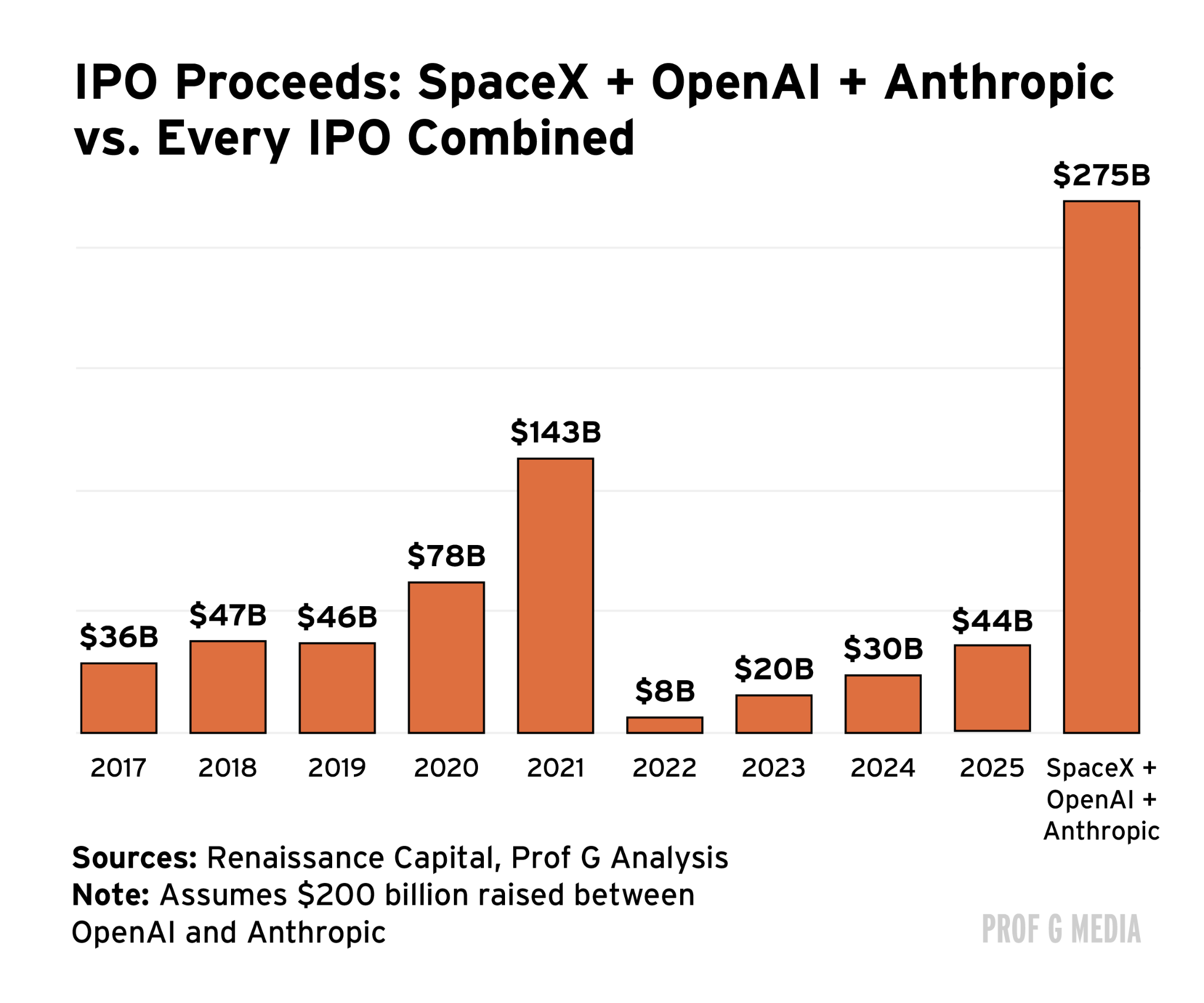

After years of hibernation, the IPO market is waking up. SpaceX will kick things off Friday with a $75 billion offering, the largest IPO in history and nearly triple the previous record. My personal thoughts on the IPO: trainwreck — but that’s another post.

Next, Anthropic will go public. Days after completing its $65 billion “Series H” round (H is the eighth letter in the alphabet and $65 billion is more than double the size of the largest IPO ever), the AI juggernaut submitted its S-1 filing. God knows how large this IPO will be, but with a 10% float we can comfortably assume the company will raise around $100 billion.

After that comes OpenAI. The ChatGPT-maker just filed for IPO, and given the size of its most recent fundraise ($122 billion — more than triple the largest IPO ever), we can assume this one will be likewise gigantic. How gigantic? Unclear. But for the sake of consistency let’s call it $100 billion too.

Tally up those three IPOs and that’s $275 billion in new equity supply. That would make 2026 the largest IPO year ever — roughly double the previous record set in 2021. That doesn’t include the nearly 70 companies that have already gone public this year, nor all the other companies that are about to.

But Wait There’s More

Last week, Google announced it would raise $85 billion in a secondary offering, the largest equity financing event in history. Two days later, we learned Meta was considering the same thing. Supposedly Microsoft and Amazon are as well. Assuming they’re all the size of Google’s, add another three hundred billion dollars or so to the equity supply.

Then there are all the shares from previous IPOs whose lock-up periods are about to expire. These are newly-issued shares that weren’t allowed to be sold until this year. (In other words, they’re now “in play.”) According to Goldman Sachs, the combined value of those unlocked shares will be nearly $500 billion — an order of magnitude higher than last year.

So: Between three record-breaking IPOs, four potentially record-breaking secondary offerings, and a record-breaking year for expiring lock-ups, the stock market is about to get hit with roughly a trillion dollars in new equity supply. That’s more than the entire stock market of Italy. Economists have a term for this kind of supply-side shock: Not good.

Economics 101

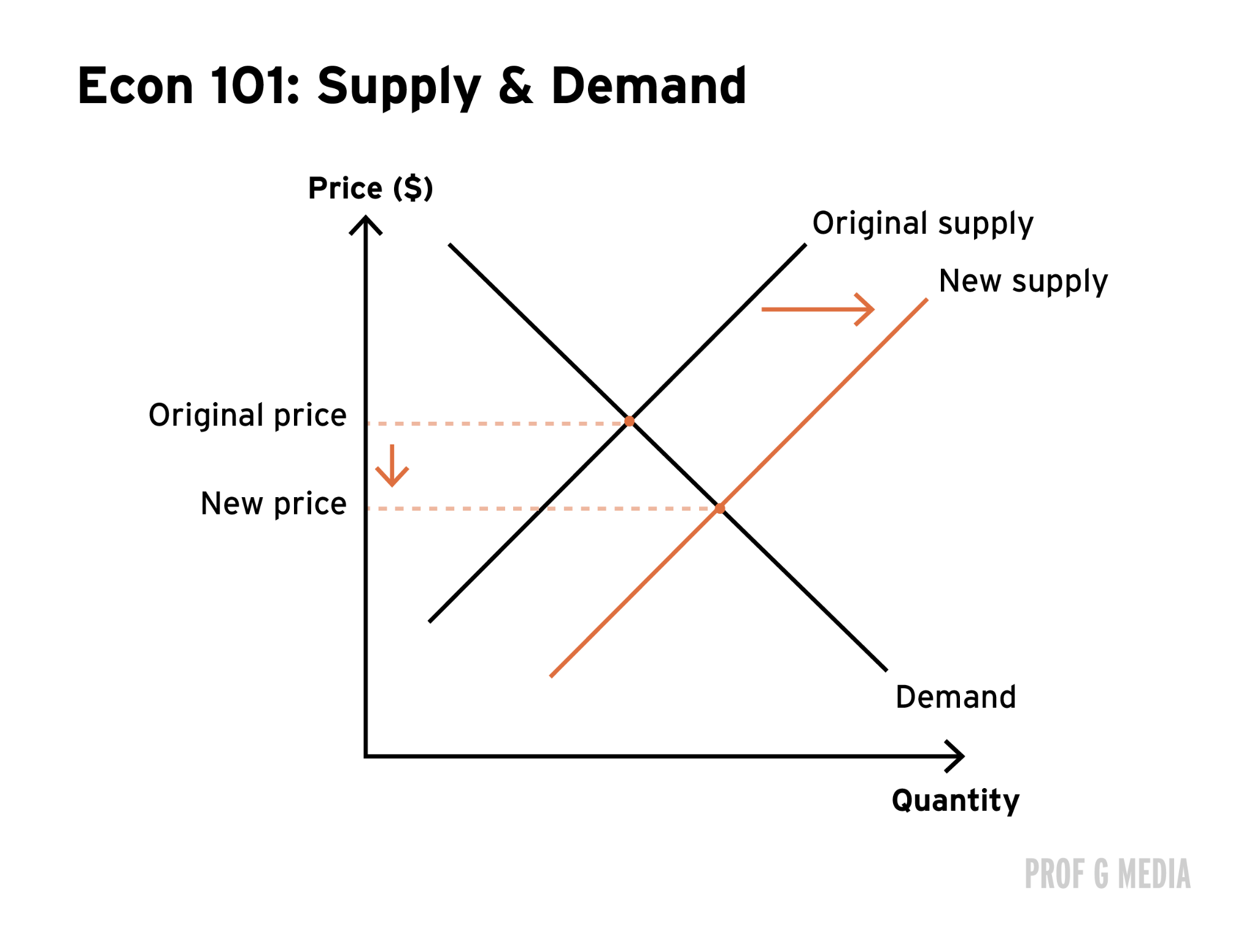

Let me take you back to my Freshman year at Princeton. As I walked nervously into McCosh Hall (where Einstein taught) for my first day of Econ 101, I saw a giant chart displayed on the projector screen. Emblazoned across the top of it read the words “SUPPLY AND DEMAND.”

“Everything in economics,” my professor proclaimed, “comes back to this chart.” Despite some initial confusion, I soon learned it described a very simple concept: All else equal, higher supply means lower prices. The reverse is also true: lower supply means higher prices. This is the most fundamental principle of economics. It explains everything from why US housing has gotten so expensive (not enough supply) to why Chinese-made consumer products have gotten so cheap (too much supply).

Supply & Demand: Stock Market Edition

A stock’s price is determined by many forces — hype, narrative, and fundamentals, etc. — but one of the less discussed forces is that of supply and demand. As the supply of a stock goes up, the price goes down, and vice versa. This is why companies love share buybacks, for example. By reducing the supply of available stock, they reward their shareholders with a higher stock price.

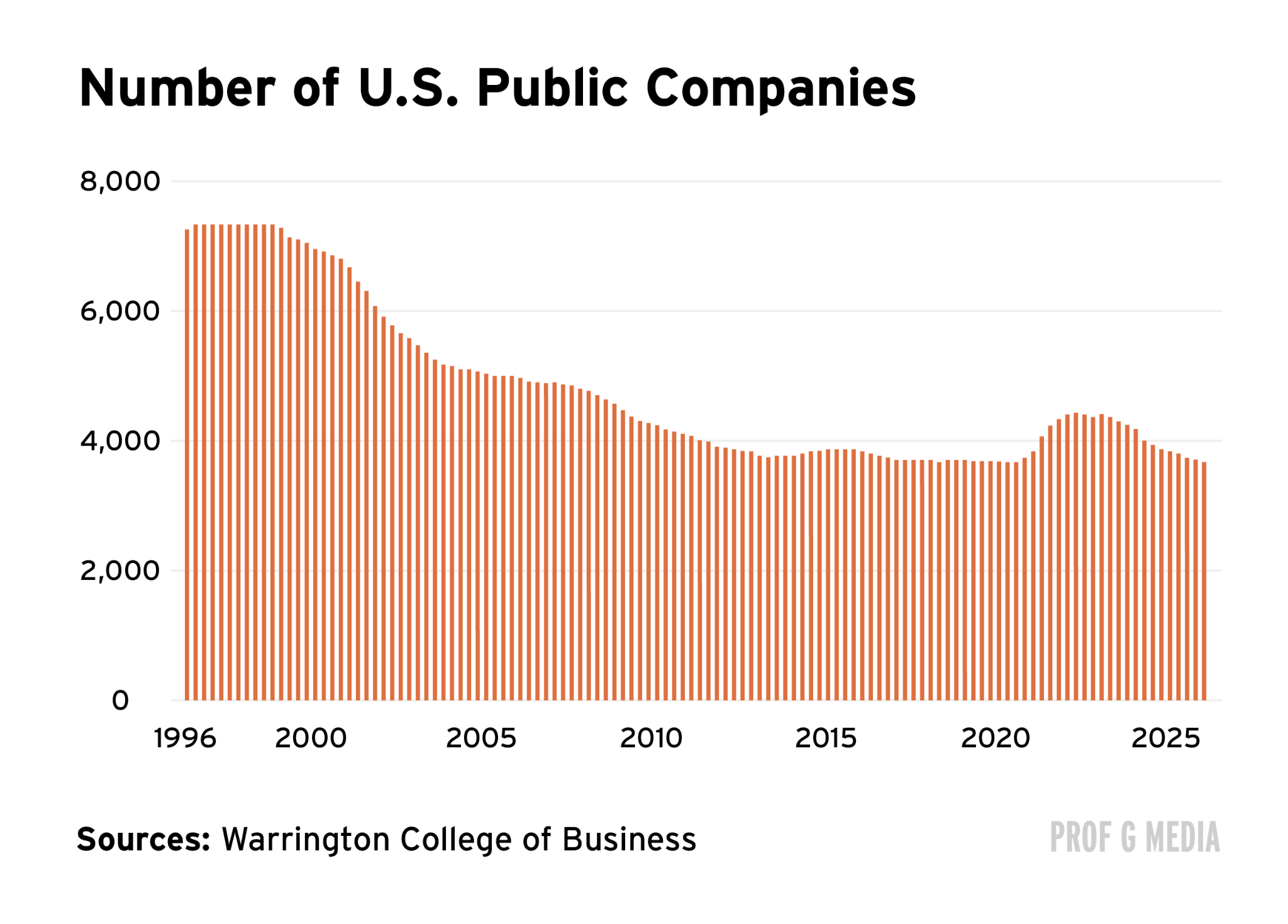

For years, stock prices have remained elevated, partly due to unusually low supply. The IPO market essentially collapsed after COVID. The number of public companies is half what it was 30 years ago.

This made investing quite easy, as all you had to do was keep investing in the companies that already existed. (Read: Big Tech.) The virtuous cycle of low supply and high demand drove the price of tech stocks ever higher, making them, on a risk-adjusted basis, arguably the greatest asset class in history.

But that’s all about to change, and violently so. SpaceX, Anthropic, OpenAI, and Google are about to inject roughly $350 billion of new equity into the market. That’s more money than the entire US venture capital industry invested last year, and more than was raised in IPOs over the past seven years combined. And that’s just four companies.

The question is whether stock prices (tech, in particular) can remain this high with this much new supply. I doubt it. Another way to think about it is the following: If investors want to fund $350 billion in new stock purchases, what will they have to sell? My concerns were recently validated by Goldman Sachs’s global head of hedge fund coverage, who said investors are “increasingly focused on whether US equity markets can absorb a growing wave of new stock issuance.” I read that as Goldman-speak for “we don’t think they can.”

History Rhymes

This isn’t anything new. Going back as far as the 1930s, blockbuster IPOs have consistently preceded periods of market underperformance. From Xerox in 1936 to McDonald’s in 1965, the dynamic is simple: Mega-IPOs tend to suck all the available capital out of the system, leaving very little capital left over to prop up the rest of the market. In other words, it doesn’t even matter whether or not SpaceX is a good investment (it isn’t). The market will be dictated not by fundamentals or narratives, but by supply and demand.

Don’t Buy The IPO

The most important question for investors this year is the following: Should you buy the SpaceX/Anthropic/OpenAI IPO? My answer is simple: F*ck no.

Aside from a dangerously high level of supply, there are other reasons to be bearish. It’s clear, for example, why these companies are all raising money at the same time: They believe this is the top. Sam Altman’s trillion-dollar question isn’t whether he can achieve AGI, but whether he can sell OpenAI stock at the highest possible price. He has finally found his moment to sell, and that moment is now.

This is also why IPOs generally underperform at first: They go public when investor exuberance is at its highest. One study found that within twelve months, the average tech IPO experiences a maximum price decline of … negative 55%. That means you can assume with relative confidence that at some point over the next twelve months SpaceX will be cut in half. Greed is a powerful and fleeting force, but AI greed may be more powerful and more fleeting.

Ghost IPOs

Homeowners hate it when large apartment complexes get built in their neighborhood. In addition to opening their community up to “the masses,” it also reduces the value of their homes. A similar event is about to take place in the stock market. SpaceX + OpenAI + Anthropic is the equities-equivalent of a residential megacomplex: Exciting for new residents, but bad for existing ones.

The critical question will be whether investors actually have the hundreds of billions of dollars these IPOs are asking them to spend. If they don’t, one of two things will happen: Either 1) they’ll sell their existing tech positions to fund their new ones (thus putting downward pressure on the markets), or 2) they simply won’t buy these IPOs. Both outcomes lead to a stagnant market, the second one arguably more so.

I’m reminded of those underoccupied developments in China. Many years ago as part of a national urbanization effort, the Chinese government spent billions building massive apartment developments in underpopulated areas. It would have been a great idea had they not miscalculated population growth — instead of soaring, the population went down. The result? Hundreds of high-rise buildings and commercial plazas with no one in them. Billions of dollars in infrastructure investment gone to waste. “Ghost cities.”

Could SpaceX, OpenAI, and Anthropic be the Chenggong District of the US stock market? The investments that “could have been” but “never were”? The Ghost IPOs? I don’t know, but one thing is clear: If ever there was a time to buy, the time isn’t now.

See you next week,

Ed

Ed, your Econ 101 chart is correct, but your application of it is incomplete. You shifted the supply curve but did not re-draw the demand curve. You also skipped past the fact that the market has been retiring shares faster than it issues them. Add demand elasticity to the picture and the analysis gets a lot more complete, and a lot less alarming. Short-term market indigestion after these mega-IPOs, I do buy. The 'trillion in supply forces a crash' version, I do not buy.

Don't forget the huge amount of money that will be funneled out of index component stocks to move the IPO stocks into them.