Twenty-three years ago, a scandal emerged on Wall Street. Henry Blodget, an equity research analyst who’d become well-known for his bullish coverage of some of the world’s hottest internet stocks during the dot-com boom, turned out to be privately bearish. In emails to colleagues Blodget described many of the stocks he’d publicly recommended as “crap,” “dogs,” and “POS.” After the bubble popped and valuations tanked, Blodget was charged with securities fraud, and the SEC banned him from the securities industry for life.

Blodget was the posterchild, but he wasn’t alone. At Salomon Smith Barney, another analyst who’d publicly rated one company as a “buy” was discovered to have called that same company a “pig” in private. Another analyst at Lehman Brothers admitted in an email that “ratings and price targets are fairly meaningless anyway,” and that the “little guy” might get misled. “Such is the nature of my business,” he wrote. It was an epidemic: By the year 2000, three-quarters of all stocks carried buy recommendations, and only two percent carried sell recommendations. I don’t need to tell you what happened next.

Why would Wall Street analysts recommend stocks they knew to be junk? One word: incentives. Since IPOs and equity offerings are important sources of revenue for investment banks, analysts are incentivized to publish glowing research about companies in order to win deals and generate fees. This conflict of interest was summarized well by a Merrill Lynch employee in 2002, who lamented to a colleague that “John and Mary Smith are losing their retirement because we don’t want [an investment banking client] to be mad at us.”

After the bubble popped, the SEC realized it’d better do something about this. So they came up with the 2003 Global Research Analyst Settlement. The goal was to neutralize the conflict of interest posed by investment bankers and equity research analysts playing for the same team. So, they separated the two divisions entirely: Equity research was no longer allowed to talk to investment banking (without a compliance chaperone present), and compensation for each group was divorced from one another as well. That way, the investment bankers could keep doing their job (winning deals), and the analysts could publish unbiased research..

Why am I talking about this?

Déjà Vu

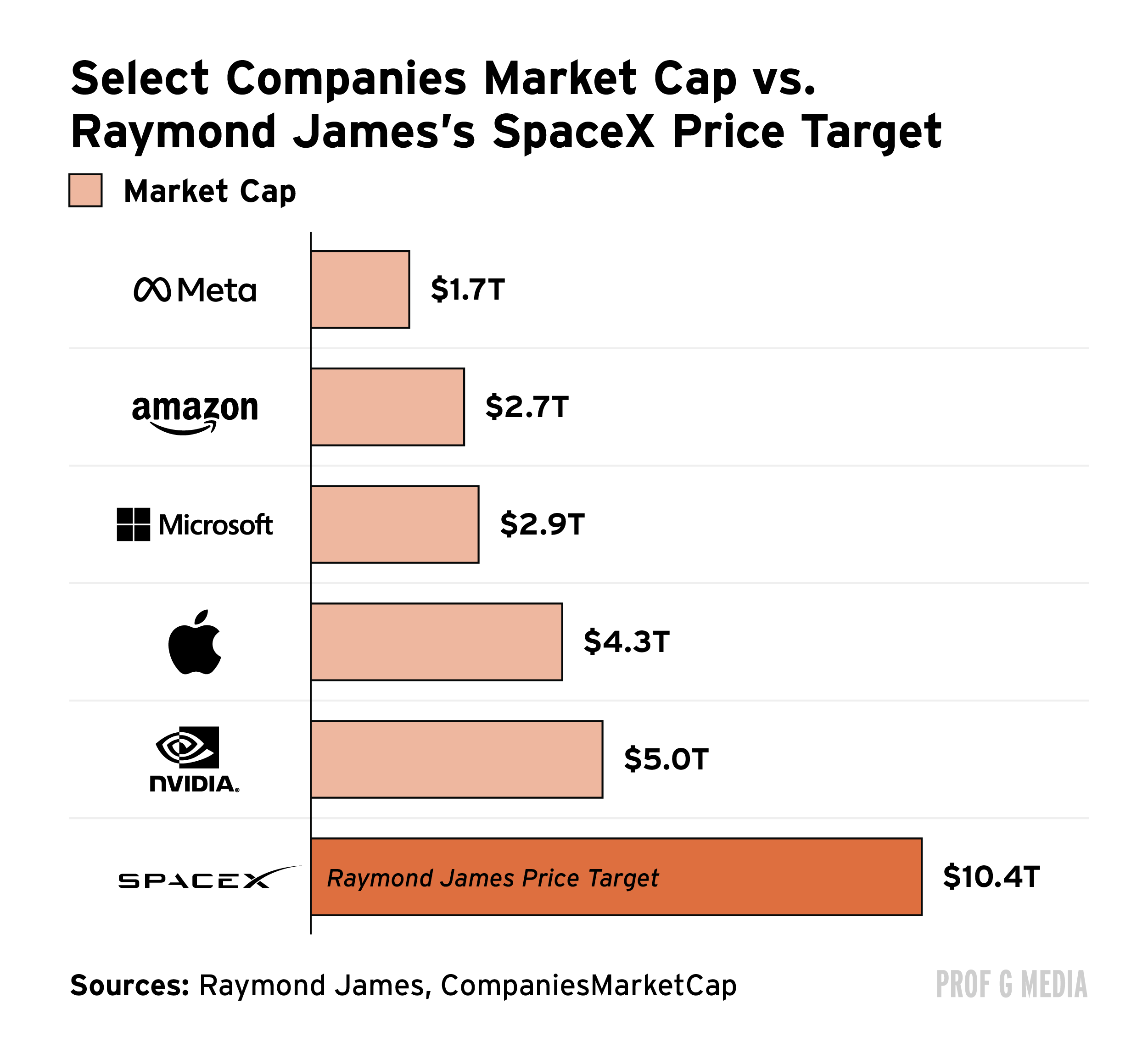

Last week, the Wall Street banks revealed their equity research for SpaceX, and the price targets were nothing short of insane. Before we discuss them, keep in mind SpaceX is already worth $1.8 trillion. With only $19 billion in 2025 revenue, that’s at least a trillion dollars too high. (I explain why here.) OK, now let’s look at what Wall Street “believes.”

According to JPMorgan, SpaceX is worth $2.9 trillion. That’s 58% higher than its current valuation. Their opinion is that SpaceX’s “potential impact on humanity” is “bigger than any company’s” they’ve “ever seen.” Deutsche Bank says the company is even more valuable: $3.3 trillion. In their view, the rocket-maker represents the “apex of civilisational ambition.” Over at Morgan Stanley, the number’s even higher: $3.9 trillion. MS says SpaceX is the “final frontier” of AI. But the price target that takes the cake belongs to lesser-known investment bank Raymond James, whose lead analyst says SpaceX is worth — wait for it — $10.4 trillion. That would make SpaceX more valuable than Microsoft, Amazon, Meta, Tesla, and Berkshire Hathaway … combined.

I have one question: WTF? I had to read the Raymond James report a second time just to make sure I wasn’t hallucinating. (I wasn’t.) Their “models” project SpaceX revenue will rise from $19 billion to more than $5 trillion by 2035. (That’s nearly a fifth of America’s GDP.) Ninety-four percent of that revenue will supposedly come from AI, which means the company’s AI business must become 23 times larger than Nvidia’s, despite currently being 67 times smaller. As I said a few weeks ago: Pass me the crack pipe.

Conflicted

These price targets are ridiculous — so ridiculous as to be inexplicable. That is until you realize the one thing that unites them all: They were all published by banks that underwrote the SpaceX IPO. Yes, Raymond James, Morgan Stanley, JPMorgan … they all participated. In fact, there is not one bank that underwrote SpaceX’s go-public and didn’t recommend the stock as a buy.

I know what you’re thinking: If the IPO already happened and the banks already collected their fees, what’s the incentive to publish flattering research now? Answer: More fees. SpaceX has already initiated a follow-on debt offering, and it’s estimated that the company will have to raise $235 billion over the next four years just to cover its costs. That translates to tens of billions of dollars in future investment banking revenue. There’s also talk that SpaceX will pursue a merger with Tesla, which would result in (spoiler alert) more fees. In sum, the most profitable business on Wall Street right now isn’t trading or lending … it’s getting Elon Musk to like you.

Open The Floodgates

But hold on. Wasn’t the 2003 Global Research Analyst Settlement specifically designed to prevent banks from bullsh*tting their research for fees? You’d be correct. That was, at least, until seven months ago, when it was … terminated.

Yes. On December 5th 2025, the SEC officially rescinded the law that Blodget had inspired all those years ago. According to the agency, the GRAS rule is now useless, as it’s been “largely superseded” by other rules. What they’re referring to is FINRA Rule 2241, a law that technically speaks to the conflict-of-interest problem, but does very little about it by comparison. As former SEC Chair Arthur Levitt wrote in his aptly-titled piece, The SEC May Make Wall Street Analysts Corrupt Again, “Don’t be fooled by the promise that other regulations provide this separation … This is the natural pattern of regulatory surrender.”

I’d be inclined to call Arthur Levitt alarmist if it weren’t for the fact that the SEC is literally being ripped apart. The agency has lost a fifth of its workforce under Trump. Last year, it brought just 56 enforcement actions against public companies — down 30% from the year before, the lowest of any transition year in a decade. Four months ago, its enforcement director, Margaret Ryan, mysteriously resigned after she tried (and failed) to investigate the Trump family for insider trading. It’s become clear that the SEC no longer exists to protect investors, but white-collar crime.

Here To Stay

If flattery was the dealmaking equivalent of a bazooka in the dotcom-era, it’s a nuke today. Saying nice things about powerful people can now win you multimillion-dollar deals, unprecedented legislation, and even cabinet positions. Tim Cook didn’t present that gold trophy for the President — he did it for shareholders. Few endeavors yield greater returns in 2026 than being a sycophant, and any executive who hasn’t clocked that isn’t fulfilling their fiduciary duty. In other words, who wouldn’t talk up SpaceX?

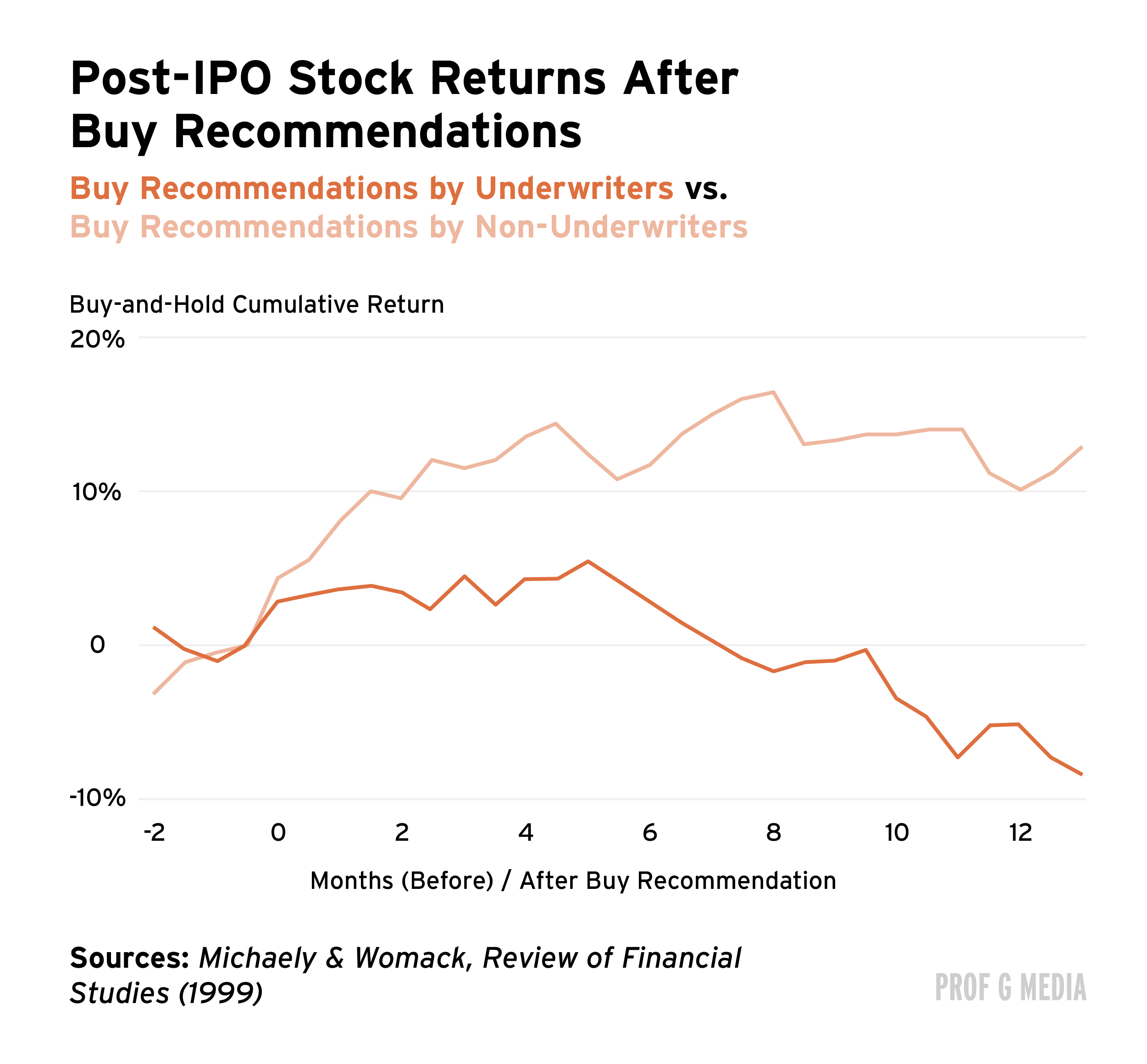

The trouble arises, of course, for the retail investors. SpaceX is already down more than 30% from its highs, and anyone who bought post-IPO is now underwater. This is in line with the trend: Research shows IPOs recommended by analysts at underwriting banks underperform and, on average, lose value. Lesson: If someone’s been paid to sell you a stock, proceed with caution.

The truth is, SpaceX at its current price is a bad investment. This was tacitly admitted in Morgan Stanley’s equity research report, which issued an “intentionally wide” price range with a bull-case target of $600 and a bear-case target of … $75. Translation: “We don’t have a f*cking clue.”

People wonder why so many Americans hate Wall Street. This is why. It doesn’t mean the analysts are bad — it just means the incentives are. In the words of Charlie Munger: “Show me the incentive and I’ll show you the outcome.”

The solution is simple: Fix the incentives. Either restore the Global Research Analyst Settlement, or find another way to eliminate conflicts of interest. It shouldn’t be that hard, but for this administration it might be, as it would undo the culture of corruption they’ve worked so ardently to build. So if you’re expecting things to change, take this analyst’s recommendation: Don’t hold your breath.

See you next week,

Ed

This piece, and the other content that Ed has produced regarding SpaceX, is excellent. One more reason for most retail investors (me included) to stick with index funds and sensible asset allocation strategies.

With the advances in technology and information, every analyst, same as every company, politician and KOL (influencers) should release their investments and holdings, in a public way.

A mere “full disclosure I invest in X” sometimes isn’t enough.

A standard way to share your portfolio holdings (doesn’t require all the details) most be enforced by consumers. We should get to a point where not doing so should be frowned upon.

This issue is fixed bottom up, not top down