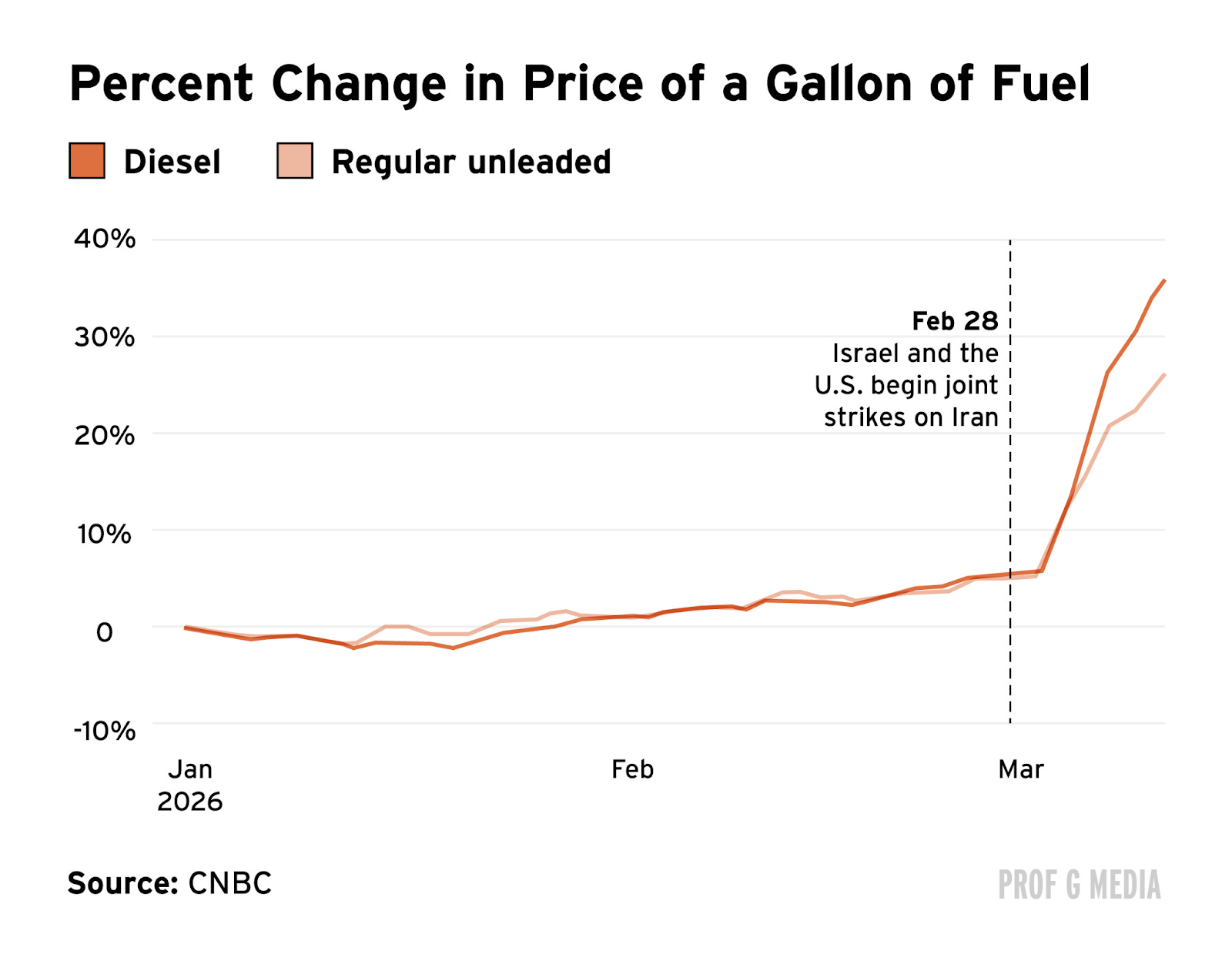

As you also probably know, the substance that fuels your car is a refined product derived from crude oil called gasoline. They’re not exactly the same thing, but they’re pretty close to the same thing. That’s why higher oil prices result in higher gasoline prices almost immediately, and why the price of gas in America has risen more than 30% since the war began.

I don’t know how much this is impacting your life specifically. But I do know how much it’s impacting Americans’ lives on average. For every dollar increase at the pump, the typical household has to spend an extra $530 per year. Americans are collectively spending $300 million more per day on gasoline today than they were before the war. For low-income families this is extremely painful, as they already spend roughly a fifth of their income on energy costs.

If you drive a truck, you’ve noticed diesel prices are soaring too — up 40%. Diesel isn’t the same as gasoline. It’s thicker, heavier, and more powerful, but it’s still a derivative of crude, which is why prices have also exploded. Regular car drivers may think these differences are irrelevant to them — they’re not. Let me explain.

Domino Effect

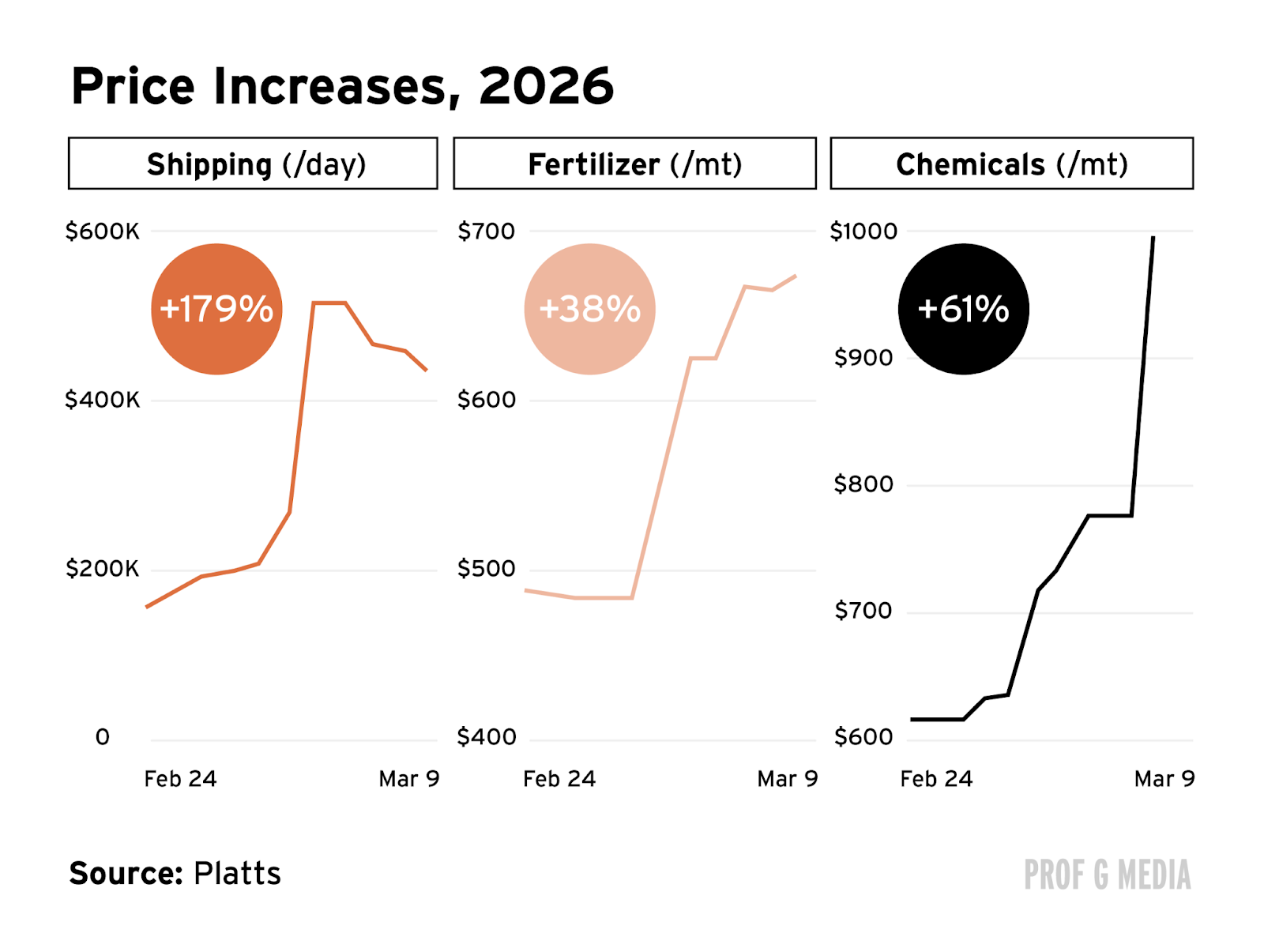

As the cost of diesel rises, the cost of trucking products around the country rises too. Diesel accounts for roughly a quarter of trucking companies’ per-mile operating costs, second only to driver wages. This is a big deal, as trucks move over 70% of goods by weight around the nation. But it’s not just trucks, it’s ships too. Fuel accounts for more than half the cost of shipping, which is why freight prices have risen roughly 30%. Baked into that number are insurance premiums too, which (for vessels traveling through the Gulf) have already risen by about 50%. War with Iran presents a unique blend of problems that make it a lot more difficult to deliver products to people.

Another domino that’s fallen is fertilizer. Gulf states account for roughly 30% of the world’s ammonia and half of the world’s urea, two substances critical for fertilizer production. U.S. urea and ammonia prices are up 21% and 41% respectively, which has resulted in a 25% surge in the price of fertilizer. This hasn’t affected you yet, but it will. Fertilizer costs account for about a third of the cost to grow crops. As with tariffs, every additional input cost will eventually be passed onto the consumer. This is especially concerning when you consider how bad food inflation had already gotten before we struck Iran.

I’m not done yet. Oil is also a primary input for plastic, PVC, and other industrial substances. It’s also critical for producing things like steel, aluminum, and cement. Lots of these materials also get shipped through the Strait of Hormuz. The result: Construction material prices have risen as much as 30%. These price increases will add more fuel to the dumpster-fire that is the U.S. housing crisis. You might remember when lumber prices tripled after Covid. What you might not recall is how those price increases pushed housing costs up by roughly $35,000. The median U.S. home now costs $405,000, about 9 times median income, the most expensive in American history. How much worse will these numbers get when the price of literally every input goes up?

No Place To Hide

When times get really tough, the best thing you can do is ask for help. In the case of inflation, that means trading with other nations. This was the U.K.’s revelation during the 19th century and Japan’s after World War II — like many economies throughout history, they realized trade was cheaper.

This time round, we don’t have that option. For one, we’ve already significantly damaged our relationships with trade partners via arbitrary tariffs and military threats. More importantly, however, prices have gone up even higher everywhere else. Across Asia, gas prices have increased as much as 60%. In Europe, the price of liquid natural gas (on which they’re heavily reliant) has risen over 70%. That’s because their supply chains are even more dependent on the Strait of Hormuz than ours. In other words, we can’t trade our way out of this mess. No one’s coming to save us.

Time To Get Worried

The Federal Reserve’s “dual mandate” is to 1) maximize employment, and 2) stabilize prices. As it stands, unemployment isn’t a huge problem — but it’s becoming one. We lost 92,000 jobs last month, and as Jerome Powell said last week, net job creation in the private sector in the past six months was “effectively zero.” Meanwhile, inflation is still a problem (we’re still way off the Fed’s target), and it’s about to become even more of a problem for the reasons we just discussed.

This puts the Fed in a tough spot. Do you keep cutting rates to spur employment but risk more inflation? Or do you stop cutting rates to bring down prices but risk losing more jobs and suppressing economic growth? At the start of the year, the expectation was that the Fed would choose the former. The inflation picture wasn’t ideal, but rates had been high for a while and the employment trend was starting to get concerning. This formed the basis of the 2026 bull-market thesis: Yes, the AI bubble was scary, and yes, tariffs were concerning, but ultimately stocks perform well when rates get cut.

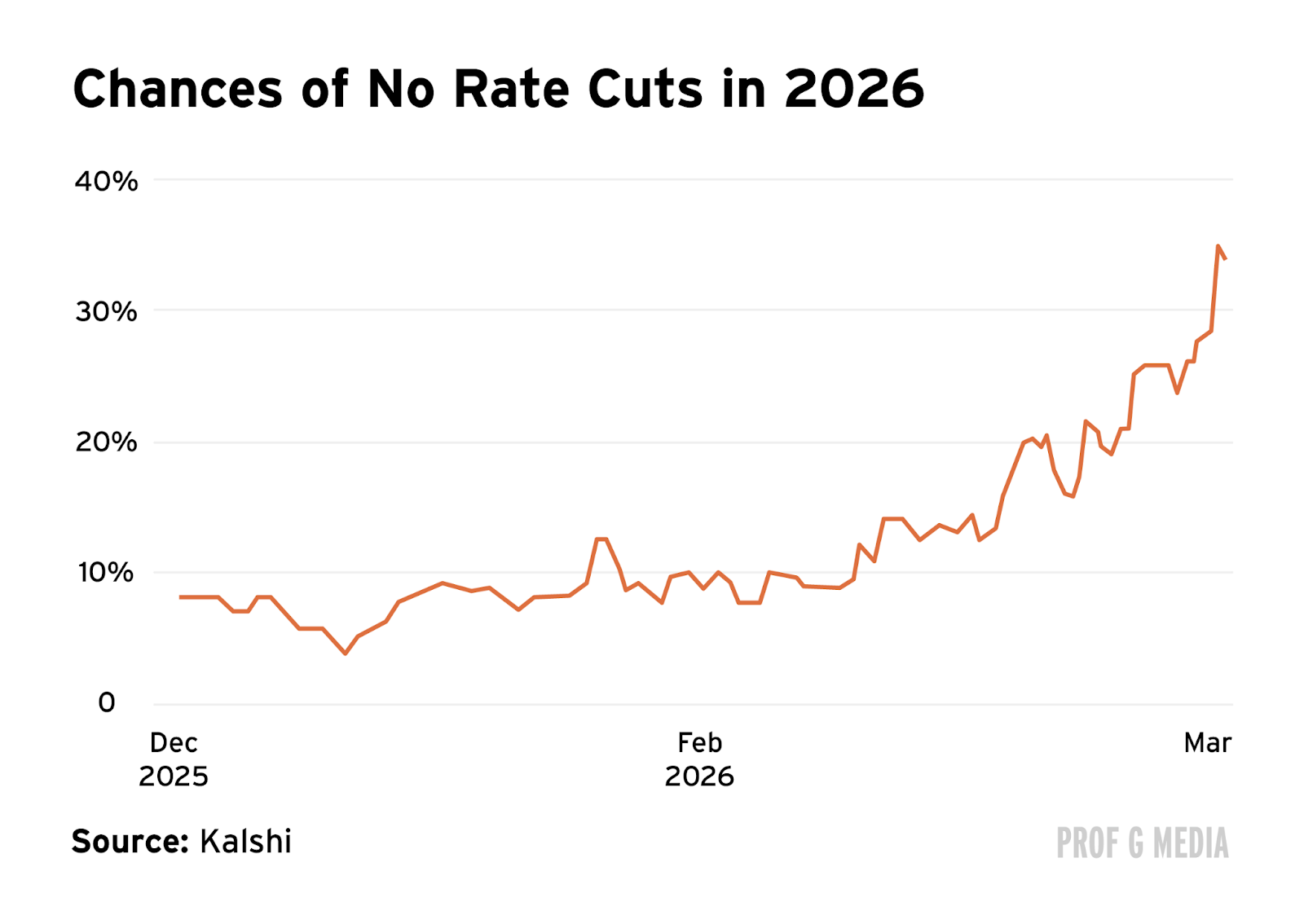

Now that we’ve bombed Iran, however, everything’s changed. Prices are surging again, which means the Fed’s other problem (inflation) is a lot bigger again. This should theoretically call the entire rate-cutting cycle into question, and in fact, according to prediction markets, it already has: In the 25 days since the war began, the probability that the Fed won’t cut rates at all has risen from 14% to 31%. Meanwhile, the chances of rate hikes this year are shooting up.

I’m transported back in time to 2022. It was my first year out of college, and I was just starting up with Scott. Covid had already taken senior year from me, and now, because of messed up supply chains, I had to pay $15 for a carton of eggs. The Fed had no choice — it had to raise rates. Fortunately for me the rate hikes worked, and inflation came way down. But not before it brought something else down with it: the U.S. stock market, which fell nearly 25% that year, its worst year since the financial crisis.

Not There Yet

I’m not saying it’s Covid again, but the dynamics are unmistakably similar. A violent force inserts itself into global supply chains, prices immediately rocket through the roof, governments tell us it’ll soon be over (but we all know it won’t), central bankers start to accept the gravity of the situation, they start to tighten policy and ratchet up rates (despite investor protests), market optimism starts to get sucked out of the room, stocks start to fall lower, and lower, and lower still, growth screeches to a halt and then inverts, until we’re forced to contend with what our situation has probably become: a recession.

To be clear, we’re not there yet. GDP growth is still positive (though a lot less positive than we initially thought), unemployment is still relatively low (though rising quickly), and inflation isn’t nearly as bad as it was after Covid. But let’s also acknowledge where we’re headed. Every day this war goes on, American households lose more purchasing power. Grocery bills, airline tickets, shipping costs, and credit card statements are rising by the billions. We’re literally getting poorer by the day.

As Trump looks to the polls, he will soon realize the gravity of his error. But this isn’t Liberation Day, this is war. Unlike tariffs, you can’t take murder back.

See you next week,

Ed

Appreciate your insight, Ed. It isn’t pleasant but reality is what it is. We’ve all been handed a shit sandwich by a bunch of grifters.

from the economic genius who bankrupted 3 casinos