Why Are Markets Hitting Record Highs?

Three reasons stocks keep ripping through a war

100

Sally Ride, the first American woman in space, was asked by NASA engineers if 100 tampons would be enough for her week-long voyage.

If the news is bad, why are stocks at all-time highs?

AI’s newest obstacle is … humanity

The real reason Amazon is buying Globalstar, plus a check-in on Prof G Media’s stock pick of 2026

Why Markets Are Ignoring the Iran Crisis

Last week, peace talks with Iran collapsed, the U.S. blockaded the Strait of Hormuz, and the International Monetary Fund warned that further disruptions in oil markets could raise the risk of a global recession.

Still, the S&P 500 and Nasdaq both hit fresh all-time highs. With so much uncertainty, why are markets so bullish?

There are a couple potential explanations. First, historically, wars aren’t that bad for U.S. markets. The U.S. is isolated geographically and insulated by having the largest and most liquid financial markets in the world. During times of uncertainty, the American equity and credit markets are seen as safe havens.

The average U.S. stock market decline during 30 major geopolitical events since 1939 was just 4%, and stocks typically bounced back within six weeks.

One year later, outcomes improved even more: the S&P 500 posted double-digit gains in the 12 months following Pearl Harbor, the Cuban missile crisis, the John F. Kennedy assassination, and the start of the Israel-Hamas war.

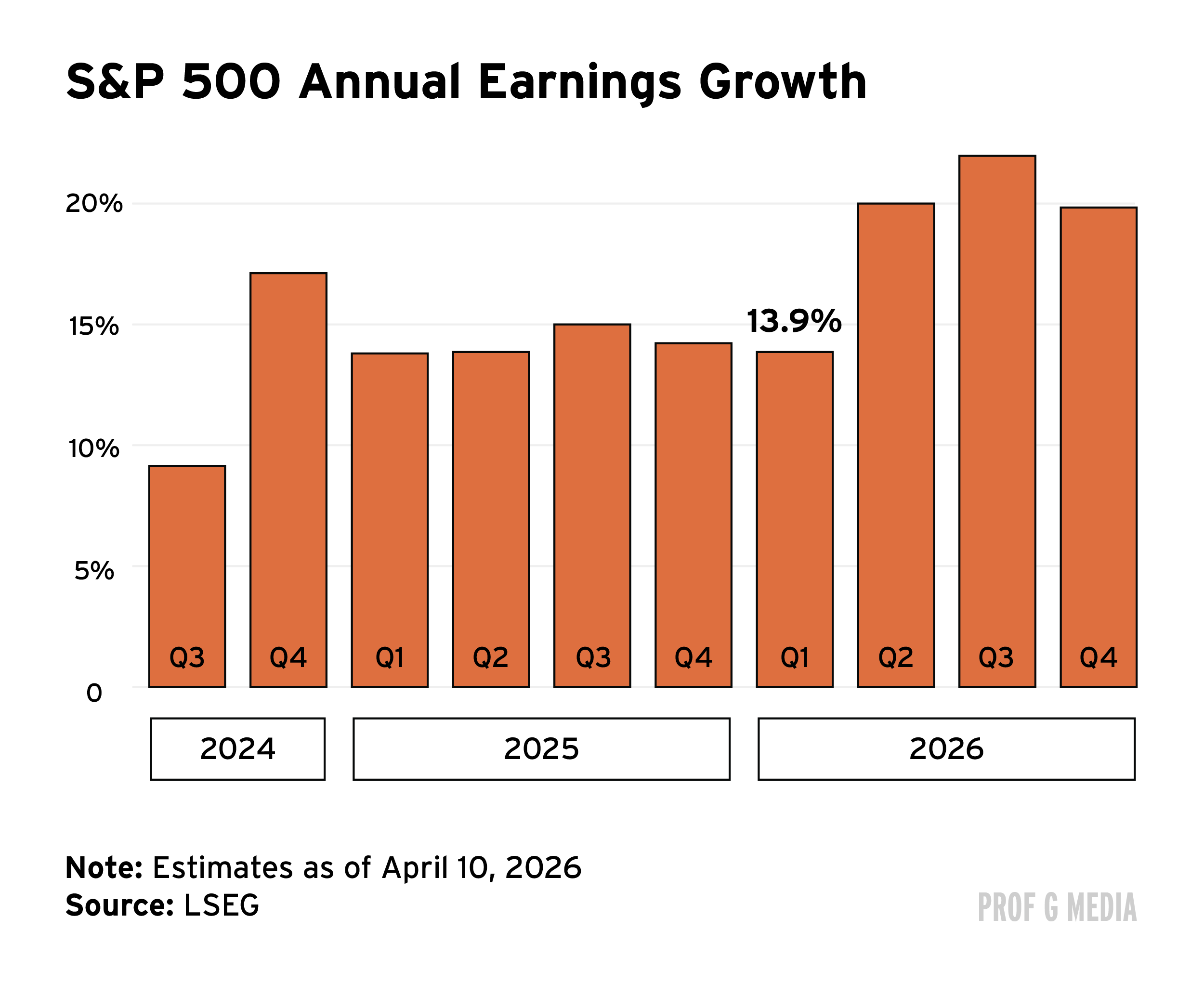

Second, company earnings are strong. The S&P 500 just posted its fifth consecutive quarter of double-digit earnings growth — the last time that happened was in 2018.

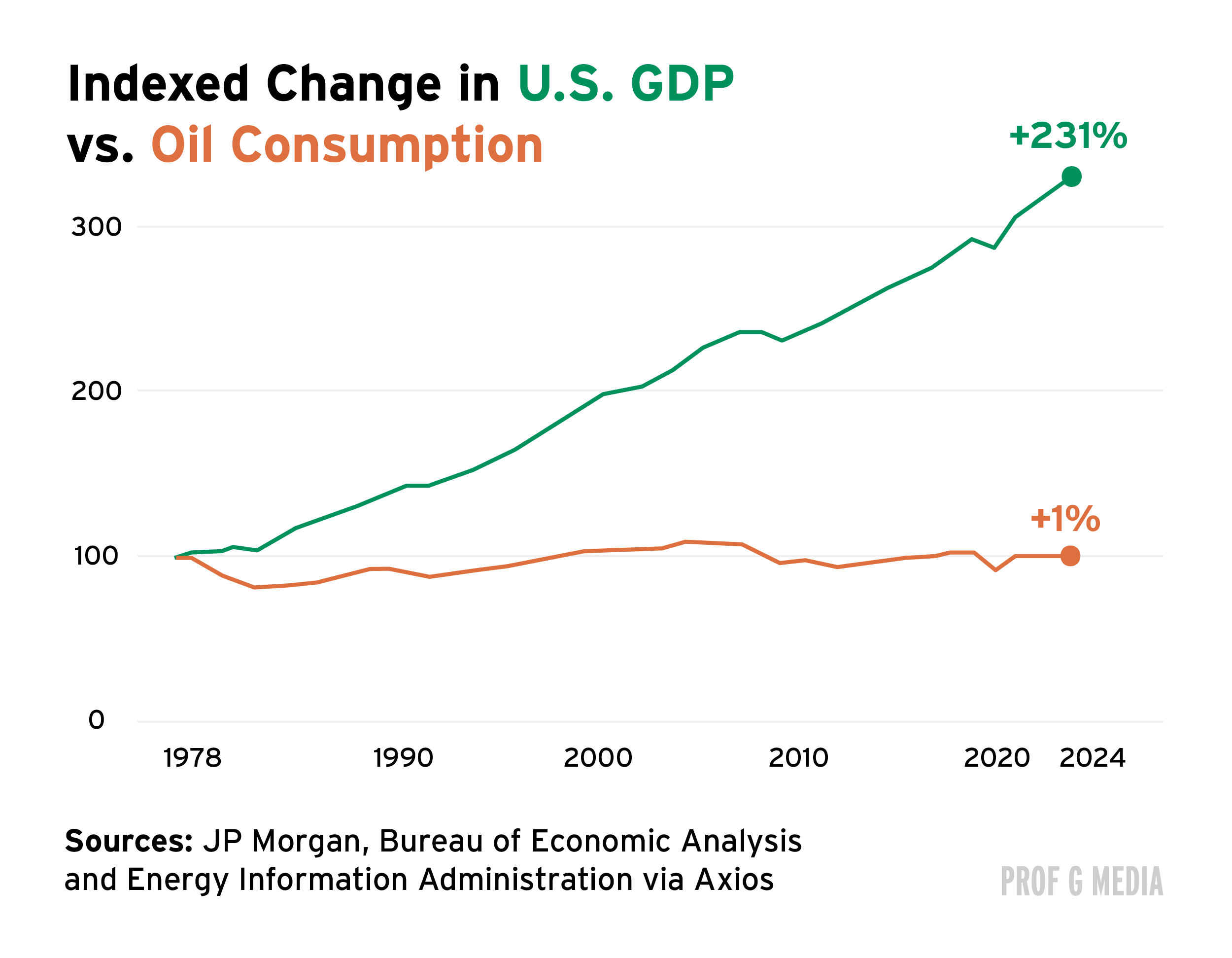

Third, rising gas prices may be affecting big companies and consumer spending less than expected. In the 1970s, spikes in oil prices triggered a recession. But since then, the U.S. economy has grown less dependent on oil: GDP has tripled, while oil consumption has stayed about the same.

Furthermore, consumer spending now hinges more on the wealthy than the middle class, and high-income consumers are less affected by energy costs.

The top 10% of earners account for half of consumer spending, or a third of GDP, and the highest-income quintile spends only 2% of their budget on gasoline. That’s compared with low income households that spend nearly 20% of their budgets on gas.

I’ve been calling this the ketamine economy. Ketamine is dissociative. You leave your body and watch your life from the outside. That’s exactly what the Dow and the Nasdaq do. They give the illusion that society is doing well, but they’re not a measure of prosperity. They’re a proxy for earnings and the wealth of the top 10%.

Think about what’s actually driving this market. Fifty percent of consumer spending comes from the top 10%. Do they care that gas is $6 a gallon? It doesn’t register. Tech dominates the market indexes. What does chaos in the Strait of Hormuz do to Nvidia’s margins? Nothing.

In addition, there’s this phenomenon of buying the dip. If you look at the last four major exogenous events, the Gulf War, 9/11, the Iraq War, and COVID, basically, there was a dip and then the markets ripped back the following year.

We did have a drawdown here in March, but it’s rebounded since. I think what’s happening is the cycle time between fear and uncertainty around a war and the opportunity to buy is compressing. Now people are like, let’s move to the part of the program where we make money.

Let me break down what’s actually happened in the markets. Year to date, the biggest winners were industrials, materials, and energy. That made sense — war in the Middle East, oil prices surge, and energy stocks move higher.

On March 30, we hit the market bottom. Since then, it’s completely reversed. Energy is down 11%. Meanwhile, financials are up 8%, communication services up 10%, tech up 21%.

So what happened? For weeks, investors were doing what you’d expect. They were pricing in the risk of the Iran war. Then something switched. I call it timeline fatigue. The Iran story kept producing plot points with no resolution. Ceasefire, then no ceasefire. Blockade, then no blockade. Trump says negotiations are going somewhere, then they don’t. At a certain point, investors just gave up trying to interpret the headlines.

When investors stopped looking at the geopolitics, they looked at the fundamentals. Earnings are strong, guidance is strong. Microsoft and Nvidia are trading at some of their lowest forward multiples in years. Suddenly the math was simple: Big Tech is executing, multiples are attractive, let’s buy.

The AI Industry Faces a New Threat: An Angry Public

The AI backlash is turning violent. On April 10, a man threw an incendiary device at OpenAI CEO Sam Altman’s house, and then went to OpenAI headquarters and threatened to burn it down. A few days earlier, a gunman fired 13 rounds into the front door of an Indianapolis councilman’s home. The perpetrator left a note that read “No Data Centers.”

Americans are making it increasingly clear they don’t like where AI is headed.

Data centers, the most physical manifestations of AI, are an obvious target. Last year, 48 data center projects, representing at least $156 billion in investment, were blocked or stalled by local opposition, predominantly in the form of peaceful protests.

Anti-AI sentiment is starting to shape policy: Maine just introduced a bill to ban data centers altogether, joining 11 other states with active bills proposing restrictions or outright bans.

Opposing data centers is one of the few topics popular on both sides of the aisle. Of the elected officials who’ve taken positions against AI data centers, 55% are Republicans and 45% are Democrats.

Another, perhaps surprising cohort coming out against AI is Gen Z. A recent survey found that 44% of Gen Z admitted to having sabotaged their company’s AI rollout in some way.

This isn’t really about AI — it’s about inequality, and AI has become the most visible symbol of it.

The top 19 households in America own 2% of all wealth, up from 0.1% just 40 years ago. We have more private security guards in this country than high school teachers. Now you have this technology that promises to reshape the entire economy, and the people positioned to benefit are the same people who already own everything. Meanwhile, local communities are watching their electricity bills go up to power data centers they had no say in building.

That’s the context for the violence. And when you look at the reaction online, it mirrors the Luigi Mangione response. People sending support, asking about bail funds. That’s not fringe behavior. That’s a signal about where a meaningful portion of the country actually is.

There’s no justifying the violence. Full stop. And I’d push back a little on the idea that this is specifically an AI problem. Historically, public figures have been targets of violence. One in three presidents has been shot at. The difference is, CEOs are now famous. Nobody knew who CEOs were when I was growing up. Now they’re the figureheads of the American economy, and that makes them targets. Oh, and there’s access to assault weapons and guns at every f*cking corner.

But separate from the violence, there’s a real story here about brand collapse. Sam Altman used to be the tech CEO we actually wanted. He spoke in hushed tones to Congress about the dangers of the thing he was building. He didn’t own equity in OpenAI. He was going to save us from AI while building it responsibly.

Then the mask slipped. He started sh*tposting Microsoft. He compared data center energy use to the calories it takes to raise a child, essentially telling critics to stop complaining. Then Marc Andreessen started saying he doesn’t believe in reflection, only forward momentum. These are not people who are winning hearts and minds.

The result is that AI’s brand has collapsed, and it’s self-inflicted.

sponsored content

Your identity sells for less than $1

In the data broker market, personal profiles are cheap.

For a few dollars—or sometimes cents—buyers can access detailed records about real people.

Addresses. Phone numbers. Relatives. Property history.

That information fuels scams, spam, and identity fraud.

Incogni helps shut down that pipeline by removing your personal information from hundreds of broker databases automatically. Get 55% off Incogni using code PROFG

Stop your data from being sold

sponsored content

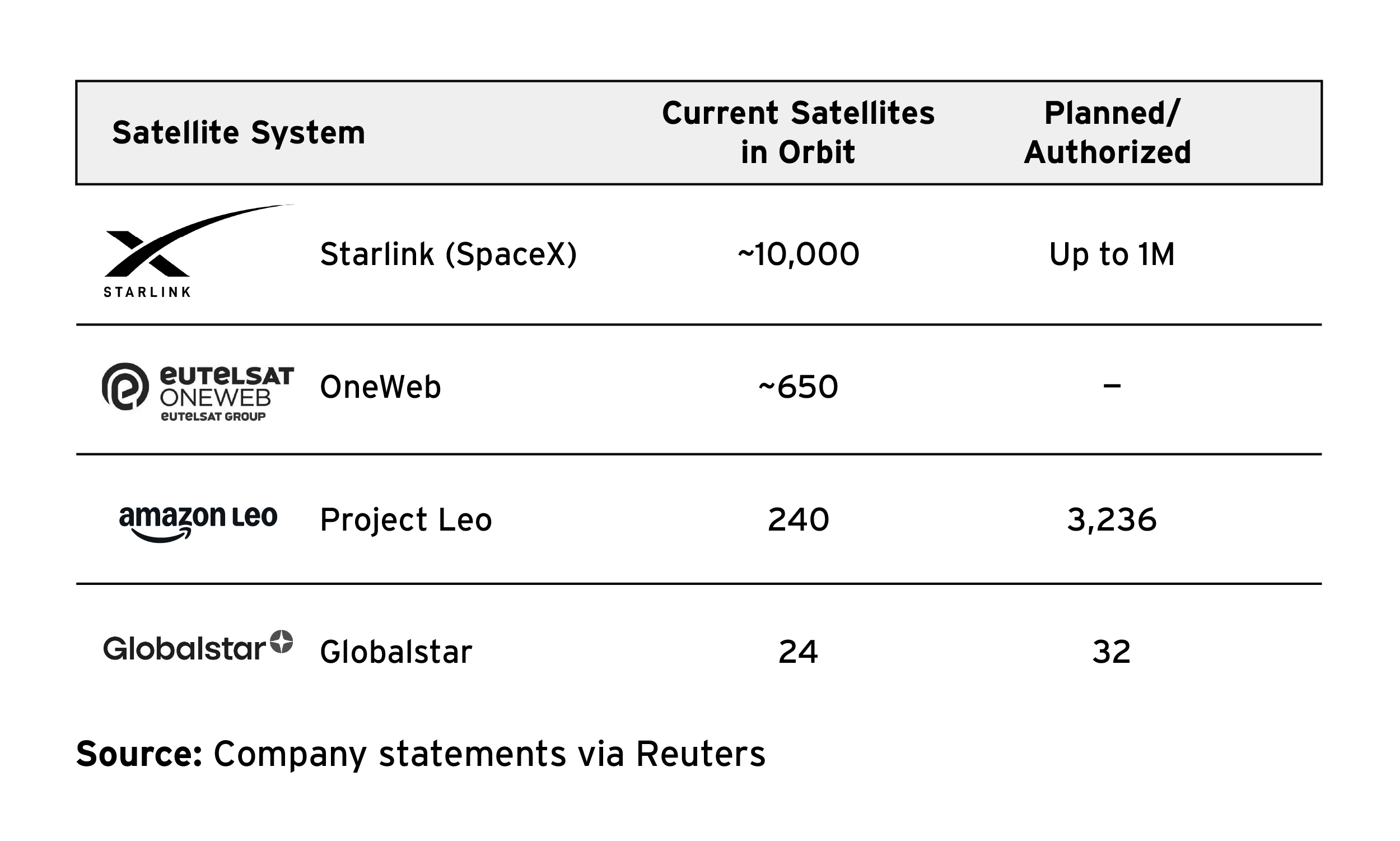

Amazon Buys Globalstar in $11.6 Billion Satellite Deal

Last week, Amazon announced it will acquire satellite communications firm Globalstar for $11.57 billion. Globalstar’s infrastructure will help accelerate Amazon’s plans to develop its own satellite network, deemed Amazon Leo.

On news of the deal, Amazon’s shares increased almost 4%, adding almost $100 billion in market capitalization — essentially paying for the acquisition eight times over. Globalstar shares rose almost 10%.

Still, the deal will be Amazon’s second-largest acquisition after Whole Foods, and it wasn’t cheap, especially given the size of Globalstar’s business. Globalstar operates just 24 satellites and has never been profitable.

So, why is Amazon paying so much for an unprofitable satellite company?

Amazon isn’t buying Globalstar for its 24 satellites, but rather the spectrum that Globalstar owns.

Spectrum refers to the invisible radio frequencies that wireless signals travel on. Some spectra carry Wi-Fi signals, some carry broadcast TV signals, some carry our smartphone data.

There is a finite amount of spectra, and the government, specifically the Federal Communications Commission, auctions off licenses for them every few years. But since there’s a fixed amount, they are expensive and hard to get. The last auction was in 2022, and Verizon paid more than $50 billion for its licenses.

Amazon wants Globalstar’s spectrum so that it can create its own private wireless network. In his annual letter to shareholders, Amazon CEO Andy Jassy described the company’s plans to use Amazon Leo to sell Wi-Fi to rural customers, airlines (Amazon already has a contract with Delta), and to integrate it into AWS.

But there’s another, even more important angle. Amazon’s industrial robots and expanding fleet of drones need to communicate constantly, and they will be able to operate more efficiently on a private wireless network. Essentially, Amazon’s purchase of Globalstar is an extension of their investment in their logistics infrastructure.

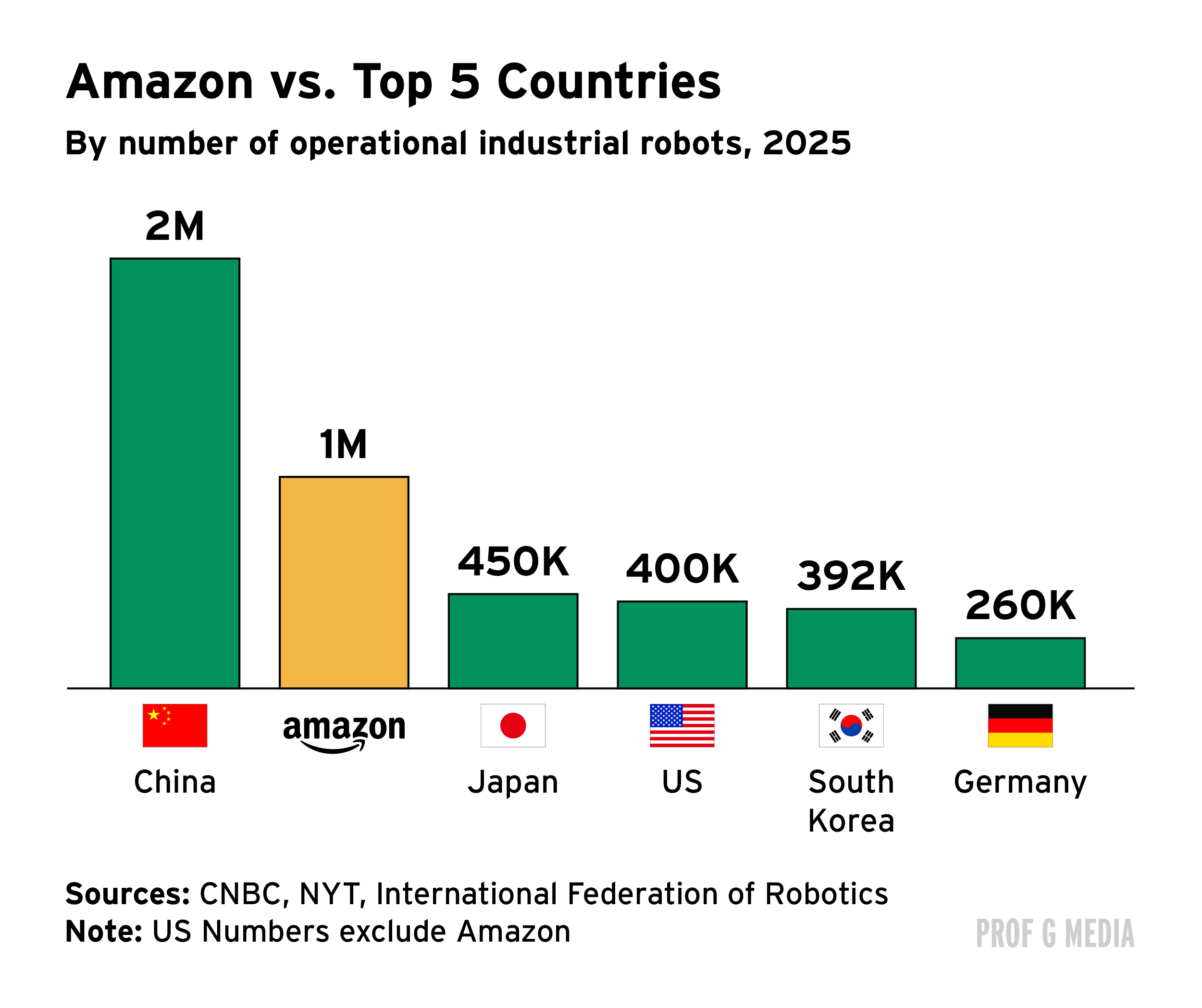

Prof G Media’s Big Tech stock pick of the year was Amazon. Why? Over the past few years, excitement about AI has made it easy to overlook the importance of hard assets. But this year, the rise of the HALO trade (heavy assets, low obsolescence) has made Amazon the best-performing member of the Magnificent 7.

Amazon’s hard assets are its biggest moat. It has as many airplanes as the Austrian or Norwegian military (110 aircraft), and more industrial robots in operation than all other companies in the U.S. combined.

These investments in automation are expected to boost productivity by roughly 25% at fulfillment centers.

The Allbirds pivot to AI is gonna inspire a bunch of copycats. Think: Kmart AI.

Prof G Markets is going on tour! Join us in San Francisco, Los Angeles, Miami, Chicago, and New York City. Expect special guests, unfiltered conversation, and the jokes that don’t make it on-air… Get your tickets here.

Totally agree with your framing: at this point, ATHs are increasingly a scoreboard for the top of the income/wealth distribution, not a “national wellbeing index.” When the top ~10% are responsible for roughly half of consumption, the marginal buyer that sets demand — and the marginal shareholder that sets risk appetite — is simply not the median household. That’s why markets can look “fine” even when large parts of society feel squeezed: the parts that drive aggregate spending and corporate revenue are still spending, and the parts that own the bulk of equities are still bidding up discounted cash flows. In that world, “strong markets” can coexist with social stress for a long time — not because the economy is secretly healthy for everyone, but because asset prices are increasingly a thermometer for top-decile balance sheets + profit share, while the median mostly experiences the economy through rents, healthcare, insurance, and debt service.

The "ripping through a war" framing assumes the S&P is a macro scoreboard. It isn't — it's a weighted bet on the future cash flows of the top 50 or so companies, most of which have near-zero Middle East exposure. Apple's iPhone margin and Microsoft's Azure contracts don't flinch at the news cycle. Record highs aren't a sign the economy is fine; they're a sign the top of the cap table has decoupled from the median household's reality.