On Saturday, January 3, U.S. troops entered Venezuela and, in less than three hours, extracted the country’s president, Nicolás Maduro, and his wife, Cilia Flores. Both were transported to New York City where Mr. Maduro will face drug-trafficking charges.

The operation leaves Venezuela and its $18 trillion in proven oil reserves ostensibly in the hands of its vice president, Delcy Rodríguez — but functionally subject to Trump’s vision for the country.

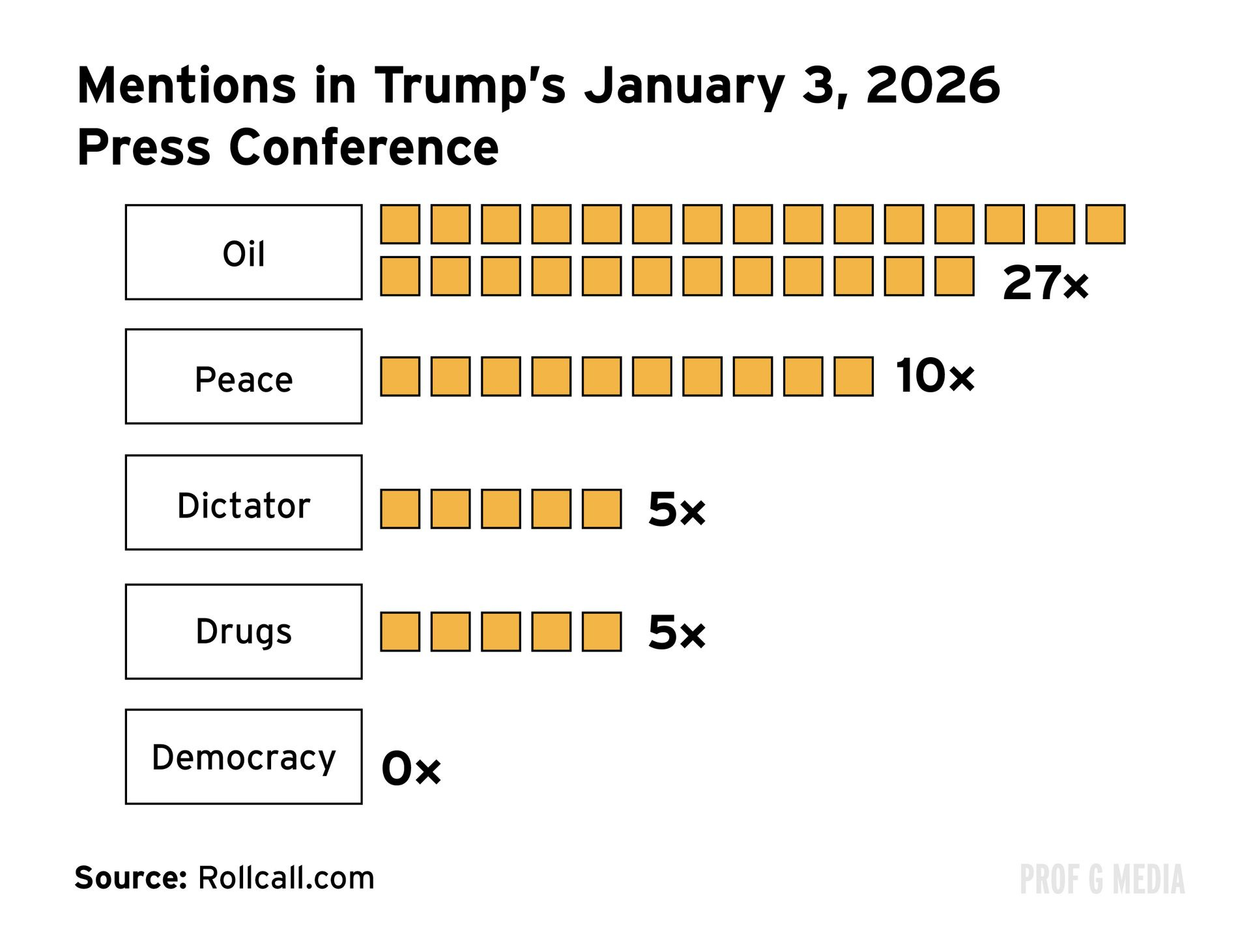

In a press conference on Saturday, Trump said the U.S. would run Venezuela until a “judicious transition” takes place, without alluding to a specific timeline.

Trump had more detailed plans for Venezuela’s vast oil reserves — believed to be the largest in the world. Namely, U.S. energy corporations will return to the country and fix its broken oil infrastructure. Trump also alluded to a kickback for the U.S. government, stating, “A lot of money is coming outta the ground. We’re gonna get reimbursed for all of that.”

Venezuela has nearly 18% of total global oil reserves, but years of mismanagement has caused the South American nation’s output to drop to only 1% of global oil production.

U.S. oil giants have not publicly agreed to Trump’s plan. Bringing Venezuela’s oil output back to where it was 15 years ago would cost an estimated $110 billion — twice the combined investment of major U.S. oil companies worldwide in 2024.

U.S. energy companies operated in Venezuela once — but it didn’t end well. In 2007, the Venezuelan government seized their operations in a move that Trump has since called “the largest theft of property in the history of our country.”

ExxonMobil and ConocoPhillips refused to accept the terms of the takeover, and the Venezuelan government still owes them billions.

Chevron is the only major U.S. oil company still operating in the country.

According to Politico, the Trump administration has told oil executives that if they want full reimbursement, they must comply with his order to revitalize Venezuela’s petroleum industry.

Given this context, how will U.S. intervention impact the economy and financial markets?

The Oil Market

In the short term, this move will likely have a muted impact on oil prices. Conflict in Venezuela was already priced in, and the country is currently such a small producer of oil, that near-term disruptions won’t have a significant impact on the broader market.

The oil market is oversupplied as it is. Increased output from OPEC+, Brazil, and the U.S. pushed oil prices down last year for their biggest annual decline in half a decade.

U.S. crude oil fell nearly 20% last year.

The Economy

Once Venezuelan production ramps up, it could contribute to the glut in supply and push oil prices down even further.

While this would be an unhappy outcome for big oil companies, it would please President Trump. On the 2024 campaign trail, he promised that, if elected, gasoline prices would fall below $2 per gallon.

Lower gas prices could help bring down inflation. Oil is an essential input to most goods —- in transportation, feedstock, manufacturing, etc. — so lower prices drive down production costs across the economy. Research from the St. Louis Fed shows that higher oil prices are associated with higher producer prices and vice versa.

Specific Beneficiaries

In the near term, the most likely winners are companies that refine Venezuelan oil in the U.S. Gulf Coast. Major refiners include Valero, Marathon Petroleum, Citgo, Chevron, and Phillips 66.

In the longer term, oil field services companies like SLB, Baker Hughes, and Weatherford will likely benefit from the reconstruction of Venezuela’s languishing oil operations. These firms produce, maintain, and repair oil extraction equipment.

Of course, the most immediately impacted are the people of Venezuela, 90% of whom live in poverty. Sentiment is divided: According to The Wall St Journal, 64% of Venezuelans abroad support U.S. military intervention to depose Maduro, compared with 34% within Venezuela.

Here’s hoping that this weekend’s military intervention has some positive humanitarian side effects.