Fourth-quarter earnings season kicks off this week, with all the major banks reporting.

The financial sector is coming off a strong year in 2025, buoyed by deregulation and robust capital markets activity. Big bank stocks rose roughly 30% last year — nearly double the S&P 500’s gain.

The Trump administration has made several moves to loosen banking regulations, including rolling back parts of Dodd-Frank, the post-2008 framework designed to limit risk-taking with depositors’ money. The result: It’s a very good time to be a big bank.

Why was 2025 such a strong year?

A couple of stars aligned here in a really nice way. Banks do as well as the economy they’re sitting in, and the American economy was pretty good last year.

Additionally, low-yield assets rolled off banks’ balance sheets. A loan made in 2020 that yields 3% got replaced with a new loan in 2025 yielding 7%. That trend will accelerate this year and create a natural lift for banks.

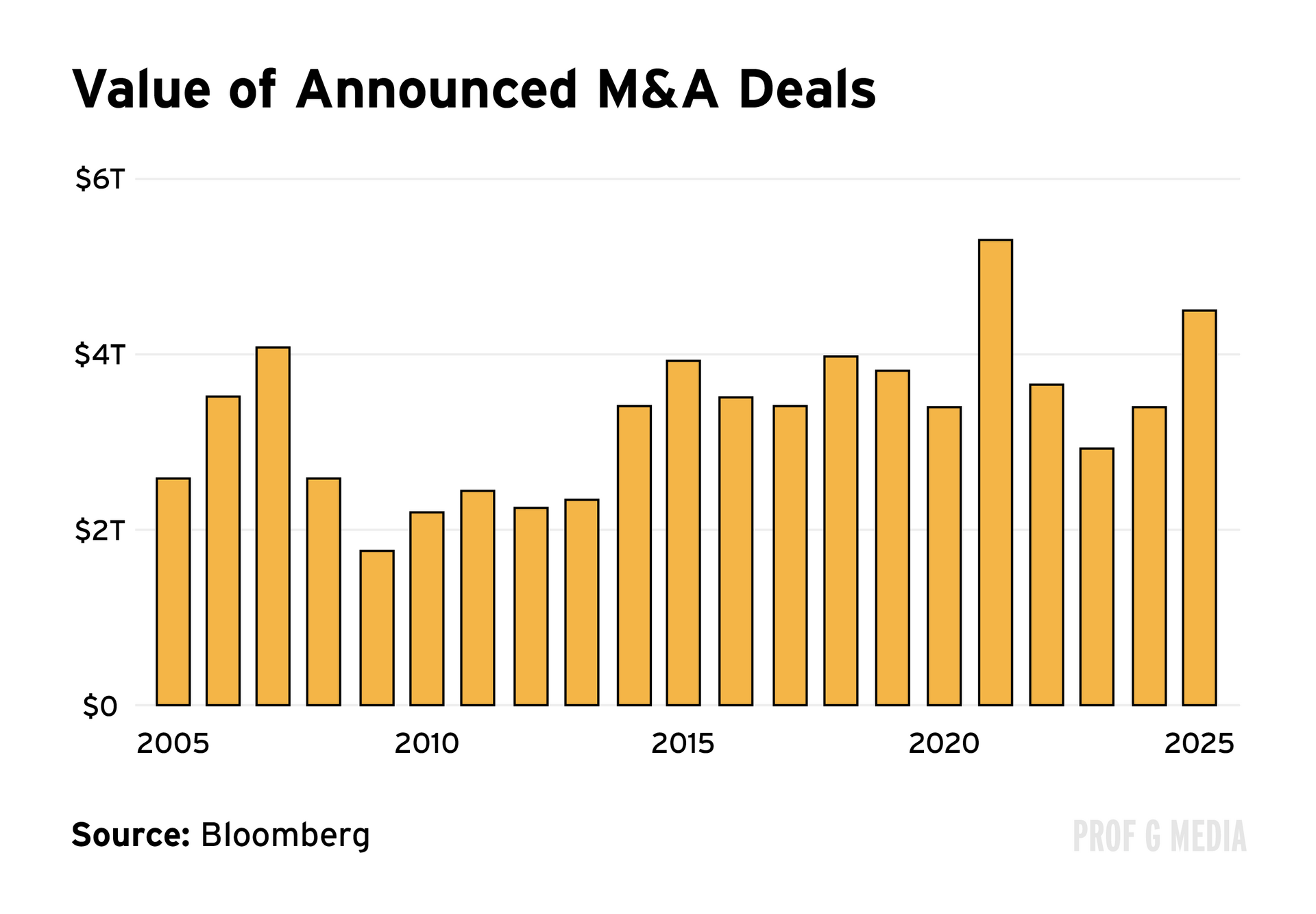

Finally, for the very big banks, active capital markets are a gold mine. Last year’s increased IPO and M&A activity was great for investment banking and trading desks.

What impact will AI have on bank stocks?

There’s been talk that AI will give banks tech-like multiples. I don’t buy it. Yes, they are businesses with high human capital costs, but banking is a human capital industry. If you replace half your bankers with AI, there will be consequences.

When good bankers and traders leave, they often take their clients with them. As people used to say about Goldman Sachs, our assets go up and down in the elevators every day.

What would be the impact of consolidation in the banking industry?

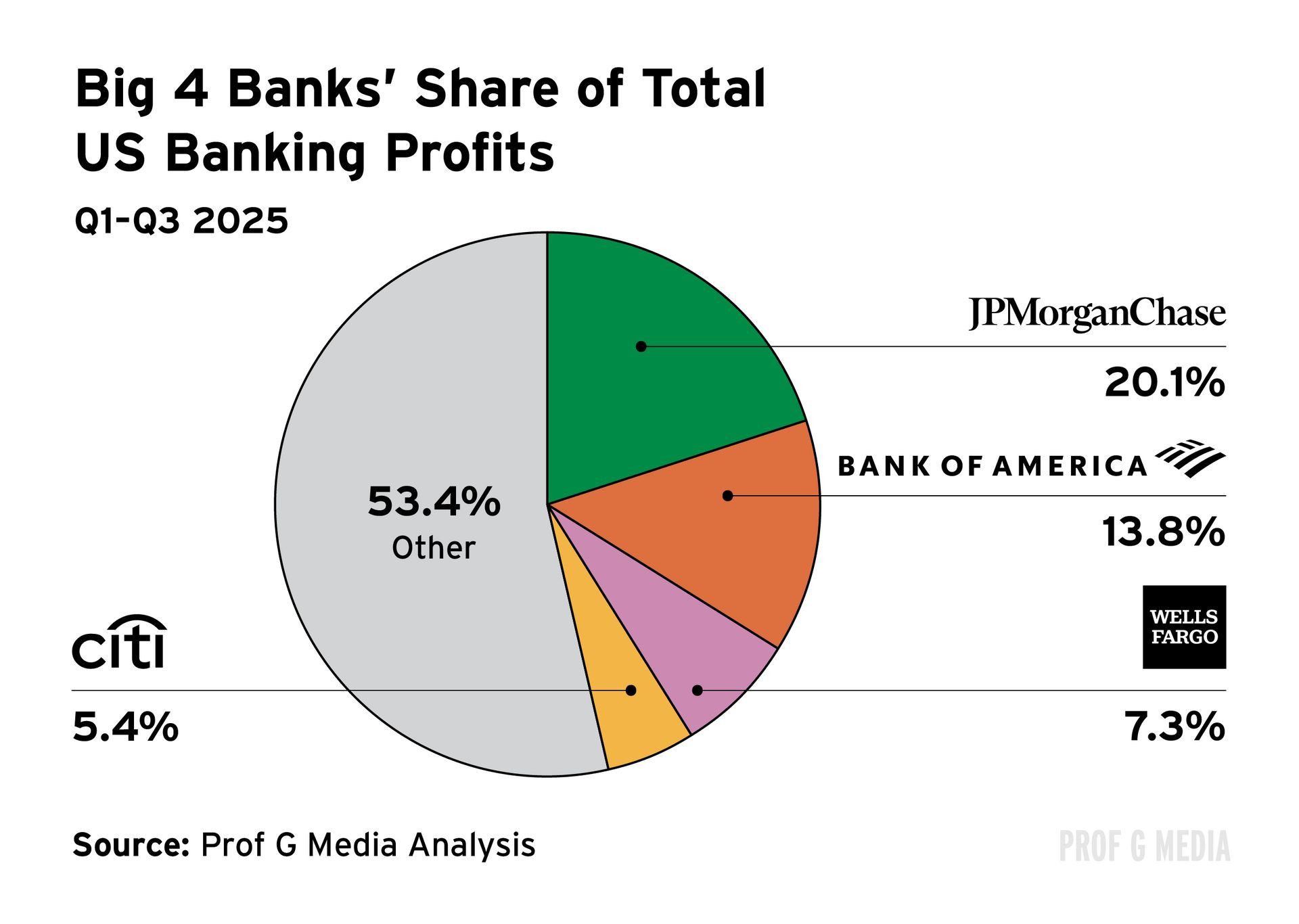

I think consolidation would be pro-competitive. JP Morgan, Bank of America, Wells Fargo, Citigroup, and U.S. Bank squeeze out most of the profits in banking. The other roughly 2,100 banks in America are squeezing out tiny drops of profit doing local banking. From an investor standpoint, regional banking has been a terrible place to invest. Consolidation would help.

But integrating bank mergers is a nightmare, and it comes down to misaligned incentives.

If you’re the CEO of a regional bank, you have every reason not to sell. You’re the (wo)man of your town, head of the Rotary … why would you want to give that up? If you sell your bank, you have to look at all the people who work for you and say we just got bought out at a premium valuation and a third of you are going to get fired. Goodbye.

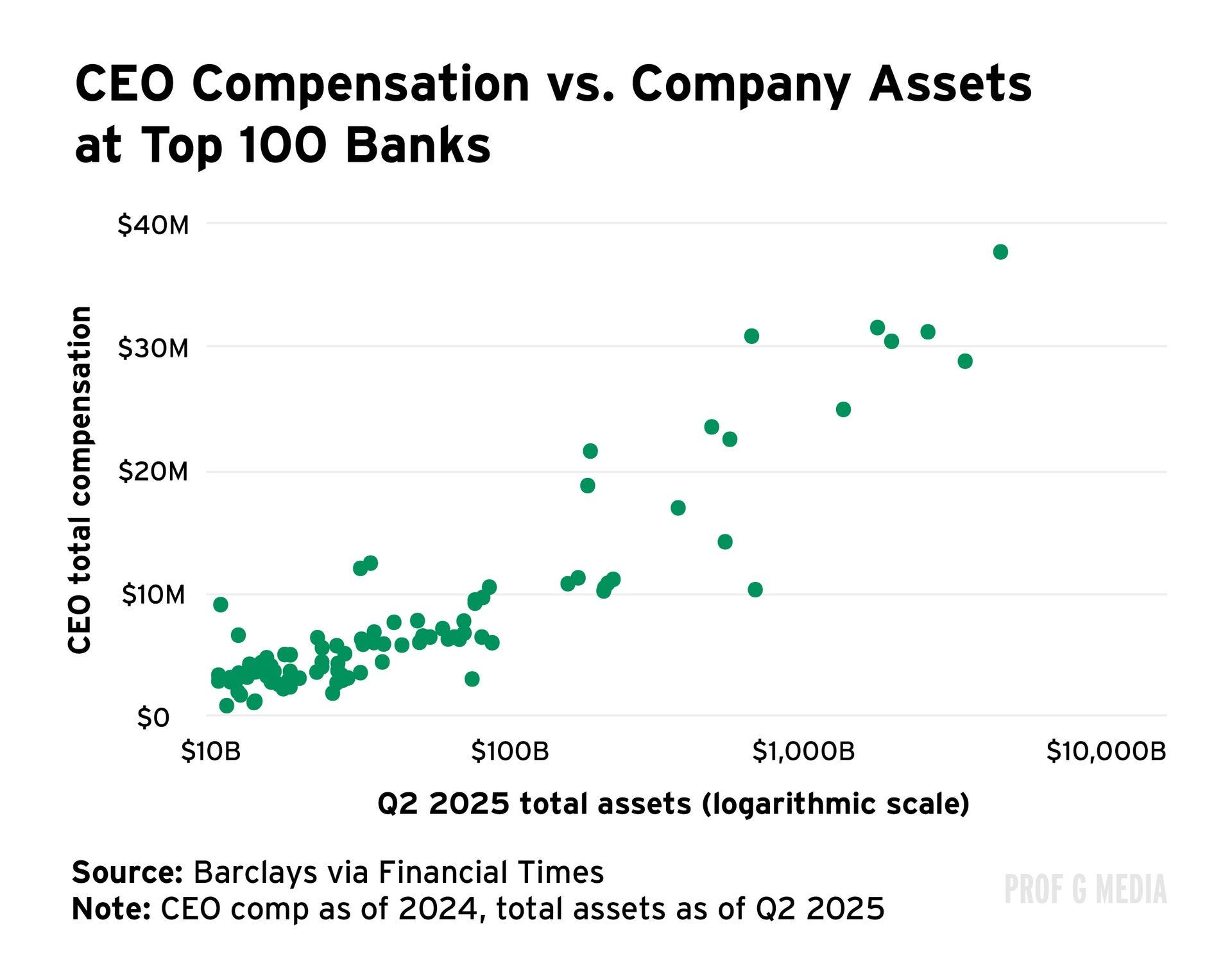

If you’re the buying bank, you have a strong incentive to overpay. There’s an incredibly strong correlation between bank size in terms of assets and CEO pay. If you run a bigger bank, you just get paid more money — whether it’s good or bad for the shareholders. So there’s a conflict of interest between the CEO and the investors in bank mergers.